Happy Independence Day from Dual Income No Kids To and your family!

if you’re out shopping on America’s birthday, don’t forget to stick to your list and use coupons.

Happy Independence Day from Dual Income No Kids To and your family!

if you’re out shopping on America’s birthday, don’t forget to stick to your list and use coupons.

All,

One of the unfortunate downsides about being married is the fighting. And the reality is that while men tend to be the more aggressive of the two sexes, in domestic situations women can dish out as much as they receive. So if you find yourself asking “my wife yells at me – what do I do?”, here are some hopefully helpful thoughts.

Note, this article is primarily for men having trouble with their wives yelling at them, but it can apply more broadly across genders and sexes. Anger is a complicated emotion. In a lot of cases, anger can be destructive and in other cases it can be constructive. Anger is also a normal response to some situations. So, its not straightforward to manage.

A lot of advice on the internet isn’t much good. For example this question “my wife yells at me”, was posed on Quora. The tenor of the comments were basically that if your wife yells at you you should dump her. This is terrible advice as getting divorced over a character issue is a bit like cutting off your foot because your toe is broken. Here is what they say:

And here are some responses:

And one more.

Source: Quora.com

Divorcing your wife may not stop the yelling – if she is angry at you over something, divorcing her will just make her angrier. And it may not immediately solve your problem. Divorces are extremely expensive and can take years to legally and emotionally untangle. This is especially the case if you have property or children (example here). So even getting rid of your spouse may not solve your problems – this person may be negative to you for years afterwards, even if you do split up. So, if you’re wondering why my wife yells at me, don’t implement an extreme solution to what could be a manageable problem.

The reality is most people aren’t pathological, or all that abusive. People sometimes just lose their temper. In any event, angry people really want to be heard. Her being angry sometimes isn’t about you. She may be triggered by something. When there are events in our life that have any similarity or remind us of previous negative events in our own history, our brain perceives a threat and gets activated. So your wife being angry may not about you. In any event, listening to what your wife is telling you nonjudgmentally is not going to hurt.

Your objective here is to understand what’s going on with her. Not anything else. If you are not clear on something, ask.

Listen carefully to what she is saying. You won’t get anywhere if you don’t understand her.

Keeping your cool when someone is yelling at you is difficult, but serves you in the long run.

According to the Gottman Institute, humans are biologically wired to be sensitive to danger. Often being yelled at or fighting with our partners can trigger these biological reactions. One of these is an increased heart rate. Another is chemical changes in your brain that which release memories or other thought processes that aren’t immediately articulatable. When you’re upset, it often means that you are not thinking rationally and aren’t able to have a meaningful conflict reducing conversation.

A good idea when this happens is to take a break. Get some physical space from the situation. But, you also need to get some mental space. Take your mind off being yelled at and instead go for a walk, work out, listen to a podcast, surf the web, mediate or the like.

Probably both you and your wife need to improve your emotional intelligence and communication skills. When things are calm, encourage your wife to manage her yelling in a healthy way. Healthy ways to process anger can include yoga, physical exercise or deep breathing. You may need to read a few books on building emotional intelligence and patiently work with her to get her stop yelling.

At a minimum when you’re talking with your wife about the yelling, you need to avoid doing these things:

If you are doing any of this behavior when you talk with your wife, stop immediately. Don’t do it again. You’re only shooting yourself in the foot.

