James Hendrickson is an internet entrepreneur, blogging junky, hunter and personal finance geek. When he’s not lurking in coffee shops in Portland, Oregon, you’ll find him in the Pacific Northwest’s great outdoors. James has a masters degree in Sociology from the University of Maryland at College Park and a Bachelors degree on Sociology from Earlham College. He loves individual stocks, bonds and precious metals.

Whenever you make a new investment you never really know it will pan out.

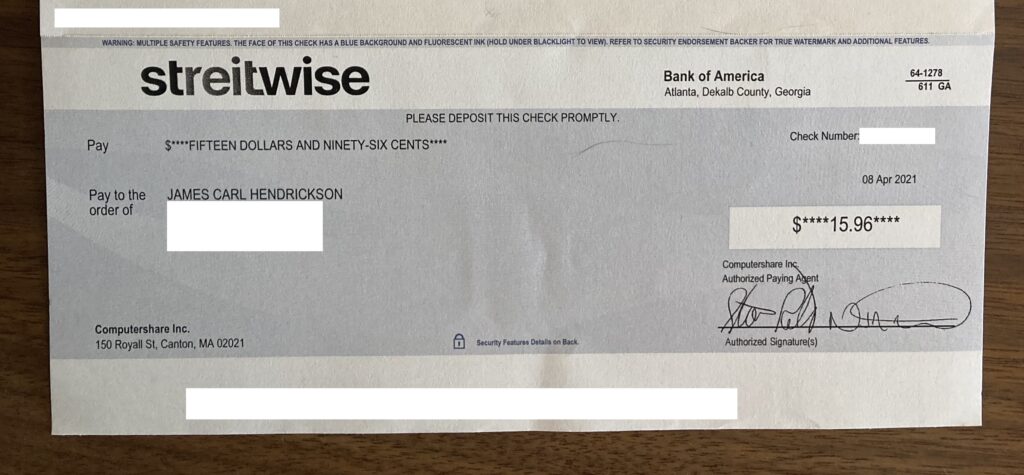

A few months ago, I bought about 100 shares of a closely held REIT – Streitwise. And…I got my first dividend check earlier this month. It’s a modest payment. Fifteen dollars and ninety five cents. But hey, $15.96 is better than nothing.

Its always nice when your investments actually send you money.

Here is the check below.

Incidentally – getting dividends is one of the major income streams of the rich. So, if you’re on the fence about getting some dividend producing assets, do it!

Here are more great dinks articles on building passive income:

Everyone is going nuts over cryptocurrency and the stock market, but bonds have been a viable investing vehicle since 2400 B.C. (here).

And, crowdfunded bonds are becoming a thing. Title III of the 2012 Jobs Act made crowdfunding bonds legal, so a number of companies are offering these products. These are:

All of these have relatively low investing minimums ($10 in the case of worthy and SMBX) and social/impact investing elements.

I’ve been investing with SMBX for a while. They’re the best of breed in the crowdfunding small business bonds space. They have the lowest minimums and the most virtuous business model.

Crowdfunded bonds aside, there are lots of ways you can get into bonds. You can always buy government bonds via treasurydirect.gov or get into bond ETFs through Robinhood.

Finally, most full service brokerages will let you buy corporate bonds (although you’ll need $1,000 to $10,000 for starters for these assets).

Why Buy Bonds?

You may be thinking – “Hey, interest rates are low and the stock market is going gangbusters, why should I buy bonds?”. There are several reasons why it makes sense:

Income: Bonds are steady sources of income.

Diversification: Over time better diversification results in better returns.

Bonds Preserve Principle: Fixed income investments are excellent for people nearing the point where they need the cash they have invested. This could be someone saving for college or for retirement.

Tax Advantages: Some municipal bonds well as some Federal bonds, are tax free.

Lastly, here is a list of “baby bonds” or small dollar corporate bonds, you might consider buying!

So, even though they’re out of favor, don’t forget about bonds!

Since it’s March and you’re reading a personal finance blog, you’re probably considering starting on your taxes. Well, it looks like you may have an extra month to file your returns.

