James Hendrickson is an internet entrepreneur, blogging junky, hunter and personal finance geek. When he’s not lurking in coffee shops in Portland, Oregon, you’ll find him in the Pacific Northwest’s great outdoors. James has a masters degree in Sociology from the University of Maryland at College Park and a Bachelors degree on Sociology from Earlham College. He loves individual stocks, bonds and precious metals.

For those of you longtime readers of the DINKs, you’ll know I’m usually pretty excited about up-and-coming fintech companies.

The latest company I got excited about was the Small Business Exchange (SMBX). The SMBX is basically attempting to reform small business finance by replacing bank lending with crowdfunded bond marketplace options.

SMBX Works – It Makes Money

SMBX works. From the standpoint of observing their business eight or so months down the line – it’s totally been working from an investor standpoint. I’ve bought maybe $10 or $20 worth of bonds per month since I started last December. Most of the bonds pay between 6.5% and 8%. Most have amortization schedules that return principle and interest over the life of the bonds, so there isn’t any large repayment at the end – similar to how most conventional bonds are structured. This means your payments are higher – which is good for investors. And, every few days I get an email telling me I have a principle and interest payment that hit the balance in my SMBX account. There also haven’t been any defaults or other nonsense. So…SMBX works.

My SMBX payment notifications.

I have to admit, it’s nice to check email after my morning routine and see a payment notification. Nothing wrong with that at all.

One of the companies I invested in even sent me a nice thank you card.

SMBX Works, But Might Not Meet Its Organizational Mission

From an investing standpoint, SMBX works. However, in terms of SMBX’s mission to transform lending markets, it’s not clear if they’re moving enough volume to make this happen. The platform only has about three companies which have active bond offerings, and only about 21 closed offerings. Twenty four total offerings isn’t enough to move markets.

That said – if SMBX can meet it’s organizational promise it could be a very interesting in the long term. Small businesses often have trouble getting affordable capital. And, not only that small busineses run by minorities typically have even more trouble. This is often due to the types of businesses they run and to lack of things like extensive bank account history, formalized accouting receipts, etc. In theory the crowdfunded bonds model should fix these issues. Only time will tell.

Incidentally, if you have all your financial bases coved (emergency fund, debt paid off, etc.), I recommend you give these guys a spin. Their website is => here.

The phrase, “You can lead a horse to water, but you can’t make him drink” means you can give someone an opportunity to do something, but you can’t force them to if they aren’t interested.

Case in point: Coinbase.

Coinbase bucks.

If you haven’t heard of Coinbase, it’s an up and coming – recently IPO’d – cryptocurrency brokerage.

Cryptocurrency and the whole economic infrastructure around it is an emerging part of the economy. The crypto sector is commanding massive and global entrepreneurial interest. And – at the rate capital is flooding into the sector, it’s just a matter of time before blockchain technology becomes commonplace.

Coinbase is really well-positioned for beginners to get involved in crypto. You get five bucks for signing up (these links are all over the web, you just need to run an internet search to find the $5 sign-up bonus), and they have a rewards system that basically gives you free cryptocurrency for watching some videos. As an entry point to get into crypto, it’s basically perfect.

Yet, when I talk with people about it, a lot of the time they just make noncommittal statements like “Oh yeah, that’s cool”, or “sure thing, I’ll get right on that”. When it’s obvious they’re just not interested. I just shrug my shoulders and when the next rewards opportunity crops up on Coinbase, I collect my free crypto.

It just goes to show, you can put money-making opportunities in front of people, but they won’t necessarily take advantage of them if they don’t care.