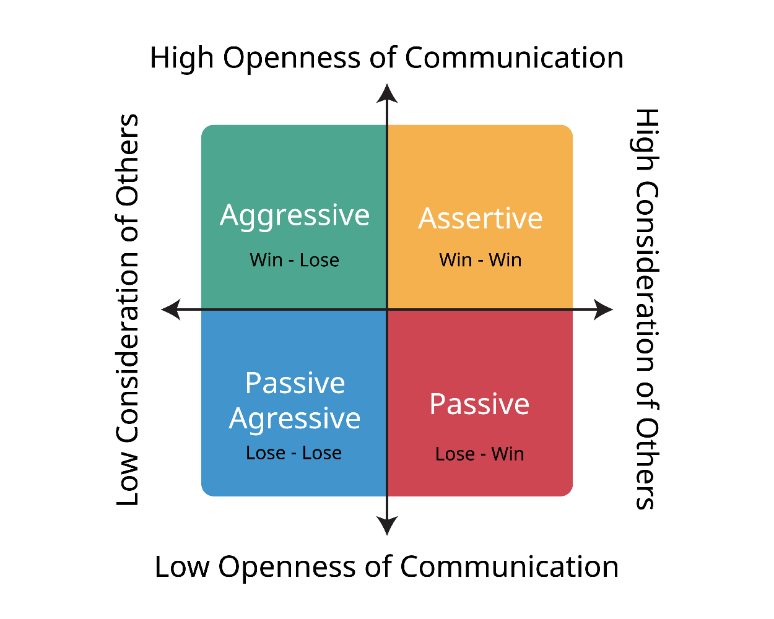

If your wife is yelling at you, you need to be assertive about telling her to stop. Sometimes people yell because they believe it is an effective way to communicate. So, she may need to hear the same message consistently, politely and assertively delivered until it starts to sink in. This may take seven or eight times over a period of weeks or months.

A good way to do this is to phrase it in terms of your needs. Use I statements and say things like “I need to spoken to in a calm manner”, or “I do better when I’m spoken to in an everyday tone of voice”. When you state your needs this way, it sends a message about how you want to be treated, in a way that leaves it open for your wife to respond in a healthy way.

In any event, assertively standing up for yourself generally improves your self esteem and it also sets a limit that you can’t be pushed around. Eventually your wife will get the message that there is a better way to communicate. The key here is you need to be consistently assertive over time.

If you’re asking “my wife yells at me – why?” One important factor to consider is social isolation. A lot of men don’t want to disclose that they’re having domestic issues. Society teaches that men should be self reliant and handle problems without asking for help. That said, this rule doesn’t apply to domestic trouble. Talk with a friend or family member you trust about this. Getting perspective will help you with a sanity check and see if your assumptions are reasonable.

Also, if your wife is yelling, on some level she may know its not okay. So, if she knows that other people know, she may curb the behavior.

Finally, if you really think you are in abusive relationship, get some help. You’ve got a couple of options. First, you can call the National Domestic Violence Hotline. That number is: 1-800-799-7233. They appear to have Spanish speaking counselors as well. Their website is here. They have live chat and text options.

If you need something more heavy duty than that, consider hiring a marriage counselor. The most direct way to do this is to ask around or hire someone. Psychology Today has comprehensive listing of accredited counselors. You can even sort by price, which is good if you are budget conscious.

There are a couple of good books you might consider reading as well:

Getting the Love You Want, Harville Hendrix

Seven Principles For Making Your Marriage Work, Gottman.