According to Bloomberg, the IRS is allowing an additional month in which to complete your taxes. From Bloomberg.com:

The Internal Revenue Service is delaying the April 15 tax-filing deadline to May 17, giving taxpayers an additional month to file returns and pay any outstanding levies.

The postponement applies to individual taxpayers, including people who pay self-employment tax, the IRS said in a statement Wednesday. The relief does not apply to the first-quarter 2021 estimated tax payments that many small business owners owe, however, the agency said. Those payments are still due on April 15. The IRS said it plans to issue more guidance in the coming days.

“This continues to be a tough time for many people, and the IRS wants to continue to do everything possible to help taxpayers navigate the unusual circumstances related to the pandemic, while also working on important tax-administration responsibilities,” IRS Commissioner Chuck Rettig said in a statement. “Even with the new deadline, we urge taxpayers to consider filing as soon as possible, especially those who are owed refunds.”

So, it’s mid-March, which means it’s time for a monthly update. This month hasn’t been too sexy, mostly I focused on consistent debt and cost reduction. Here is the breakdown of what I’ve been up to.

Canceled Services & Reduced Bills

This month I spent some quality time on the phone with Comcast/Xfinity. I got autopay set up for a total savings of $10 per month, or $120 per year.

For some reason, cable internet companies don’t seem to have an appetite to reduce prices. This may be because they have local monopolies, or it costs their customers a lot to switch. I wrangled with them for about an hour and spoke with a couple of customer service reps – they couldn’t offer much beyond the autopay discount. Another thing with Xfinity is you’ve got to watch the fine print. The autopay discount is only good for 12 months, but they’ll keep auto-billing you without applying the discount after the 12 months are up.

Still, $120 savings for an hour’s work isn’t bad.

I had Starz but canceled that also. The savings was about $5 bucks. Not much, but the discipline of cutting expenses over the long run is what counts.

Finally, I called T-mobile, my cell service provider. Got it to issue a $20 dollar credit without much hassle. In contrast to Xfinity, T-mobile may let its customer service reps give discounts if the representative feels it is a good idea.

Paid Off Debt

My biggest financial goal is to get my credit cards paid off, I’ve got the figure down from $10,000 to $4,200. I’ve also been pretty consistent about paying off my mortgage. So far that’s realized about $1,800 in equity build up this year.

