Hey Dinks Readers,

What would you like us to write about?

Leave a comment below and we’ll see what we can do.

Hey Dinks Readers,

What would you like us to write about?

Leave a comment below and we’ll see what we can do.

If you’re shopping, don’t forget to check your receipts closely!

I was at Kroger earlier this week and bought a bunch of dish soap. The soap was on sale for $1.77, but rang up as $2.56. This was almost a dollar more.

The reality is a lot of grocery stores don’t always have their systems updated, so it pays to check your receipts. If you find they made an error, you can always go to the customer service desk and get your money back. So, it pays to check your receipts.

For more personal finance life tips, consider these:

Hi All,

Like a lot of dinks, you probably have a full-time job and are interested in ways to economize without committing to a part-time job. So here is a comprehensive list of Microincome and Microsavings apps. By and large, these don’t take a lot of time to set up and maintain. Many of them are also passive or semi-passive.

All of these pay small amounts in cashback, points that translate into dollars, Amazon credit or crypto, or micro-work which are 15-minute jobs that pay about $1.50 or so. Some of these, such as bandwidth selling apps or passive income apps have some upfront setup time, but little in the way of ongoing maintenance work.

Here is the list ordered by type of app:

This list of Microincome and Microsavings apps is bringing in maybe $350 per year. They aren’t big moneymakers. However, using them can give you some extra money.

The winners are:

1. Selling spare bandwidth apps. I have all five installed on both computers in my home. All five together generate about $10 per week.

2. For surveys: 1Q is the winner. It pays 25 cents per question. It has fewer questionnaires but at 25 cents per question, it is well worth it.

3. Nielsen Opinion Rewards – also very low maintenance

4. Tapestri – it generates about 15 cents a day and pays on a net 60 basis.

5. Amazon Shopper Panel – it’s $1 in Amazon credit per each receipt you scan. Most of the other receipt scanning apps pay pennies

Zogo is an interesting little app. It’s funded by a credit union and you get paid in Amazon credits for doing educational modules about basic personal finance topics. It is good if you’re a beginner and want to get paid to learn about personal finance.

By and large, this list of Microincome and Microsavings doesn’t make sense if you’re bringing in $150,000 or $200,000 annually. However, if you’ve got a lower salary and you want some extra money for groceries or for investing, a lot of these are worth the time.

If there are any good money makers that I’m missing, please let me know by leaving a comment below!

For more on generating Microincome read these:

Ways To Make Extra Money

Building Wealth on $600 Per Month

Wealth Building After The Basics

The Streams of Income Of The Wealthy

P.s This article contains referral/affiliate links.

All,

It is mid-March, so I sat down and added up my net worth this weekend. My wealth was $402,000. This is up $386,000 from December of last year.

The major components are my online business, the equity in my condo, stock, and some other assets. Here are the actual figures:

Here are some highlights that are working for my wealth building – they may also work for you.

I’ve started experimenting with selling my unused bandwidth using several pieces of software. The one that is working most consistently is called EarnApp. I have it installed on two laptops at my home and its generating about $5 per week. Which is pretty good for basically doing nothing.

If you have an unlimited internet plan and want a few extra bucks, the apps I am using are: EarnApp, Packetstream, Honeygain and Peer2Profit. All of these are generating between $1 and $20 per month.

I’ve been selling my personal data for about six months. This isn’t yielding much, but since it’s largely passive, it is free money. This is giving me about $20 per month. I’m using Invisibly, Reklaim and Nielson Opinion Rewards.

For the last couple of years I’ve been able to consistently save small amounts in my retirement accounts. Its been paying off.

Inflation numbers are running at 7.9% percent for the last 12 months (per Bloomberg), and from what I’m hearing global food prices are up 40 percent. I haven’t done much in particular to cope with it – there does not appear to be a silver bullet. What I have been doing is stocking up when I can find a bargain on food that will keep.

For example, I found several cases of Campbells soup that were retailing for 10 cents each at Kroger. I bought as much as I could carry. Normally each can retails for $1.25, and it’s super clear that the price of metals, wheat, poultry, etc. are just going to go up in the next 12 months. So I wanted to lock in a solid deal when I could.