How To Tell Your Spouse They Don’t Make Enough Money

Yes, Making Unilateral Decisions Can Impact Your Relationships

All,

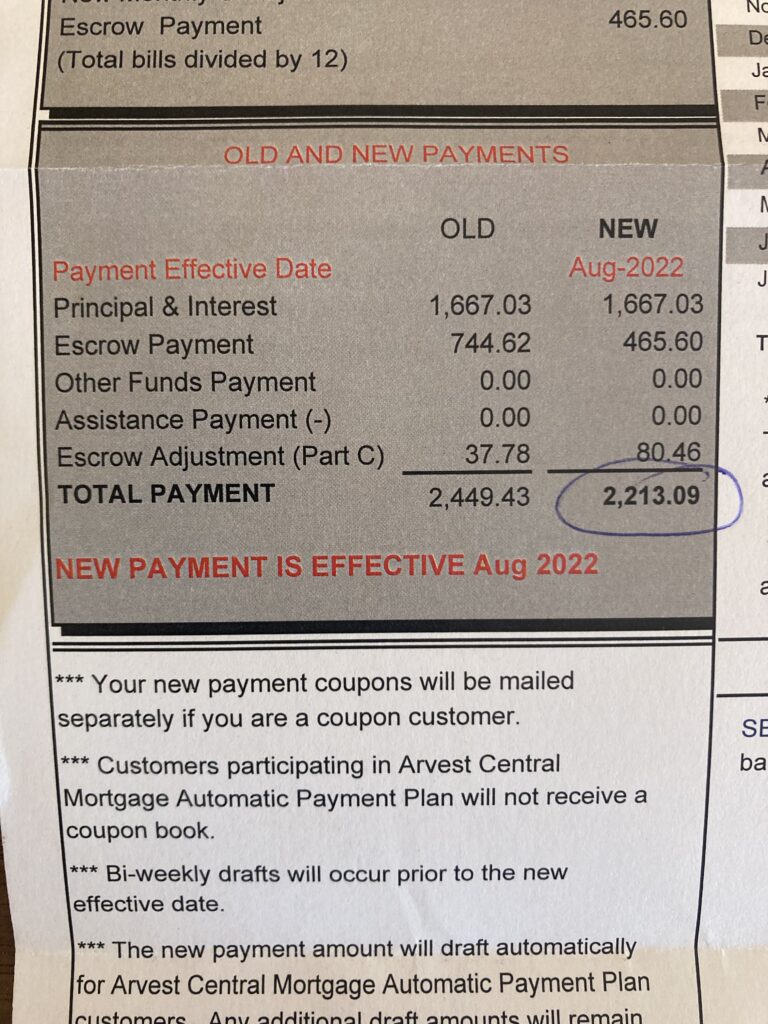

Wanted to share a couple of personal updates with DINKs readers. Today, I got the private mortgage insurance (PMI) taken off my condo and I picked up some passive income payments from a couple of companies I’d been working with. It was super nice to come back home from work and have the good news in the mail box.

When I initially bought my condominium unit in Portland, Oregon I only put 7 percent down. So I had to pay PMI. I’d been paying about $279.00 per month for PMI for the last seven years, and hating every payment. Since the Portland condo market had been strong for the past couple years, the value of my place had increased substantially. As a result, I had more than 20% equity in the condo, so I applied to have PMI taken off.

Well the application was successful! Here is my new escrow statement.

Its gonna be great to not have to pay PMI.

When I came home I had a couple of payments waiting for me. For some context – I’d been focusing on picking up extra money by selling my browsing history and other data. A couple of the companies I’d been using paid out.

Nielsen Opinion Rewards – paid $10.

Savvy Connect – paid $5.

I’ve included links to both of those companies – if you’re looking to pick up some passive income, I recommend both. They are a bit of a hassle to install, but otherwise they both pay well and reliably.

Goodbye PMI, hello money indeed!