For more great dinks finance articles, read these:

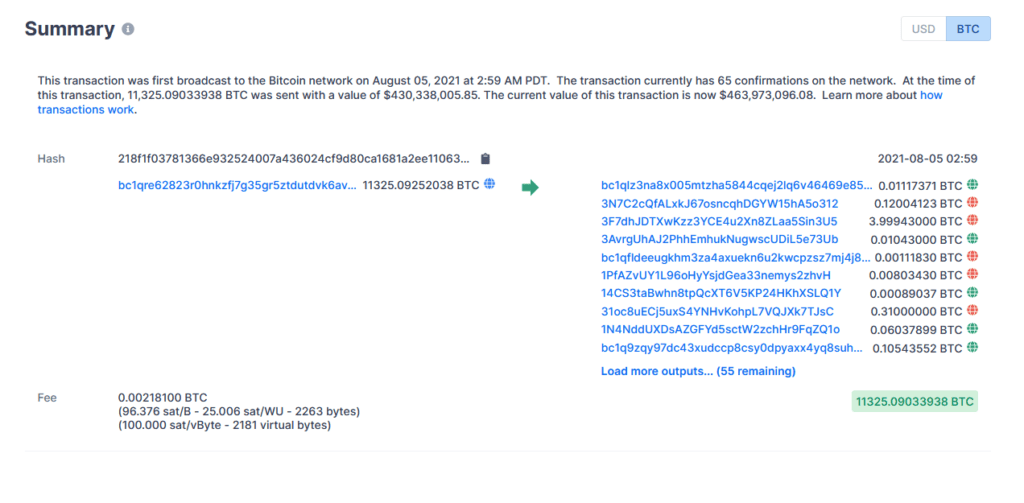

Unless you’re hanging around the Crypto space in blockchain.com you probably missed this. It’s a $430 Million transaction in bitcoin.

I’ve been noticing more and more recently that the crypto space is sucking up entrepreneurial energy and capital. There just aren’t that many transactions worth $430 Million in the US economy.

Notably, this transaction had a fee of around $81 bucks. That’s dirt cheap for the amount of money that’s being moved.

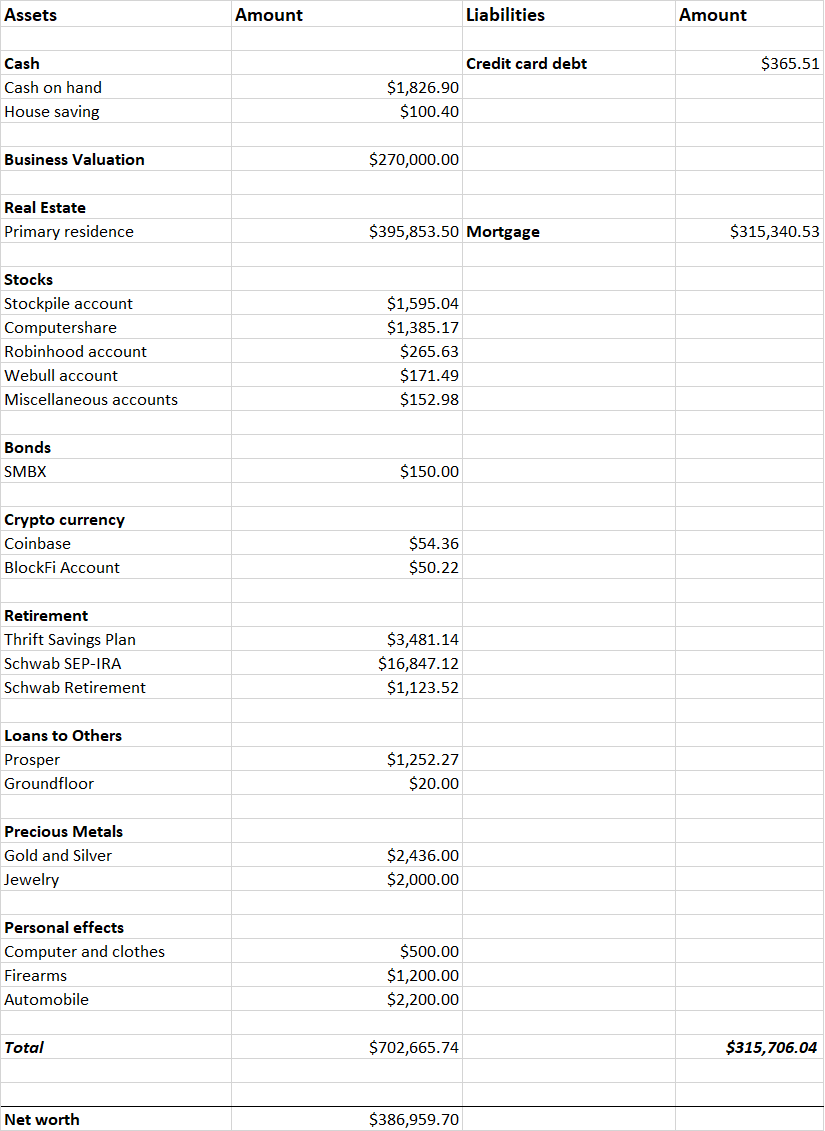

Okay so I sat down and calculated my net worth last weekend.