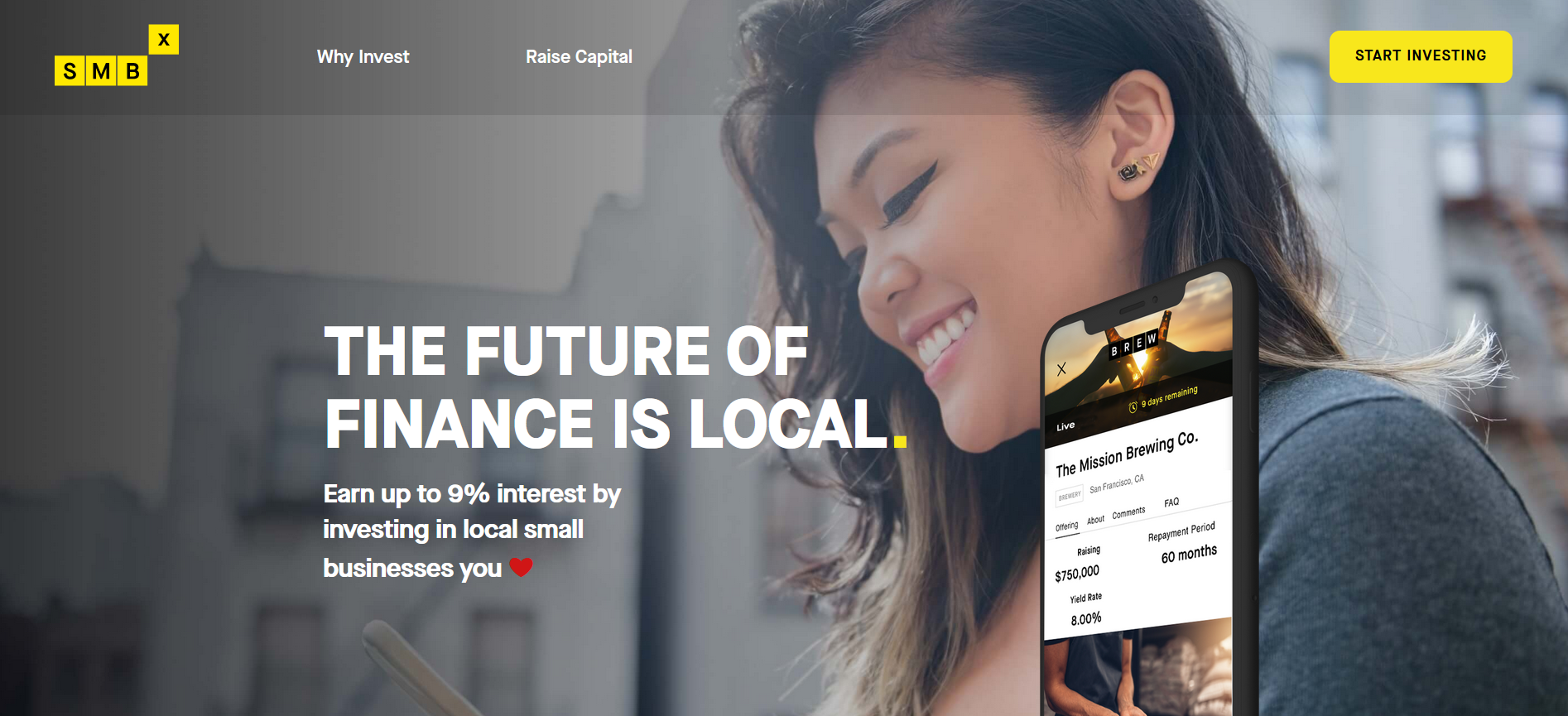

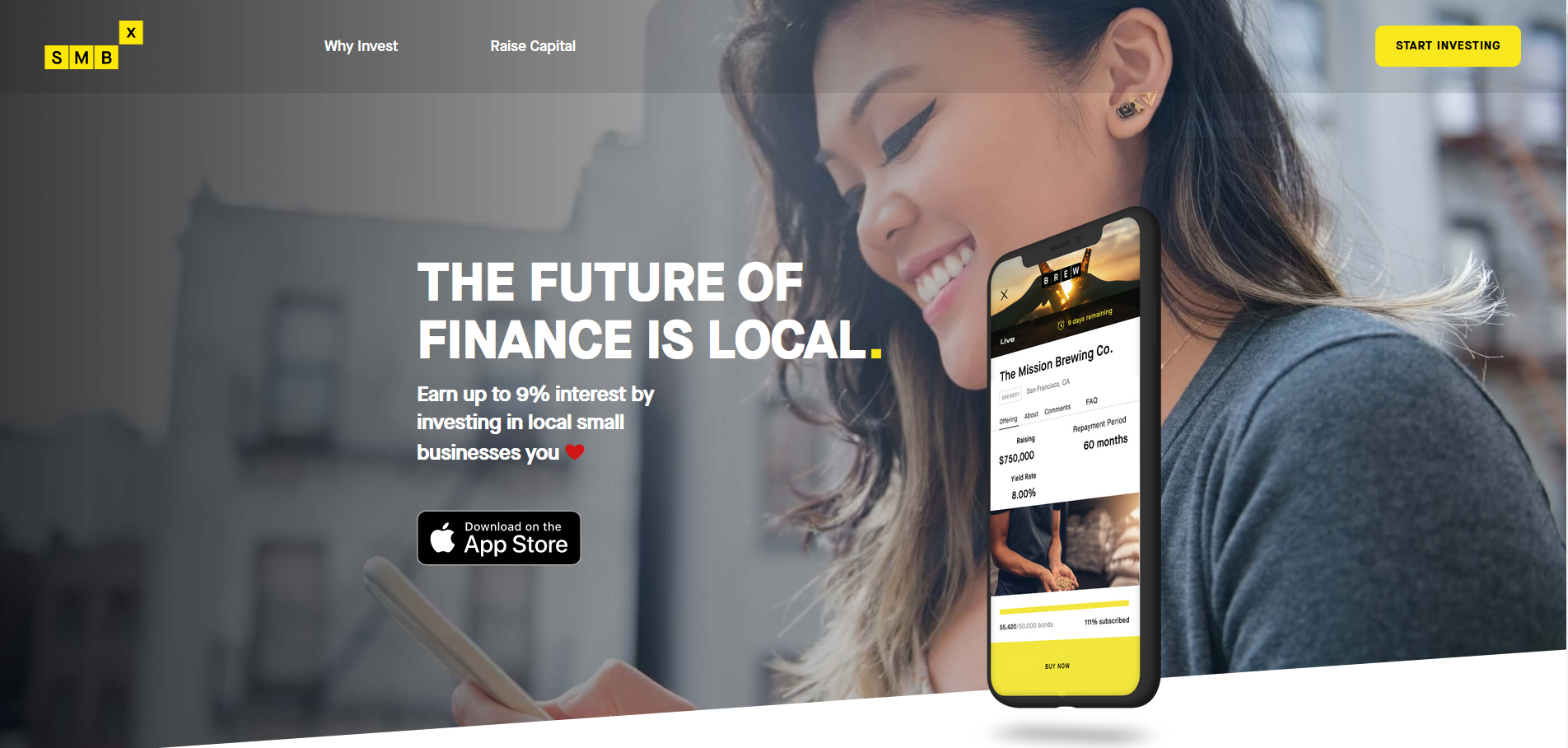

SMBX stands for The SMall Business Exchange. This is a cool little start-up in California. It’s basically building a marketplace for small business bonds — a neat idea because they’re using crowdfunding methods with $10 investing minimums. The model replaces the need for small businesses to apply for bank loans with more cost-effective bond structures. I like this basically because commercial banks tend not to lend to minorities, and this model diverts funds away from the banking system and into local communities. Wealth inequality has had a corrosive effect on U.S. society, so funding Joe and Jane average instead of the big banks is a good idea.

The value of my account there is super modest – it is something like $72.00. But, I’ll likely be putting more funds into the platform in the future.

Actually, if you’re interested in innovative fintech, I suggest you check them out.