Yes, You Can Make A Ton Of Extra Money

Hello Dinks,

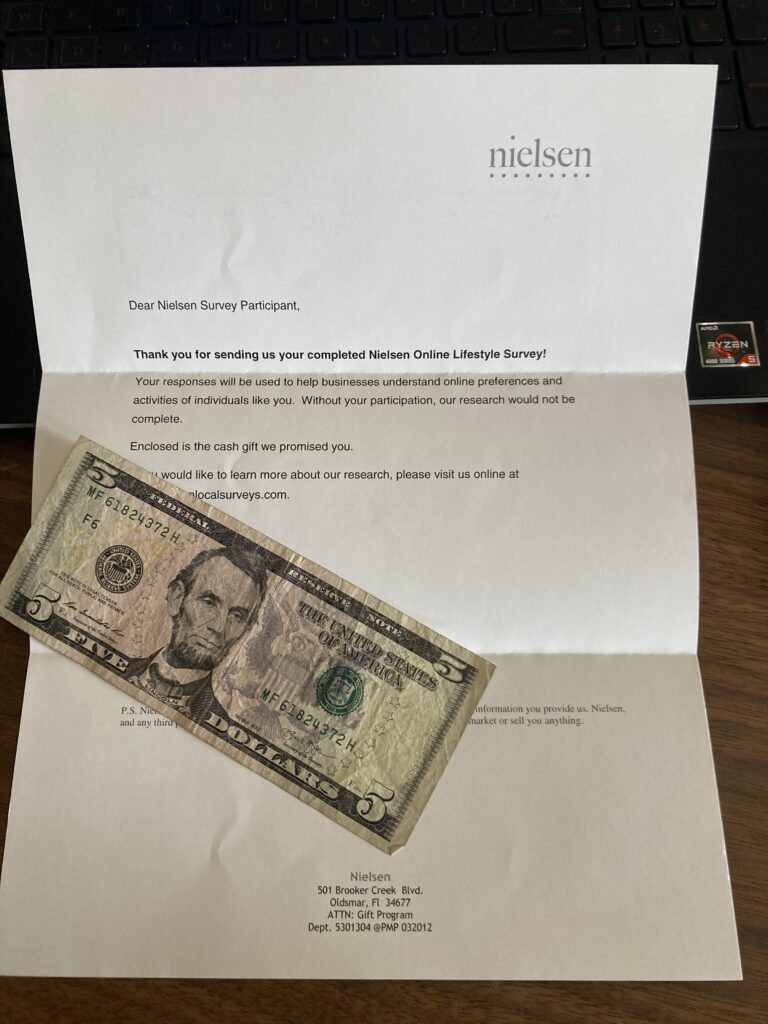

I came home this afternoon to a pleasant surprise. I’d received an old fashioned letter with five bucks in it. The five bucks was from a survey I’d done for Nielsen. If you’re not familiar with Nielsen it’s a publicly traded data analytics and measurement company (here).

I’m part of their Computer and Mobile panel. The panel is relatively straightforward. You install their software on your phone or laptop and in return you get points which are convertible to cash, which is valued at about $5 a month. They also send survey opportunities, which is how I got the $5.

If you want some semi-passive income, I’d sign up for Nielsen’s panel. Pretty much all you have to do is install it and collect. Install is painless (here). Once its installed, you pretty much just have to check their rewards porthole every month to collect.

Five bucks isn’t much, but it does add up over time. Especially if you can invest it in something productive.

For more on extra money, consider reading these:

Yes, You Can Make A Ton Of Extra Money.

All,

In honor of yesterday’s inflation numbers showing a year over year increase of 8.3% I am posting a bit of inflation humor for your enjoyment:

Since inflation has a massive economic impact, and since there isn’t a whole lot you can do about it (other than buy I-bonds and wait for the Federal Reserve to raise interest rates), you might as well laugh a bit…so here are some more inflation jokes.

Inflation is out of control

That’s just my $5 bucks.

Inflation is really getting out of hand..

That’s just my 3 cents.

What did the banker say when he heard inflation was at an all time high?

That really peaks my interest.

Hat tip: Upjokes.com

Shrinkflation, Now With Less Farfalle

Hi All,

So – every time I go shopping, I’m reminded that the US is living through a period of high inflation.

I went to my local Kroger last week, and picked a few boxed of Kroger brand farfalle pasta. And, wouldn’t you know it, once I opened the box the thing was a 1/3rd empty. This is on top of the fact that prices for past at my local Kroger have climbed by at least 20% in the past few months, so I’m looking at getting less pasta and paying more for it.

Incidentally, economics call this shrinkflation. Per Wikipedia “shrinkflation, also known as deflation or package downsizing, is the process of items shrinking in size or quantity, or even sometimes reformulating or reducing quality, while their prices remain the same or increase. The word is a blend of the words shrink and inflation” (cite).

So, shrinkflation in full effect here in Portland, Oregon.

Evidently everyone knows what’s going on as well. CBS News has covered it, so has the WashingtonTimes, and the New York Post. And there is a whole subreddit devoted to it.

If you’d like more on this, consider checking out Milton Friedman’s excellent explanation of how inflation gets started.