I’m up 2.48% from May. July’s wealth total was $386,959.70, up $9,377.09 from May’s $377,582.61.

The major long term drivers of the growth have been:

A. Appreciation of my condo unit. The value of the condo increased by about $1,000.

B. Growth of my stock – I was able to make a substantial deposit of around $4,000 into my SEP-IRA. I bought shares of APO, MNST, and took a larger position in the Vanguard S&P 500 index. All these are up at least 20% since I’ve bought them.

C. Debt reduction: I was able to get about $6,000 worth of credit cards paid off. And the amount owed on my mortgage has been ratcheted down a bit also.

Here are the specific figures:

James bucks in July 2021

There are a couple of things I’ve done so far this year that are working.

Streitwise

I put an investment into Streitwise – it’s a semi-private commercial reit. Its been reliably paying since I purchased it six months ago. Its become a bit less interesting for small investors recently. They upped their minimum from about $1,000 to $5,000. But its been sending its dividends of $0.21/share or 8.4% annualized – so that’s been working. They’ve also managed to survive the worst of Covid related commercial real estate crunch, so that’s good news.

SMBX

Also, I’d put a limited position into a small business bonds marketplace – TheSMBX, which has turned into a neat little operation. I’ve been putting as much money into them as my cash flow comfortably allows. The bonds are yielding 7.5% to 8.0%, which should give me some decent returns over inflation. I’ve got my portfolio up to about $150 in that platform. They’ve been a bit slow to add in new companies looking for funding, I think because they’re still building their assets under management.

“Get Stock For Signing Up” Type Offers

I’ve been scouring the web for “get stock for signing up” type offers – I’ve signed up for virtually everything I could find. I’ve also been working some some of my friends to get referral stocks. This has given me maybe about $500. It’s not a huge money maker, but if you’re cash constrained, its a good wealth building option. Companies to check out in this space are Robinhood, Firsttrade, Public and SoFi.

BlockFi

Per crunchbase, BlockFi is a secured non-bank lender that offers cryptoasset-backed USD loans to cryptoasset owners. The story there is they offer something like 7.5% interest rates if you deposit funds with them. I don’t entirely understand what they’re doing to generate returns higher than 7.5%, so I’ve only got about $50 in the platform.

The Main Takeaway

Here is the takeaway for my July net worth update. I recently started tracking my net worth – and the results have been incremental improvements on a quarterly by quarterly basis. I think the main point here is pretty clear, if you spend your time on building wealth, eventually you’ll get results.

For more on net worth and building wealth, read these

The more time you spend on the planet, the more you realize that even smart money is fallible.

