James Hendrickson is an internet entrepreneur, blogging junky, hunter and personal finance geek. When he’s not lurking in coffee shops in Portland, Oregon, you’ll find him in the Pacific Northwest’s great outdoors. James has a masters degree in Sociology from the University of Maryland at College Park and a Bachelors degree on Sociology from Earlham College. He loves individual stocks, bonds and precious metals.

“Let me put it bluntly: anyone who says money isn’t important doesn’t have any! Rich people understand the importance of money and the place it has in our society…poor people validate their financial ineptitude by using irrelevant comparisons. They’ll argue ‘Well, money isn’t as important as love’…What’s more important, your arm or your leg? Maybe they’re both important”.

Since we dinks are hard at work today, we wanted to let you know about some handy money saving tips from your friend and our’s, The State of Florida!

The Florida has a handy document, called 66 Ways To Save Money, that details ways you can save money buying a car, getting a checking account or negotiating with your power company!

It’s a quick read and has some great tips, so feel free to check it out HERE.

P.s. as a bonus, if you’re looking for ways to save, consider checking out Rebate sites like rebatefanantic.com, or swagbucks.com. They’re not sexy, but are tried and true ways to save.

If you ask the average investor out there what metal they’d recommend to diversify a portfolio, they’ll usually reply, “Gold”. In 2020, gold reached historic highs as investors flocked to it as a hedge against market uncertainty. Yet, gold’s highs were some time ago. As investors have awakened to the possibility of higher interest rates, gold has become less and less attractive. Higher interest rates are bad for gold because gold doesn’t yield any interest. Putting your money in gold in this environment is a recipe for sub-par performance. There’s a smarter way to play the metals game. According to research from JPMorgan, we are in the first innings of a commodity supercycle. At a time when commodities are experience severe supply constraints, there is no reason why investors should restrict themselves to gold. I suggest investing in the rare metals bull market. The rare metals bull market has been spurred on by the recovery of oil to pre-pandemic highs. As global mining and emerging markets have rebounded, rare metals have received a boost and their outlook is especially bright. In this article, we will discuss how to take advantage of the rare metals bull market.

Silver, Owned By Warren Buffett

One metal I like right now is silver. This is because silver has extensive industrial uses, unlike gold. Warren Buffett is famously averse to gold, but he has played the silver game. When he bought silver in 1997, it was at a time of high stock market valuations. He analyzed the silver market and discovered that there was a shortage of silver relative to demand. At the time, nobody really mined silver on purpose. It was essentially a by-product of mining other metals. This led to a huge imbalance in the silver market and at some point, there would be a reckoning. Buffett purchased 130 million ounces of silver and went on to make a $97 million profit.

Silver Has Historically Outperformed Gold

An interesting fact about silver is that it has outperformed gold in five of the last six gold bull markets! At present, we are again in a period where stock market valuations are extraordinarily high. There is evidence that silver has entered a bull market. In a bull market, prices typically remain higher than their 150-200 day moving average. That gives you an indication of the dynamics at play. As the global economy recovers, demand for silver will rise in response to the reopening of industry. Remember, silver has extensive industrial applications.

Silver’s outperformance is different to that of gold. Silver was up 70% in 2020 at a time when everyone was talking up gold. Since gold’s 2020 highs, gold has been in a funk, with its price declining and experiencing a lot of volatility. When an asset experiences this much volatility, it’s usually because investors’ conviction about that asset is shaky. Every bit of news either spooks them or sends them over the moon.

One thing that makes silver so interesting is that because gold is usually touted as a safe haven against economic uncertainty, gold is unlikely to perform well as the economy recovers. Silver, however, will do well as the demand for its industrial applications rises. It’s not surprising then that gold has only risen 4% in the last twelve months, against 70% for silver.

So, How Do You Take Advantage Of The Silver Bull Market?

Answer: Buy some silver. Here are some common ways.

1) Open a precious metals IRA. A precious metal IRA is a special form of self-directed IRA. The reason this your first starting place is IRAs are tax advantaged, they either reduce your taxable income or they reduce the amount of taxes you need to pay on any gains you make. Precious metals IRAs are a specific type of account that lets you buy and invest in precious metals.

The outfit I like in this space is Augusta Precious Metals. You can find them => here.

Once you’ve got account you can fund it and buy silver through the account.

2) Buy shares in a mining company. A lot of mining companies haul silver out of ground as a by product of their operations. Or the alternative is that you can buy shares directly in a mining company that focuses on extracting and producing silver. If you don’t have access to the stock market, get Robinhood and look at PAAS, WPM or CDE. These are three largest mining companies in the US by market capitalization.

3) Get an EFT. Popular ETFs that pertain to precious metals are: SLV, DBS and AGQ. DBS and AGQ track the index price of silver and are a bit cheaper over the long run as their lowered expense ratios. You can also get an TFR through Robinhood.