And here are a bunch more articles on inflation:

Inflation At 40 Year Highs Here Is Some Context

Hello Dinks,

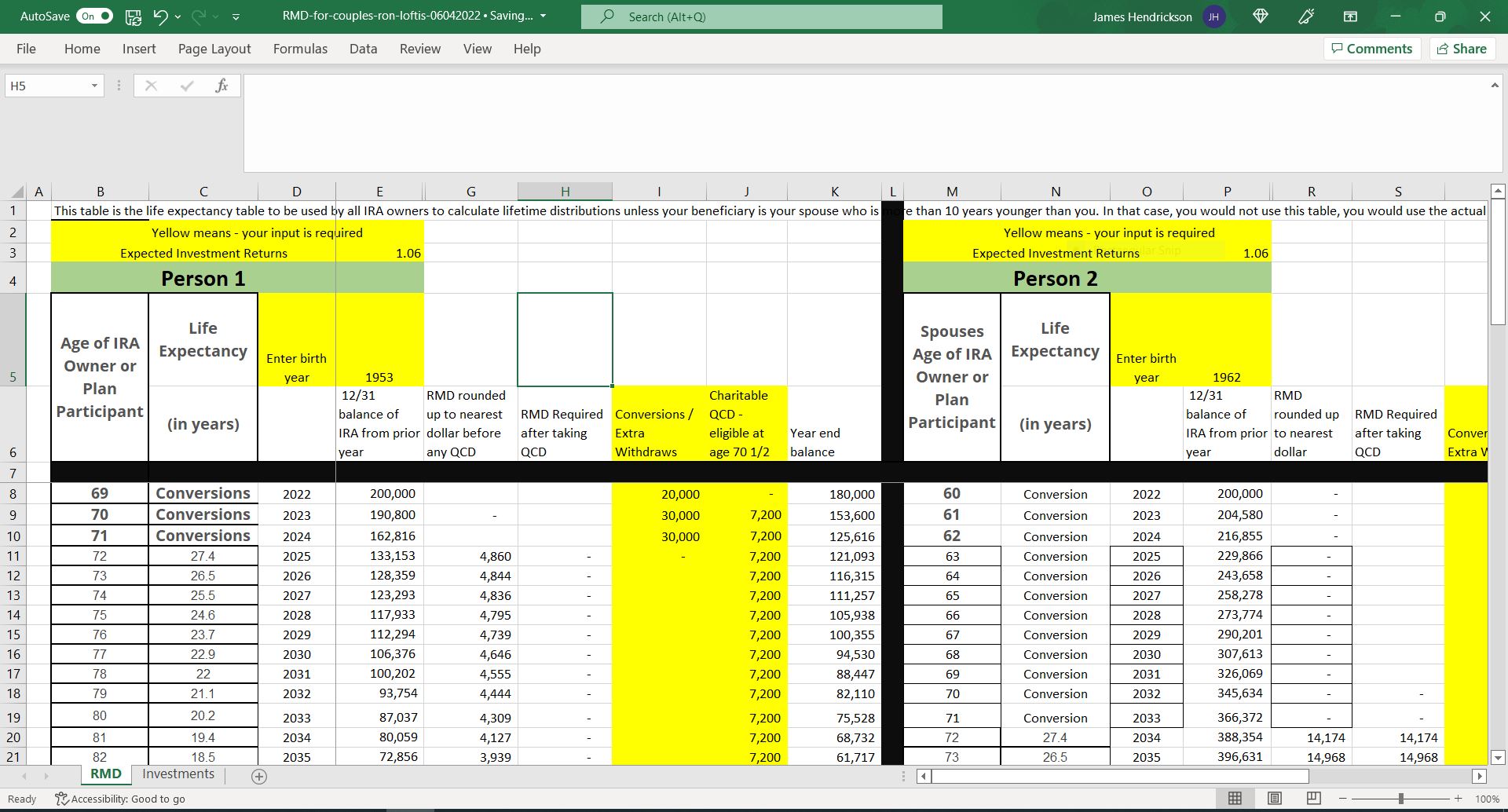

If you are a couple looking at retirement in the next few years, you might be wondering the required minimum distributions for couples are. And you might want to calculate these yourself.