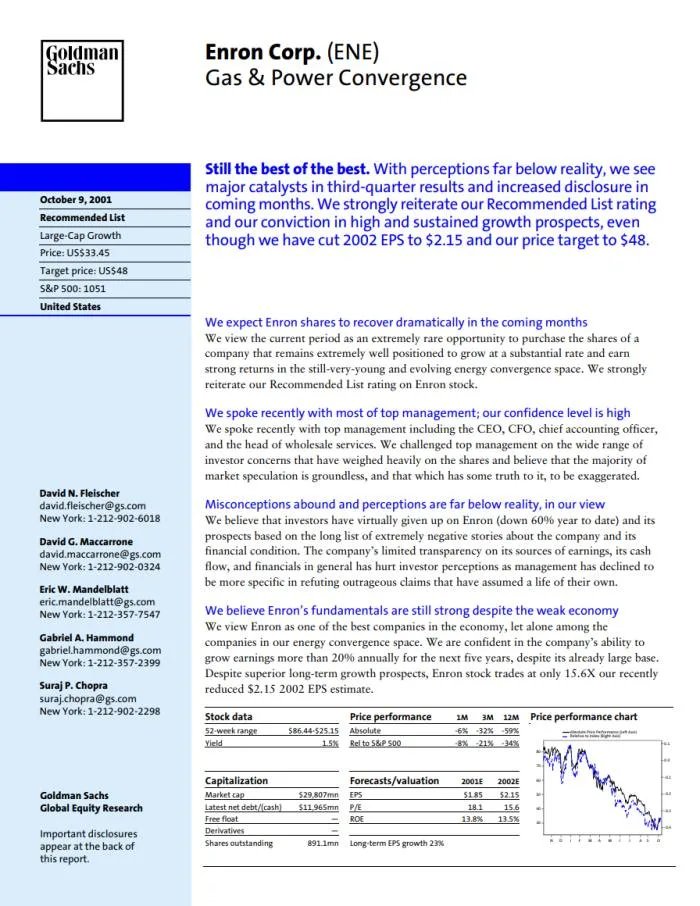

Here is a graphic that is making the rounds on the web. Its a stock recommendation issued by Goldman Sachs on the now defunct Enron Corp.

In case you’re not familiar with Enron, here is the story. The Enron Corporation was an American energy, energy commodities, and related services company based in Houston, Texas. In 2001 Enron was shown to have committed institutionalized and systemic accounting fraud. Since known as the Enron scandal, the company’s name has become synonymous with willful corporate corruption. The scandal also brought widespread scrutiny of corporate accounting practices and was a strong factor in the 2002 Sarbanes-Oxley act. Enron’s fraud also lead to the dissolution of Arthur Anderson, which was Enron’s accounting firm.

The bottom line is: even the smart money is fallible. The highest paid analysts can and do make mistakes.

It’s definitely summer here in Portland, Oregon. Last weekend was the hottest on record. The temperature hit 116. It was so hot in fact, that the multivitamins in my apartment melted. As a result of the heat, a ton of people are buying summer stuff – clothes, furniture, etc.

Last week I was at a Fred Meyer (which is a local Kroger chain) and outdoor furniture and camping gear were selling like hotcakes. Fred Meyer had these 10 dollar cheaply made lawn chairs on sale.

These chairs are a classic example of what economists call a “false economy”. If you’re not familiar with the term, per Websters, a false economy is basically something that costs less at first but results in more money being spent in the long run.

These lawn chairs look great for $10, but they’ll fall apart in a few months. I know because I’ve seen some junked on the side of the road and I’ve owned a couple myself. The joints break down pretty quickly and the cloth rips easily.

So, people, if you’re going to be buying summer camping gear, get stuff that won’t fall apart. Buying cheap junk means you’ll have wasted the money you spent in the first place and you’ll just have to buy it again later on. Instead, go with something that’s more durable and a better value. It may cost you more upfront, but in the long run, it’s better for your wallet.

For more great articles from the dinks, read these:

This is a quick posting for everyone working on a large savings goal.

If you’re saving – don’t give up.

Don’t Give Up. Don’t quit saving out of the silly belief that you’ll never have enough to meet your goal. Forget focusing on the big figure you need to get to. Instead, work it out using a calculator and break down what your weekly, monthly and annual savings goals should be. Focus on these smaller numbers.

If you do this, you should be able to build your retirement or other savings accounts step by step.

Have ever wondered why it’s so hard to get rich? In America, we love and worship rich people. Guys like Warren Buffet and Elon Musk are celebrated personalities. We also value and appreciate the actions of people like Richard Branson or Oprah Winfrey. So, if being rich is so awesome, why aren’t more people wealthy?

Consider the numbers. There are about 128 million households in the US, but as of 2020 there were only 11.6 million of those were worth over 1 million bucks. This means that only 9% of American households have crossed the seven-figure line. When you think about it, it’s even rarer for people working on their own to achieve net worths higher than $1,000,000. For whatever reasons it’s uncommon to become really rich.’

So, why is it so rare to become wealthy? Well, there are substantial barriers to getting rich.