Just to wrap this up, at the moment I’m single, which puts me at a wealth building disadvantage relative to married couples or DINKS. On average married couples without kids are richer, partly because they have economies of scale (e.g. one housing payment, family plans on phones, shared insurance plans, etc.). Married couples can also cooperate on important goals – like paying off a mortgage or saving up a nest egg – in a way that singles can’t.

For More On The Mechanics of Wealth Building, read these:

James’s July 2021 net worth – Tracking works

December 2021 Net Worth – Drooping Assets and Living Off The Land

This posting is for everyone who wants to save money but has trouble doing it, or needs a case study on how to save money.

Here is the backstory. I got sick of not having money and always needing to sell assets or put big-ticket emergency expenses on my credit card. For example, I had a 1997 Toyota 4Runner that needed an engine replacement — twice. Both cost $7,000 in total. I was able to cover a part of it by selling some of my silver and gold, the rest I had to put on my credit card.

So, I decided to get my act together and build up an emergency fund.

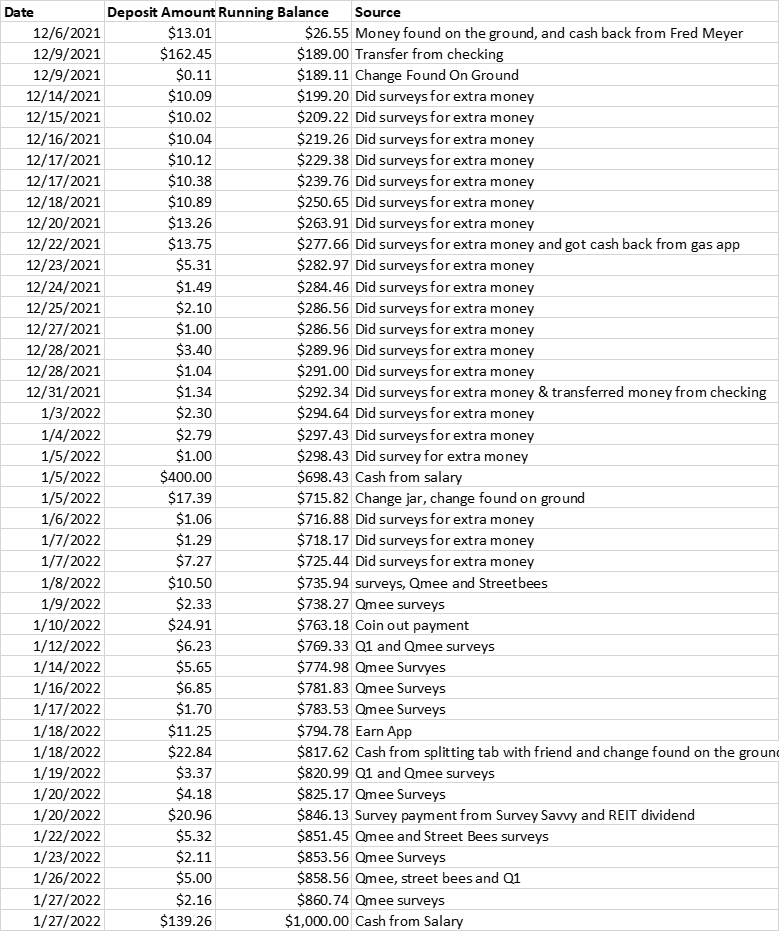

I saved $1,000 in cash after six weeks of very part-time effort. So you can see the specifics, here are the transactions, the dates, the sources of the funds, and the balance.

.

To save $1,000, I basically implemented a hybrid strategy to raise the money.

To help me save $1,000, I had to hack my behavior. First, I decided on the amount I wanted to save. Second, I decided when I needed to have the savings done. Third, I committed to doing it. And, to be sure I kept it in mind, I wrote down the goal and put it over my desk. The mental commitment was probably the most important part.

To remove the temptation to spend the money. I set up my accounts so the savings was hard to access. I have online access to most of my accounts. However, for my savings account, I deliberately did not set this up. Instead what I did was use PayPal to move money around. This worked out fine as most of the apps and surveys pay via PayPal anyways.

Here are some helpful takeaways from this case study:

1. If you want to save $1,000, set a goal with a timeline and commit to it

2. Use multiple sources of income

3. To supplement your salary, consider getting small amounts of money, taking surveys (Qmee is best), and using cashback or cash-producing apps.