Well, there is a spreadsheet for that.

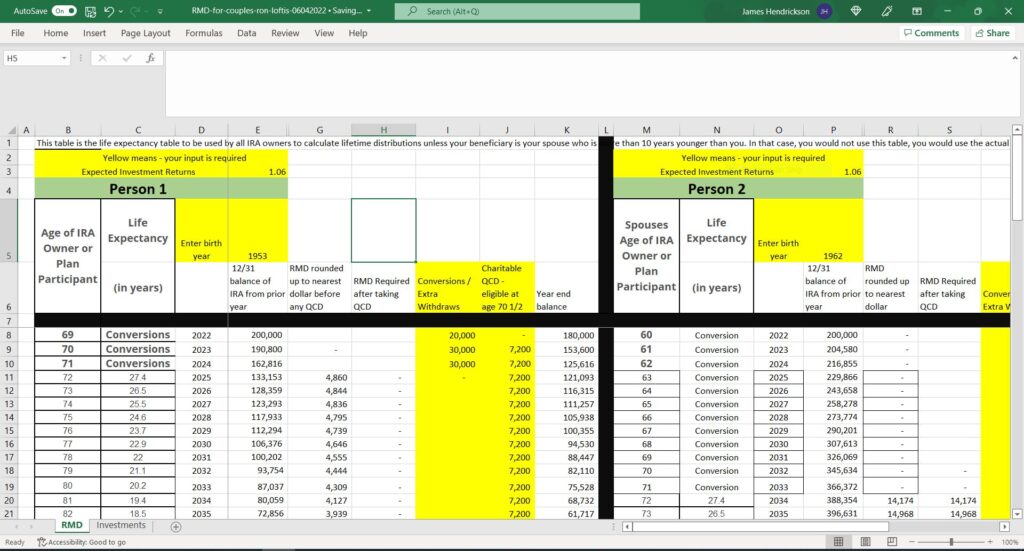

A friend of dinksfinance has produced a very nice required minimum distributions (RMDs) spreadsheet for couples. It is a simple excel file. The sheet has columns for the age of each person in the couple, as well each persons projected life expectancy. The sheet calculates how much each individual would need to withdraw, and how much collectively the couple would need to withdraw. It looks like this:

The spreadsheet is downloadable here, free of charge.

Here are some points to keep in mind:

First, you have to start taking required minimum distributions at age 72. So, unless you are older than 55 or a hardcore retirement planning enthusiast, RMDs are not something you need to immediately worry about. Second, required minimum distributions only apply to employer-sponsored retirement plans, traditional IRAs, SEP, or SIMPLE individual retirement accounts (IRAs). If you’re saving for retirement using other types of account it doesn’t apply.

Third, Investopedia has a very good basic article on required minimum distributions, here. It is worth reading if you want to try these calculations yourself.

Fourth, the spreadsheet is a preliminary “work in progress”. Feel free to edit or modify as you see fit.

Hat Tip: Ron Loftis for creating and sharing this sheet.

All,

For this posting, I’m sharing a couple of neat finance sites I found, as well as a personal wealth update.

Here are the two sites I found:

So I was looking around for additional passive income sources this morning and came across Neevo. Neevo is an AI training site where you can get paid to help train the software by doing micro tasks like grading essays or correcting grammar mistakes in text messages. The site says pretty much all you need to do is be human, have time, and have an active PayPal account. I haven’t used it yet, but it looks fun.

So I was looking around for additional passive income sources this morning and came across Neevo. Neevo is an AI training site where you can get paid to help train the software by doing micro tasks like grading essays or correcting grammar mistakes in text messages. The site says pretty much all you need to do is be human, have time, and have an active PayPal account. I haven’t used it yet, but it looks fun.

Roofstock is the second site I found this morning. Roofstock has a business model where they help you buy single-family residences and provide full-service property management. The company is geared toward medium-high net worth investors, with most properties valued at $100 thousand up to about 600K — meaning this could be an excellent investment opportunity if you have the cash for it. Roofstock is here.