1) Economic Change: Wealth is often generated via investment vehicles such as stocks and bonds. While the performance of historical U.S. equity markets has been very good, there is no guarantee that future trends will continue. As an example of the impact of change on becoming wealthy, a lot of people were left high and dry when the tech bubble crashed in 2001. Similarly, many folks hoping to get rich quickly in real estate lost a great deal of money when the market contracted in 2007. Also, unpredictability in mortgage and interest rates can sabotage the wealth-building processes even absent a boom.

Similarly, economic fortunes can be hindered by failure to adapt to dynamic economic conditions. For example, in the early 1800s, England was hit with a sustained depression in the price of agricultural commodities. This meant that landowning families who hadn’t diversified experienced a severe decline in their wealth and political power.

In short, economic trends change quite frequently. This makes it difficult to effectively generate a long-term plan to achieve great wealth. And, when one has achieved some wealth, economic conditions or technological change can wipe out that fortune.

2) Culture of Debt: When I say culture, I mean that debt has seeped into American psychology. At this point debt is almost a psychological mandate, our culture seems to dictate that to live a normal life you must have debt. If you look on TV it’s easy to see this: there are tons of advertisements for mortgages, rent-to-own schemes, payday loans, etc. In this sense, debt has become a part of what’s normal and every day.

Not only is debt a part of everyday norms, it’s also a part of our life cycle. Consider major points in the typical American life span. First, most people take on some level of borrowing to cover going to college. After education typically comes marriage. Weddings can cost thousands, so people put the cost of their wedding on their credit cards. After marriage, a lot of couples buy a house, and along with the house comes a mortgage. The next step is children and more credit card debt. Basically, debt is often incurred at important parts of the life cycle, education, marriage, children, etc.

It goes without saying, but the more debt you’ve got, the less money you have to grow your capital. Thus, debt tends to hinder one’s ability to get rich.

3) Consumerism: Consumerism is the theory that the consumption of goods is economically desirable. It’s also a model for economic production. One major barrier to building wealth in today’s economy is that the US is geared towards consumerism. On a big picture level, we tend to focus our economic activities around manufacturing and buying low-quality cruddy consumer goods. Unfortunately, these aspects of macroeconomic activity translate to individual behavior. People often choose to spend their money improving their consumer goods rather than saving to generate capital to start a business. Thus, consumerism and a consumer-oriented society is a barrier to building wealth. We buy crap instead of saving.

4) Peer Pressure: Honestly, I’ve noticed that the more successful one becomes, the greater the subtle degree of peer pressure NOT to achieve. It’s hard to say, but most people are actually pretty mediocre. Thus, there may not actually be a lot of support from one’s friend to achieve real wealth, in fact, they may discourage you. This is because your own success reveals their own inadequacies.

5) Psychological Barriers: Think about it for a second. Have you ever conceived of achieving a very high degree of wealth? I don’t mean sitting back and daydreaming about it, but really sat down and turned the idea over in your mind? Probably not. Probably most people haven’t. Most people just don’t think about achieving wealth and accordingly don’t decide to make the formal commitment to becoming rich. Considering the prevalence of laziness and cynicism in American society, it’s clear there are substantial psychological barriers to getting rich.

6) Taxation: The average effective income tax rate in the US is 13.3% (1). All things being equal, this means that 13 cents on your dollar are not going to make you wealthier. Taxes aren’t all bad, they pay for defense, police, schools, roads, and other good things. However, purely from the standpoint of barriers to wealth, it’s a lot easier to get rich when you’ve got 100% of your dollars working for you. When you’ve got 13% of your income going to taxes, that’s a drag on your ability to achieve wealth.

7) Discrimination and the Old Boys Network: In some parts of the US there are organized social resistance to minority populations achieving wealth. Just to illustrate this with a couple of examples:

1) In the deep South, state and county Jim Crow laws prevented African Americans from full economic participation. This is well documented.

2) In some rural parts of Mormon-dominated areas in the country today, economic discrimination is practiced against Catholics by members of the Church of Latter Day Saints. This is less well documented but is nonetheless true.

3) Economic discrimination against Jews was common in many parts of the US in the first half of this century. This is also a matter of historical record (1).

If you live in some environments, there can sometimes be organized local resistance to your economic success based purely on ascribed characteristics like race or religious belief.