Readers, if you know a good way to generate extra cash for savings, please leave a comment below.

Hi Guys,

So I got up this morning and CNBC had the blaring headline “U.S. inflation in January surged at fastest rate in 40 years” (clicky). From the article:

The annual rate of U.S. inflation is rising at its fastest rate in 40 years as supply-chain disruptions and rising transportation costs show no sign of abating.

A key inflation gauge, the Consumer Price Index, rose 7.5% from a year ago, the Labor Department reported Thursday — the largest increase since May of 1982. Core inflation, which strips out volatile food and energy costs, was 6%. The CPI index rose 0.6% in January, the same pace it showed in December but a slowdown from the 0.9% monthly increase in October.

Part of the problem for consumers in adapting to inflation is…the public doesn’t understand it. So, rather than write a novel, I’m just going to share a video on the subject from the late economist Milton Friedmann.

I recommend you listen to it while you’re working. Friedmann’s thinking is clear and logical, which is a change from most of the drivel in contemporary media.

If you don’t have an hour to spare, here is the main idea: the only way to stop inflation is to have government create less money and spend less money. And, the reason why we have inflation is because the public wants it, and demands the government give them money.

Hey Dinks, its January, so here is a personal update. I’ve mostly been looking at new fintech apps, building side income and saving money.

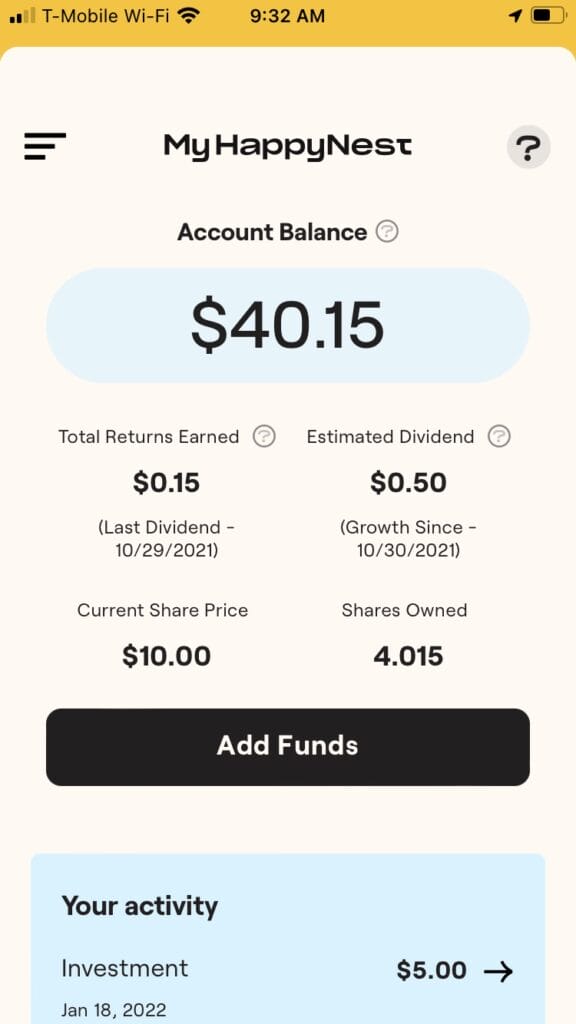

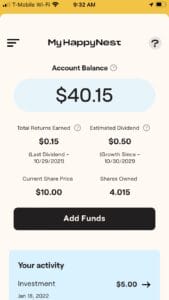

One thing I did in January was experimenting with some Fintech apps. The latest one I’ve been working with is an outfit called HappyNest (not to be confused with the laundry company). I’d heard about them a few months back when I was looking for ways to double my money. I opened up an account using an old referral link and their customer service was cool about honoring the deal even though the terms had long expired.

One thing I did in January was experimenting with some Fintech apps. The latest one I’ve been working with is an outfit called HappyNest (not to be confused with the laundry company). I’d heard about them a few months back when I was looking for ways to double my money. I opened up an account using an old referral link and their customer service was cool about honoring the deal even though the terms had long expired.