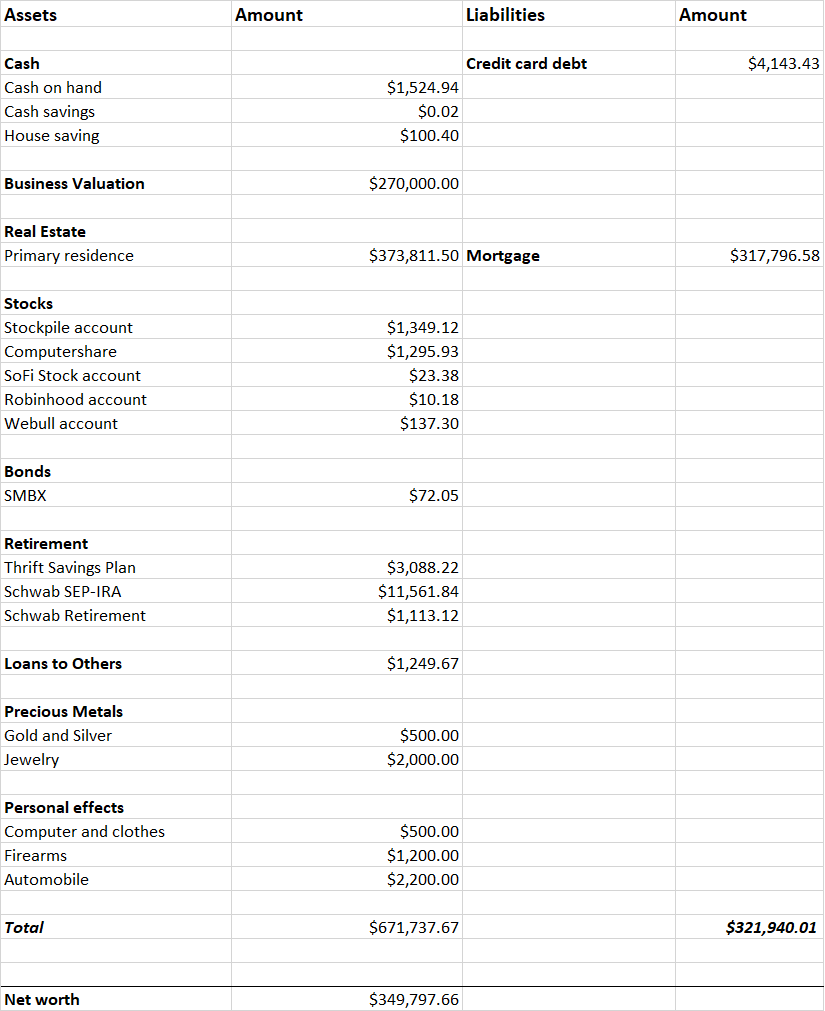

March Net Worth

Paying off debt and cost-cutting isn’t earth-shattering or sexy, but it’s good basic blocking and tackling that you need to do for long-term wealth building.

Here is my net worth in mid-March: $349,797.66.

If you’re interested in building wealth yourself, here are some good basic articles to read.

Long-time Dinks readers will know that we’re not shy about FinTech investing opportunities. A few weeks ago, I found a neat little start-up in California called SMBX. It is building a crowdfunded marketplace for small business bonds — a historical first. It’s an interesting company, so we’re covering it in depth here.

Before we launch into this, here’s what you need to know.

When you buy a bond. You are lending to the issuer, which may be a government, municipality, or corporation. In return, the issuer promises to pay you a specific rate of interest during the life of the bond. It also promises to repay the principal of the bond when it comes due after a set period of time. In general, bonds are less risky than stocks. Although, this can vary depending on the type of bond.

Unlike stocks, after bonds are issued, they are typically bought and sold in over-the-counter (OTC) markets. These markets are usually dominated by large institutional broker-dealers. Again, relative to the stock market, the bonds market is typically inefficient with fewer rules, less oversight, and higher costs.

Several things make SMBX interesting for investors.

Interesting Leadership, New Company

The California-based founder is Benjamin Lozano. Lozano is an unusual and fertile thinker, with a history of academic work in the ontology of finance. He founded SMBX with long-time collaborators Bhavish Balhotra, Gabrielle Katsnelson, and Jackie Chan. They’ve got obvious chemistry and they’re all in their late 40s, which is common for startup leaders.

Here is one of their team videos:

SMBX received venture funding from several impact investing outfits: Better Ventures, Impact America, Ironfire Ventures, and UC Berkeley. All of these funders are specifically focused on supporting companies with a social impact mission. So, the leadership team and social mission suggest SMBX is qualitatively different from most run-of-the-mill profit maximization enterprises.

The platform is new. SMBX was first registered with the SEC in 2018. The experience of the peer-to-peer lending market has shown that it’s not easy for companies such as prosper.com and LendingClub to grow their businesses based on charging processing fees to issue debt. SMBX’s monetization model charges borrowers 3.5 percent of funded loans.

Its platform currently shows that it has 16 bond issues, with ten being completed. The total amount of funded bonds so far is $1,342,510.00. At SMBX’s fee rate, that’s about $46,000 in revenue. This isn’t enough to support four core staff. However, this isn’t really a problem as the company has venture capital funding, which also means it’ll need to scale quickly to make its model viable.

Small Business Bonds Are a Totally New Asset Class

What’s really amazing about the SMBX model is it’s creating a totally new asset class. Nobody has really made a marketplace for small business bonds using digital crowdfunding before. It’s totally unique in human history.

Private Bond Markets Have Contributed to Instability

Private capital has traditionally dominated bond markets. With bonds being largely traded by broker-dealers funded by institutional or private money. This has historically contributed to the concentration of wealth and its associated problems.