Roofstock is the second site I found this morning. Roofstock has a business model where they help you buy single-family residences and provide full-service property management. The company is geared toward medium-high net worth investors, with most properties valued at $100 thousand up to about 600K — meaning this could be an excellent investment opportunity if you have the cash for it. Roofstock is here.

Today I did a few things that won’t move the needle but will add incrementally towards my net worth goals this year.

1) Prosper. Added some money to my Prosper.com account. It was only $50 bucks, but it was what I wanted to do for the year. My Prosper portfolio has been paying about 4.6%, which is way less than current inflation numbers.

2) SMBX. I also added three more bonds on SMBX. I like SMBX. It’s a neat little marketplace for small business bonds. I like it because it’s improving minority access to capital. It is also a nice way to diversify away from stock and real estate. Its website is here.

3) Debt. I was able to get a big chunk of my credit card debt paid off – that was a huge relief.

4) Lots of dividends. I have like fractional shares in over 30 stocks. So every few days I get an email saying I’ve got a dividend. Most of them are pretty small – like 2 cents or a dollar or whatever. While the amount of money is small, getting emails is a confidence builder.

5) Bought Stock. Picked up about $25 worth of the S&P 500 and $25 in Costco stock. I bought this via Stockpile, which is a kind of a dumb move because my stockpile account isn’t tax advantages and I haven’t maxed out my retirement. That said, there is a virtue in acting so I went ahead and bought the stock. Costco has been making money hand over fist and profited a lot from the Covid 19 Pandemic.

For more on wealth building research read these:

How Much Wealth Did James Have In May 2022?

Our Top Ways To Make Extra Money

List of Microincome and Microsavings Apps

James’s December Net Worth – Drooping Assets and Living Off The Land

SMBX – Bonds For Socially Conscious Investors With An Appetite For Risk

Readers, do you have any wealth-building wins you’d care to share? Leave us a comment below.

Now that I’m in my 40s, I meet a lot of single people. Maybe they’re divorced or what have you. A lot of them seem totally focused on staying single, yet they want to be financially independent. This is a shame because in staying single is building wealth with the brakes on. That is, if you are in a marriage where you work well with your partner, your wealth really improves.

Here is an example from a Facebook group I’m part of.

And here is the same perspective on Twitter. Its popular.

This attitude is a shame, because staying single but wanting financial independence is building wealth with the brakes on.

Here is a research finding:

Findings show married couples have higher levels of wealth than all other household types.

– Asset holding and net worth among households with children: Differences by household type. Grinstein-Weiss, et al. Children and Youth Services Review, Volume 30, Issue 1, January 2008, Pages 62-78.

This just one example, but the finding is consistent wherever you look.

There are economies of scale, but also a number of significant tax and fixed expenses benefits.

Hat tip: Investopedia.

So here is the takeaway, if you single, consider getting a partner and teaming up with them. Being single is basically wealth building with the brakes on. You have none of the economic or tax benefits married couples have access to. In contrast, if you are happily married, you’ll have have someone to share your struggles with. And, since since you’re typically living together you’ll realize household economies of scale – including only having to pay one rent payment or one utility bill (instead of two).

What Dave Ramsey’s Take On Marriage Is Missing

The Grass Is Greener Where You Water It

Yes, Unilateral Decisions Affect Relationships

Getting Together, Getting Hitched – Prenups And More

Yes, Married People ARE Richer

Why Does Marriage Build Wealth?

If you are married and its been good for your finances please leave a comment below!

Hi Dinks,

May was remarkable for its consistency with the rest of the year. There weren’t a lot of drastic changes, just a lot of grinding out extra money and keeping the show on the road.

I’ll just highlight some of the positives, then share where I have some room for improvement.