HappyNest is a Private Real Estate Investment Trust (REIT). The company was founded by entrepreneurs Jesse Prince and Leonardo Sessa. So far it is still a fledgling operation. The company has only raised about $1.1 million and has just two substantial properties. A Fedex terminal in Indiana and 14% of a CVS in Massachusetts (per the SEC). So, they’re still looking for capital to scale up their business.

Their tech stack works pretty well. In fact, their smart phone app has a feature that lets you round up your purchases on your credit/debit card and invest the difference in HappyNest shares. Their shares also pay about 6%, which should keep pace with inflation.

So far I’ve got about $40 bucks into the service. I’m targeting getting $100 into the service by December of this year. I would go harder on HappyNest, but the lack of a broad real estate portfolio and relatively slow fundraising (roughly $550,000 for 2020 and 2021 each) makes it difficult to justify the risk of adding more capital – especially when you consider the hundreds of REITs available in current equity markets.

If you want to get into HappyNest, they are offering a $10 for $10 sign up offer. You can get the offer here.

I’ve scan all my receipts. Since receipt scanning is trading data for money, most of the apps are slow payers, but I am seeing some fruit. The issue is most of them aren’t paying much. And, when they do, its often in Amazon giftcards instead of cash.

So I’ve managed to build up a bit of credit in Amazon. This is good, but what I really want is stocks and bonds. By and large you can’t buy those on Amazon.

I’ve asked around but nobody seems to know how to convert Amazon credit to marketable securities.

In term of extra income apps, what is working is Earn App. I’d installed it a while back on a lark. When I checked it last week, to my surprise I had like $11 bucks in the service. Its been paying me for my used bandwidth by about $1 per gigabyte. Amazingly, it actually pays what it says. This is far better than some of the other things I’d been experimenting with. I’d give it a try => the sign up link is here.

In case you want a handy list of apps that will actually give you money, here it is:

I’d take a few hours and get all of them installed.

If you know of any other solid passive income players, I’d love to hear about it.

I’ve also been working on building my savings up to $1,000. Right now I’ve got $851.69 and I’ll probably have the goal done by the end of the month. Here is the savings tally:

I’m frankly worried about inflation. Late last year, I read several econometric studies projecting 12 to 18 inflation rate numbers for selected commodities, so we could easily see more than 5% to 7% overall inflation in 2022. At this point none of the options on the table for where to stash the emergency funds are good. Certificates of Deposit and checking accounts are paying interest rates of something like 0.05% here in Oregon. Other options like stock and crypto are too volatile, and are likely in a bear market. Even traditional alternatives like bonds have taken it on the chin.

At this point I’m going to try and find the highest yielding money market account possible and just stash the cash there – then pray that the Fed gets inflation under control soon. This is a terrible plan, but it is the most workable one I can think of.

If you want more on building wealth, read these:

Savings And Side Income Ideas You Probably Haven’t Thought About

Our Top Ways To Make Extra Money

December Net Worth – Drooping Assets and Living Off The Land

Readers,

I’ve been thinking seriously about what I can do to better build wealth – and I thought I’d put it out there.

What’s been the #1 driver of your wealth?

Stocks? Real estate? Saving? 401(k)? Beanie Babies?

Leave a comment below.

This posting is basically a list of apps that let you sell your data. I’ve been looking around for a list like this for a while, but I couldn’t find one. After endless hours of internet searches, I opted to just make one for those who might be looking.

All the apps in this list are designed for either the iPhone or Android as well as Mac or Windows OS, and they actually work. By work, I mean the technology stack is functional, the smartphone apps work as advertised, and the applications pay as promised. They’re also all passive. By passive, I mean after set up, they don’t require a whole lot of ongoing work.

So, here is the list of apps that let you sell your data. I’ve tried all of them. This list is based on my personal experience.

I like invisibly. It’s a straight-up, sell-your-data-for-a-small-amount-of-money type of company. You create an account and let them monitor your spending and social media transactions. It bundles your data, sells it, and then gives you a cut of the sale. You install it on your desktop. Payout is via Paypal once you get to $5. So far I’ve made about $3 per month with it. Its payment is based on how often it sells your data, so you have to check every few weeks. That said, it’s basically set it and forget it. Then check back 6 weeks later and collect. Note, as of 7/7/2022 it appears that Invisibly has ceased their operations.