And – in case you haven’t noticed, wealth concentration has become a serious issue. This has historically lead to dangerous social and economic instabilities. Famed investor Ray Dalio has noticed this. He recently posted in a LinkedIn update:

The Cycle of Internal Order and Disorder & Where We Are in It

Classically, the big cycle transpires with periods of peace and productivity that increase wealth in a disproportionate way, which leads to a very small percentage of the population gaining and controlling exceptionally large percentages of the wealth and power, then becoming overextended, then encountering bad times that hurt those who are the least wealthy and powerful the hardest, which then leads to conflicts that produce revolutions and/or civil wars, which after completed, then lead to the creation of a new order and the cycle beginning again.

The current state of the U.S. bond markets frankly contributes to the timeless cycles Dalio noted. Basically, if only big banks and rich people have access to bonds and their advantages (portfolio stability, and regular income, etc.), the rich increase their control over the nation’s wealth, alienating the rest of the population.

Public Crowdfunding Could Reduce Disparities

In 2019, Americans of African descent had a median family net worth of $24,000. This is the lowest of any ethnic group measured in the Federal Reserve’s Survey of Consumer Finances. Part of the reason for this is lower average incomes and reduced chances of receiving inheritances. This also means that, on average, African American people have less capital to work with and are less likely to afford the $1,000 price of most bonds.

Funding small business growth can be a challenge for minority business owners. Obtaining traditional bank financing is often tougher for minorities than others due to issues such as insufficient credit, limited banking history, or unconscious bias. In cases when traditional bank financing is not available, business owners are often forced to utilize high-interest predatory lenders.

SMBX’s model represents potential solutions to these problems. SMBX has a $10 dollar minimum purchase price. It’s designed so that anyone with a U.S. bank account can buy in. This means that even low socioeconomic people can afford to invest, and minority businesses can get access to funding opportunities that might not be otherwise available due to institutional barriers. This is largely because SMBX operates on a crowdfunding model. Businesses can work with their existing customer base to fund their bond offerings, circumventing the need for traditional financing.

SMBX is New, And Not Risk-Free

It is having some trouble attracting investors. I think this is due to a couple of reasons. First, nobody has heard of SMBX and most of the companies on the platform. Second, SMBX is the initials for The Small Business Exchange, but it also stands for Super Mario Brothers. So if you google for SMBX, you get a bunch of hits for Super Mario Brothers-related content. Third, the investing public doesn’t know how to judge the risk/return ratio.

Here are a few other things you should be aware of:

Bonds are out of fashion these days. With bitcoin and the equity markets generating double-digit returns nobody is excited about 6 percent real interest rates.

The assets are still not liquid, but that’s normal for FinTech startups. Peer-to-peer lenders such as prosper.com and Lending Club weren’t able to generate a marketplace for their securities, so it’s common in the crowdfunded space. SMBX is built on a blockchain platform so it’s possible it will have superior transparency when it comes to bond ownership pedigree.

Bonds have some risk, and small business bonds are riskier than other kinds of bonds. This is offset by the higher rates of interest paid.

Bonds are variable in quality, the financial strength of the businesses in the SMBX platform meets minimum criteria, but beyond that, it’s variable.

Ultimately, with a new asset class, nobody really knows the risk. The data just isn’t there to calculate realistic figures in SMBX’s platform yet.

Who Should Buy SMBX Bonds?

SMBX bonds have all the virtues of bonds as an asset class: asset value stability and income. So if you’re interested in having assets with stable prices and predictable income, SMBX isn’t a bad candidate. You’ll need to take a limited position though, as the platform is new and the risks of investing in small business bonds aren’t well defined yet.

Ultimately, what makes SMBX interesting is the potential of the business model and the chance to make money, not just make money. So, if you want to add some diversification to your assets and you like supporting companies that can impact the structure of capitalism, SMBX would be a fun company to invest with. Check it out => here.

If you’re like us DINKs, you’re probably wondering how to improve your financial bottom line. The recent covid related economic slowdown has torpedoed some people budgets, so some options for seeing immediate gains to one’s net worth are limited.

One way to immediately improve your bottom line is to pay off your debts. There are several advantages in doing so.

First, paying off debt improves your cash flow. Every dollar that’s borrowed usually costs you to carry the debt. Right, so if you owe 100 dollars at 6 percent annually, it costs you 6 bucks to carry the debt every year. Well, if you pay off the $100, then your budget has an additional 6 dollars more. Run some real numbers to see if what I’m saying makes sense.