4) Other alternatives. There are lots of ways to invest in silver other than physically buying it or getting it indirectly via an exchange traded fund or a mine. These other options include derivatives. I am significantly less familiar with these, so your best bet is to check Wikipedia.

Everyone’s personal financial situation is different. Some people are still getting organized, others are in better shape.

So, for many the question is: after you’ve got the basics nailed down, where do you go after that?

For example, after you’ve paid off your high interest debts, have an emergency fund and are sticking to a budget, whats the next step?

Well, there are several priorities you might consider:

1) Home ownership: If you don’t own your home, and are in otherwise in good shape, you should strongly consider buying a home. There are number of benefits to owning your own place. First, you have tremendous tax advantages as the mortgage interest and property tax payments can be written off your taxes. You also have greater autonomy in terms of decorating and remodeling. Owning real estate also provides important protection against inflation and housing can be an important asset when you reach retirement after the mortgage is paid off.

2) Start an investment fund: Various gurus like Loral Langemeier and Robert Kiyosaki argue that you should set up a separate bank account to save up for something entrepreneurial. Consider saving five or ten thousand dollars and investing that money into a solid asset class. You might consider something like buying index funds in the stock or bond markets or purchasing an annuity. If you are looking for a bit of a higher return, you could get into something like lending money directly via an outfit like Prosper.com or buying shares of individual companies directly in a brokerage account.

3) Start saving for retirement: Saving for retirement is sometimes a bit dull, but you’re better off with full retirement accounts. This is because traditional IRAs, ROTH-IRA and SEP-IRAs all have tax advantages. For example, investments held in ROTH-IRAs compound tax free. For most dinks, retirement is a long way off, which is actually an advantage to you. The longer off retirement is, the more time you have for your investments to compound.

4) Start a small businesses: There are a number of proven business models that you could get involved with. Among these are franchises or rental real estate, etc. Starting a side business can take a great deal of time, but the rewards can be substantial. Just to illustrate this with a personal example, my brother has a number of rental houses which give him several thousand dollars per month in income. The point here is that a proven small business can really improve your bottom line and give you a great chance to build wealth.

Good luck, if you’ve gotten to the point where the basics are nailed down, you are way ahead of a lot of people.

Here is a speech from the late Nobel Prize winning economist Milton Friedmann. Its an excellent explanation of the root causes of inflation, its effects on your income, and what can be done to combat it.

This is important today as inflation is starting to reemerge (clicky).

If you’re interested in understanding personal finance, you should probably develop at least a rudimentary understanding of how inflation works. So, please do watch the video.

For more great articles on this topic, read these:

Here is a brief, but insightful video on spending money by Milton Friedman. Since Friedman was one of America’s most famous economists, so its worth taking a bit of time to look at. His thoughts on spending money have some political implications, but at 1.46 run length its worth a watch for the loads of common sense it contains.

I drive around rural Oregon a lot these days. I live in Portland and commute on a semi-regular basis to the Oregon coast. It’s interesting going from the relatively affluent Portland suburbs to the poorer rural parts of the state. It usually has me wondering what it means to be poor versus rich. So, for this article, I did some research and came up with an answer.

One popular source on the subject of poor versus rich is Tom Corley’s study of rich habits. His study is outlined in his popular book: Rich Habits: The Daily Success Habits of Wealthy Individuals. His study is also on his website, which I looked at for this post.

Poor Versus Rich Differences

When it comes to the poor versus rich, there are a lot of non-monetary differences:

Relative to the rich, the poor are:

Significantly less likely to believe wealth is part of the American dream (20% versus 96%)

More likely to say the American dream is about homeownership (51% versus 5%)

Less likely to believe that bad habits create detrimental luck (9% versus 76%)

More likely to believe fate dictates financial circumstances (90% versus 10%).

The poor also:

Are more likely to lease a new car (45% versus 6%)

Less likely to balance their checkbooks every month (32% versus 94%)

More likely to carry balances on their credit cards (90% versus 5%)

Often have more than one card (77% versus 8%) and more often transfer balances (87% versus 0%)

Are less likely to know their credit score (5% versus 72%).

Educational differences are evident.

The poor are more likely to lack a college degree (17% versus 68%)

Fewer poor people say they like to learn new things (5% versus 86% )

Poor people are less likely to read for education, career, or self-improvement (2% versus 88%).

Unsurprisingly, when looking at poor versus rich, the poor save and invest less.

The poor save far less than the rich. Just 19% are saving for retirement, compared to 100% of the rich.

The poor also save less of their income than the rich (5% versus 100%).

The poor in Corley’s study is also:

Less likely to volunteer 5 hours per month (12% versus 72%)

Less likely to vote (16% versus 83%)

Less likely to be involved in a charity or non-profit (6% versus 67%).