I like invisibly. It’s a straight-up, sell-your-data-for-a-small-amount-of-money type of company. You create an account and let them monitor your spending and social media transactions. It bundles your data, sells it, and then gives you a cut of the sale. You install it on your desktop. Payout is via Paypal once you get to $5. So far I’ve made about $3 per month with it. Its payment is based on how often it sells your data, so you have to check every few weeks. That said, it’s basically set it and forget it. Then check back 6 weeks later and collect. Note, as of 7/7/2022 it appears that Invisibly has ceased their operations.

Next on the list of apps that help you sell your data is Reklaim. Reklaim is an interesting and scrappy little growth company. It’s a publicly-traded penny stock. Right now, its shares go for under thirty US and Canadian cents. But, it’s making a lot of good moves. How its model works is you give it access to your spending history, your demographic profile, your smartphone data, and your purchase history, then you get 100 points per week. Once your account hits 1,000 points, you can take the reward in cash or crypto.

Next on the list of apps that help you sell your data is Reklaim. Reklaim is an interesting and scrappy little growth company. It’s a publicly-traded penny stock. Right now, its shares go for under thirty US and Canadian cents. But, it’s making a lot of good moves. How its model works is you give it access to your spending history, your demographic profile, your smartphone data, and your purchase history, then you get 100 points per week. Once your account hits 1,000 points, you can take the reward in cash or crypto.

![]() Nielson Opinion Rewards is in this list of apps that let you sell your data because this is a classic well-designed, and robust platform. The guys at Nielson have got the onboarding process pretty well-ironed out — and it pays reliably via Paypal. It takes a bit of doing to get the software installed on your phone. However, once its on, the software works well. You’ll get about $5 every couple of months.

Nielson Opinion Rewards is in this list of apps that let you sell your data because this is a classic well-designed, and robust platform. The guys at Nielson have got the onboarding process pretty well-ironed out — and it pays reliably via Paypal. It takes a bit of doing to get the software installed on your phone. However, once its on, the software works well. You’ll get about $5 every couple of months.

![]() This is actually isn’t a smartphone application, but I’m including it here because it works and it pays. You install it on your laptop/desktop browser and you get points each day you visit social media. Upvoice awards 20 points per day, per social media platform. You can then select gift cards if you want to get paid. It nets out to something like $3 per month. Pays you in Amazon or other gift cards. Note: as of 7/7/2022 Upvoice appears to have shut down their operations.

This is actually isn’t a smartphone application, but I’m including it here because it works and it pays. You install it on your laptop/desktop browser and you get points each day you visit social media. Upvoice awards 20 points per day, per social media platform. You can then select gift cards if you want to get paid. It nets out to something like $3 per month. Pays you in Amazon or other gift cards. Note: as of 7/7/2022 Upvoice appears to have shut down their operations.

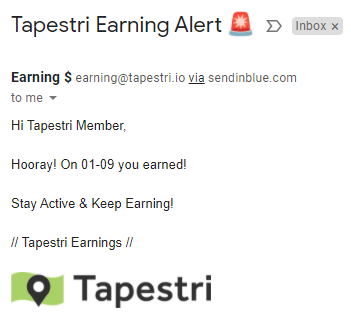

Tapestri is an app owned by Chicago company Complementics. The app basically uses your phone to generate movement data about you, then Complementics sells the anonymized data to brands, hedge funds, and advertising agencies.

Tapestri has been paying me about 16 cents a day. It’s not huge money maker, but since you’re basically trading your location data for money, it’s a fair deal. It also sends you emails every time you earn. It’s a small amount of cash, but hey, nothing like an email saying, “Hey, you’ve got money.” You’re looking at roughly 4 to 5 bucks per month. It pays via Stripe when your balance reaches $10.

This is an interesting outfit. It’s not a company at all, rather Swash is a data union. A data union is basically a way of pooling data between various parties and collectively monetizing it. How Swash works is you install a browser extension and let it read your browsing history. You then get paid in Swash tokens. I’ve had it installed for a couple of months and I am making like 3 units of swash per month. This is pretty much no money at all. A Swash unit is worth about 8 cents. That said, its better than nothing and it costs nothing to install and run.