8) Chance. Pure random chance. The world is a probabilistic place. This means that random things happen; hurricanes acts of God, heart attacks. Basically random things happen every day that are outside of anyone’s control but nevertheless impact your wealth building.

So, just to sum it up, there are lots of barriers to getting rich in the US. The good news however is that lots of people do manage to make a great deal of money in America, so while difficult it is entirely possible to make a fortune. In fact, there are millions of millionaires, with the right steps you can become a millionaire in twenty years, too. You’ve just got to make it happen.

Here is a tip for you. If you have grocery coupons, but you forgot to use them during your shopping trip. Bring your coupons and your receipt the grocery store.

The customer service desk may be able to credit your coupons to your rewards account, or they might be able to give you cash back.

Brain Drain is Happening In South Africa – Short Sell It

Everyone knows about Elon Musk – he’s one of the most famous entrepreneurs in the US. But, were you aware that he’s South African? Musk however, is not the only major entrepreneur of South African descent in America. Energy drink entrepreneurs Rodney Sacks and Hilton Schlossberg are also South African. Other notables are Roelof Botha, a partner at Sequoia Capital, entertainer Trevor Noah and Paul Maritz, CEO Of VMWare.

A lot of the reason South Africa emigres are in the US is due to high crime, corruption and aggressive racism in their native South Africa. And it’s no surprise, prosperity is difficult if personal safety can’t be assured and people hate you for the color of your skin. South Africa will have challenges with long term economic decline if it can’t fix it’s internal crime and racial conflict issues.

A good way to profit from this might be to short ETFs with heavy exposure to South African government securities or the South African economy.

Are Commercial Banks At Risk Of Becoming Dinosaurs?

The long term economic dominance of commercial banks is becoming increasingly less clear.

The crypto space is tremendously vibrant, in comparison to the rather moribund and rule bound commercial banking sector. I read Satoshi Nakamoto’s original white paper a while back and was frankly impressed with Nakamotos conceptualization of the blockchain. While the technical aspects of blockchain construction are beyond the scope of the this posting, what they basically allow is peer to peer financial transactions. In theory, this eliminates the need for third parties (e.g. banks) to move money. This means its safer, cheaper and easier to move money with a blockchain.

Also, lending & economic activity is increasingly vibrant in the crypto space. Companies like BlockFi, Nexo, and Celsius are all offering interest rates of at least 5%, This is compared to the average of .06% commercial banks offer on savings accounts. That’s a ratio of 83:1. Granted, cryptocurrency and cryptolending are unregulated, so it’s riskier, but even if regulation does halve the value of the crypto interest rates, you’re still looking at 40:1 ratio. If this keeps up, capital will continue to flow into the crypto space.

The dominance of crypto relative to traditional commercial banks is also shown in new business formation. New commercial bank formation has declined dramatically in the US (clicky) – with less than one new commercial bank starting per year. In contrast, Crunchbase reports there have been 837 new cryptocurrency start ups since 2017 (here).

The cryptocurrency space is extremely volatile, but one possible way to make money in this part of the economy would be to screen the various cryptolenders and see which ones might merit some investing/lending capital. If you want to do this, here is a list of five red flags of fraud.

To get you started, here is a list of some of the crypto lending companies:

Hello All,

Hello All,

Everyone knows about Elon Musk – he’s one of the most famous entrepreneurs in the US. But, were you aware that he’s South African? Musk however, is not the only major entrepreneur of South African descent in America. Energy drink entrepreneurs Rodney Sacks and Hilton Schlossberg are also South African. Other notables are Roelof Botha, a partner at Sequoia Capital, entertainer Trevor Noah and Paul Maritz, CEO Of VMWare.

Everyone knows about Elon Musk – he’s one of the most famous entrepreneurs in the US. But, were you aware that he’s South African? Musk however, is not the only major entrepreneur of South African descent in America. Energy drink entrepreneurs Rodney Sacks and Hilton Schlossberg are also South African. Other notables are Roelof Botha, a partner at Sequoia Capital, entertainer Trevor Noah and Paul Maritz, CEO Of VMWare. The long term economic dominance of commercial banks is becoming increasingly less clear.

The long term economic dominance of commercial banks is becoming increasingly less clear.