Work differences also contrast the poor versus the rich. The poor are:

Less likely to wake up 3 hours before their workday starts (3% versus 44%)

Less likely than the rich to say they do more than their job requires (17% versus 88%)

Less likely to work 50 hours a week (43% versus 86%)

Are less likely to be small business owners (8% versus 51%)

Less likely to like what they do for a living (4% versus 86%).

If you’re an aspiring wealth builder, or you are looking at improving your personal financial situation Corley’s work provides some clues.

1. Adjust your mindset to develop a sense of mastery 2. Avoid high-interest debt 3. Get educated and participate in ongoing knowledge building 4. Get involved in civics 5. Work a lot.

Most articles looking at his data don’t really explain who he talked with. For this study, Corley interviewed 233 wealthy individuals and 128 poor individuals between March 2004 and March 2007. The rich group had a minimum of $160,000 in annual income and $3,200,000 in net worth. The poor group had less than $35,000 in income and $5,000 in assets. Most of the rich group were self-employed entrepreneurs. Most of the poor group were employees. His research methodology is here.

Corley’s data is substantially better than most articles on studies of the rich because it is more than just opinion. However, the data isn’t perfect. It doesn’t say much about investing patterns or the middle class. And, it didn’t use statistical methods of selecting participants for the study – so readers should take his work with a grain of salt.

If you want to get more details on the differences in Corley’s data I suggest getting on his email list => here.

For more on building wealth, consider reading these:

The economy and markets have been on a crazy tear these days.

Think about whats happening.

The Yolo Economy – You no longer need to be in a specific geographic location to have a job. = > here.

Magic internet money has increased in value by 12,000%.

A new Jersey deli with a single location is listed at over $100 million.

Digital crowds can now manipulate markets – this used to be the exclusive purview of high net worth individuals or institutions. Per CNBC.

The Fed has dumped a ton of money into the economy – the total supply of money increased by $3 trillion in 2020 alone.

With all this insanity, the only helpful thought I can offer is: try not to get sucked into the economic craziness. If you can’t, then just take a very small percentage of your investable assets and play along. Whatever you do, try not to get involved in the insanity. Because…insane market conditions have a habit of ending badly.

Here is another posting for those interested in passive income.

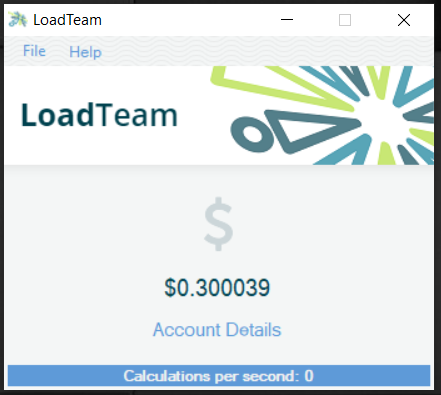

One of my goals for 2021 is to build more passive income. So, I’ve been experimenting with ways that I can build income without trading my time for dollars. Some of these are working pretty well, some of them are a bit more experimental. This article is a Loadteam review, which is a passive income application. It will be short, because I quickly reached a negative opinion of Loadteam.

What is Loadteam?

Loadteam is an application that allows you to make passive income using your computer. The main idea behind it is: download the application onto your harddrive, let it run and get paid. Loadteam’s business model basically works by mining cryptocurrencies using distributed computing. Their application makes use of unused harddrive computation power. It downloads part of a cryptocurrency problem set onto your laptop, cracks it, then sends it back to Loadteam.

Here is a screenshot of what the app looks like after it is up and running on your desktop.

My Loadteam Review – my experience

I had Loadteam installed on my laptop for about a month. This was my experience.

1. Very low payout. Loadteam credits your account with 40 cents when you get started. I earned 26 additional cents in the month I had it. I had the software installed on both my work computer and my home computer, and devoted 20% of my processor’s cycles to the application. So, the rate the application pays really isn’t worth the install time.

2. Load issues. Their application failed to load consistently, and caused my computers to occasionally freeze.

3. Loadteam has a thin corporate presence. From a brief review of their LinkedIn and other social media profiles, they’re located in New Zealand, which is fine. However, per LinkedIn, they’ve only got a couple of employees. With a small company there is always a bit more risk. Unlike a large company, Microsoft for example, Loadteam may not have the funds to pay it’s partners or they may not be able to release updates or fix security holes in a timely manner.

My take on Loadteam: don’t bother. I will likely be uninstalling it.

For more wealth building and passive income ideas, consider these great articles:

Since we dinks are hard at work today, we wanted to let you know about some handy money saving tips from your friend and our’s, The State of Florida!

Since we dinks are hard at work today, we wanted to let you know about some handy money saving tips from your friend and our’s, The State of Florida!