A) Tornado. A friend from Facebook turned me onto Tornado (formerly Nvestr), which has a learn and earn program. I’m liking it so far because the platform is super easy to use and has provided about 40 bucks worth of sign up incentives. Unlike a lot of people, I don’t mind doing sign ups for $40 or $50 bucks. Tornado has also done a good job from a user acquisition and onboarding standpoint. Their interface is slick and well designed, and I’ve been having fun with their platform.

B) DimeFi. I also took advantage of an “invest $20 and get $20” offer from DimeFi. DimeFi is an up and coming cryptocurrency brokerage. I have the $40 in their USD coin which is yielding 6%.

C) I-Bonds. I bought about $650 worth of I-bonds. For those who don’t know, I-bonds are the Federal governments inflation protection bond product. They’re paying 9.6%, which is way better than the rate on my checking account. The only trouble with the bonds is they basically preserve your capital, that’s it. They don’t grow your wealth. In any event, it’s better having bonds than watching ten cents on the dollar disappear due to inflation.

D) Selling My Personal Data. Selling my data is working. I’ve been able to get modest amounts of cash from Earn App and Packetstream.

A major challenge is I’ve been running a budget deficit, which hasn’t helped. The major issues are childcare costs and housing – that’s been running me consistently into the red for the last year or so – and my credit card debt is the result. This kills me because I’m frankly a bit ashamed of it. I’ve been actively building wealth for over a decade and know better. Also, my employer has been flaky about paying me. So, I’m frankly a bit bummed about my wealth building this month.

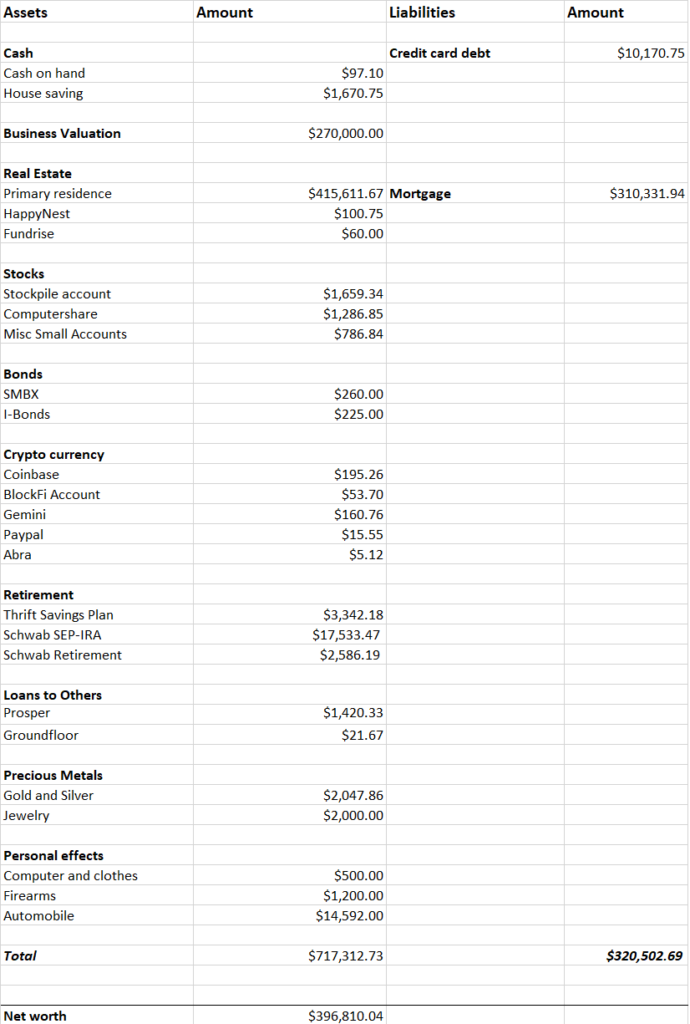

Here is my net worth for May.

Note, these figures were calculated before the market downturn at the end of this month, so the stock numbers are a bit inflated.

If you want to read more about mechanics of wealth building, consider these:

Our Top Ways To Make Extra Money

Better Models for Building Wealth

List of Microincome and Microsavings Apps

You cannot copy content of this page