All,

There’s lots of good information available regarding tips for economizing your budget, but relatively less information about how saving fits into your overall strategy for your personal finances. Saving is in fact, rather passé today. Most Americans do not maintain a large cushion of savings. This is a shame, as saving can have a substantial impact on your wealth and financial security.

1) Saving is a Means to an End

The first point is savings should be a core part of your strategy. Saving should be a core part of helping you achieve something greater such as building up a nest egg or obtaining capital to start a business. Its not about gathering money for the sake of having money – that’s hoarding. Also, your savings should be part of a plan. Even a basic savings plan will help you better answer questions such as how much money you need and when you’ll need it. Saving will also help you to able cope with finance challenges like overspending or changing priorities that can derail your good intentions.

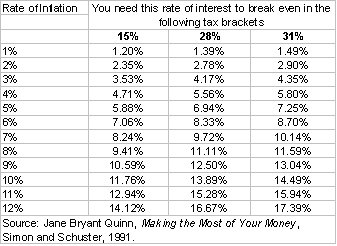

2) Your Savings have to Beat Inflation

Inflation is defined as a sustained increase in prices over time. This is important because high inflation can erode the amount of stuff or services your money will buy. Since you’re reading this blog, you probably already know what inflation means, so I won’t try to further define it here. The main idea here is that anything you put away needs to beat inflation to keep your savings from falling behind. How much do you need to beat inflation? – Good question. The table above will tell you the return your saving need to do better than inflation.

3) You can Save 10 Percent

Absent a goal, lots of people ask how much they should be saving. The truth is most people can manage ten percent of their income. Whenever we have this conversation with my friends, they inevitably start to say that they can’t save 10%. They complain that rent is too high, car payments are too much…etc etc. The way around this initial reservation is to start with a small amount, like 5%. Once you find that it doesn’t impact you that much, you can then gradually ramp up to 10% or 15%. Your expenses and lifestyle probably won’t be all that affected if you take a gradual approach.

Finally, the main point to consider is that savings can fit into your overall personal finance strategy. For example, you might be interested in putting a house down-payment together, or you might want to build up a cash reserve in case you have major medical problems. A savings plan that beats inflation can be an integral part of this.

Best,

James

Pingback:Save Your Money People - Save Your Money - Dual Income No Kids | Dual Income No Kids