This is an interesting outfit. It’s not a company at all, rather Swash is a data union. A data union is basically a way of pooling data between various parties and collectively monetizing it. How Swash works is you install a browser extension and let it read your browsing history. You then get paid in Swash tokens. I’ve had it installed for a couple of months and I am making like 3 units of swash per month. This is pretty much no money at all. A Swash unit is worth about 8 cents. That said, its better than nothing and it costs nothing to install and run.

Tartle is another interesting data union. It’s the brain child of Alexander Ramsay McCaig (Linkedin) and, like Swash, its not a company rather its a data union.

Tartle is another interesting data union. It’s the brain child of Alexander Ramsay McCaig (Linkedin) and, like Swash, its not a company rather its a data union.

The model works like this: You upload a bunch of information on Tartle’s platform. Tartle then bundles your data and pays you whenever it is able to make a sale. Though there are issues with the notifications and set up. And its marketing and operations also need improvement. That said, it’s a good idea. However, I think it is still new and have limitations on its labor power. Tartle also has a super low payout — like 2 cents for a series of 10 to 20 questions. My account balance is at a buck seventeen.

You have to generate data to get paid for it. That means you pretty have to live on the internet. In this list of apps that let you sell your data, you’re only getting paid if you’re actively using data on the web, or buying stuff. So if you live off the grid and exclusively use cash, these apps are probably not going to help you.

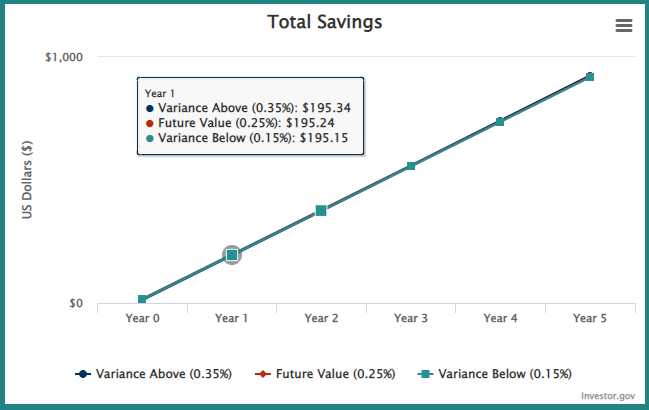

You might be thinking “so what? These apps pay nothing, it’s not worth my time.” Even running all of these on your phone and desktop/laptop is going to bring in just between $15 to $20 cash per month. Factoring in inflation, that’s not much these days.

However, if you get your act together and place the income on the market or sock it into your savings, it does add up.

Here is what the five year saving trajectory looks like:

Here is what the amount would like if you invested in stocks or bonds and got 7 percent annualized returns.

Both charts assume you’ll start with $15, get $15 each month, and compound it over 5 years. They also assume savings account interest rates at .10% and investing account interest rates at 7%. The bottom line is that consistently selling your data can add up to bigger things over time.

Even if the app doesn’t pay you in US dollars, it’s still to your benefit. For example, if you get credit at Amazon you can use it to offset your grocery bills. Or, if the app pays you in cryptocurrency you can use that to build your wealth.

For more practical articles on building wealth, read these:

Getting Ahead On $600 Per Month.

James’s December Wealth Update

Our Top Ways To Make Extra Money

So, it’s the new year season. Around new years many people focus on getting their personal financial house in order, but a lot of people are also focused on improving their personal relationships. So, if your goal is to improve your personal relationships, you’ll have to take some action.

Here are four ways to do this:

1. Deciding to do it – being intentional. You need to make a conscious decision to make the relationship better.

2. Paying attention & being present. When you’re spending time with them put your phone and distractions away.

3. Appreciate the totality of who the person is. Everyone has good points, you just have to focus on them.

4. Adore and respect the person. Support their bigger dreams and life goals.

Good healthy relationships matter a lot. Per Harvard, people with strong relationships are happier, live longer and have fewer health problems (proof here). Relationships are also conduits for knowledge, as well as for capital and opportunities. So, if pays to make them a priority.

And as a bonus if your goal is to improve your personal relationships, these other articles from the Dinks might help point you in the right direction.

The Grass Is Greener Where You Water It

How To Tell Your Spouse They Don’t Make Enough Money

You cannot copy content of this page