Second, paying off debt improves your net worth. For example, let’s say you have a mortgage worth $100,000, but you own $80,000 on your house. Your networth, all things being equal, would be $20,000 (i.e. $100,000 – $80,000 = $20,000). But, if you spend some time and aggressively pay down $10,000 on your mortgage, then your net worth is now $30,000. This is only natural, when pay down debt your net worth, and accordingly your ability to build wealth increases dramatically.

There are some tax issues with interest deductibility, but basically the first two points hold true.

Third, debt reduction is risk free. You incur absolutely no market risk, systemic risk, or other kinds of risk if you pay off debt. Every dollar you pay off is a dollar more towards your net worth, and a dollar that improves your cash flow – all at no risk to you. This is a contrast to stocks, bonds, cryptocurrency & starting a business or any of the other typical means that people use to improve their net worth.

In terms of the mechanics of making this happen, here are some practical tips on getting extra money to pay off your debt, as well as an example of how its done.

I was chatting with a friend the other day, and her sister messaged her on Skype. Her sister was curious as to about how much she should be spending on common household expenses. Well, I was also curious and decided to hit the books to see what good rules of thumb are.

According to the Motley Fool, you might consider the following very rough guidelines:

Housing and utilities, 25-30% Food, 10-15% Vehicles, 10-15% Insurance, 5% Saving and investing, 10-15% Entertainment, 5% Clothing, 5% Medical, 5% Childcare and education, 1-8% Gifts and charity: Up to you!

Of course, where you live is a major factor in how little you pay for each category. For example the DC area, housing is very expensive. In a rural part of the country like Oregon rent and mortgage prices are more manageable.

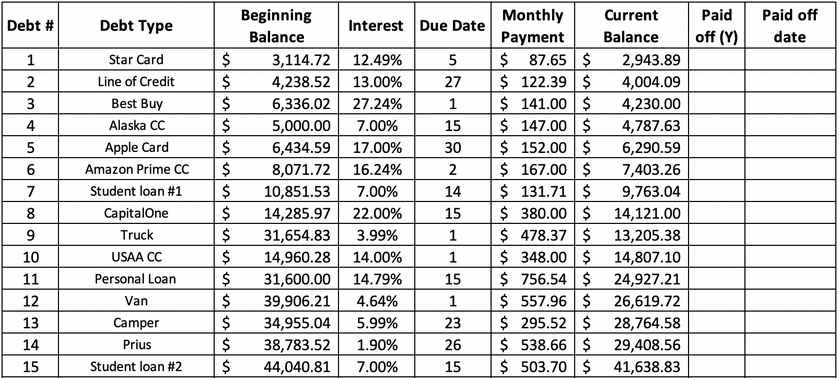

I spend a lot of time on the internet, especially on personal finance blogs. Over this weekend I came across this posting. Evidently its written by a couple from Alaska. The interesting thing is…they have a lot of debt. Not just like a few thousand on a couple of credit cards, they owe about $232,000 in multiple vehicle loans, student loans, credit cards, and personal loans.

Here is a screenshot of what they owe:

My first reaction was: wow, how does that happen?

My second reaction was: wow, it must be tough for them. Probably most, if not all of their income is spent on debt service.

In any event you might want to surf on over to their original posting. The commenters there have some good pointers on debt management.

As an aside note, DinksFinance is really more about investing and couples finance, so if you want more info on debt reduction, I’d check out these sites:

In 1758, Benjamin Franklin, the original blogger, wrote an essay called The Way To Wealth. The essay is basically a collection of advice and adages from 25 years of Franklin’s Poor Richard’s Almanac.

I’m presenting it here because most of what Franklin said in 1758 is still applicable today. Especially the themes of hard work and frugality.

Here are some notable quotes:

“Beware of little expenses; a small leak will sink a great ship”

“Gain may be temporary and uncertain, but ever while you live, expense is constant and certain”.

“Sloth makes all things difficult, but industry all easy”.

Here is a text version of The Way To Wealth =>: https://liberalarts.utexas.edu/coretexts/_files/resources/texts/1758%20Franklin%20Wealth.pdf

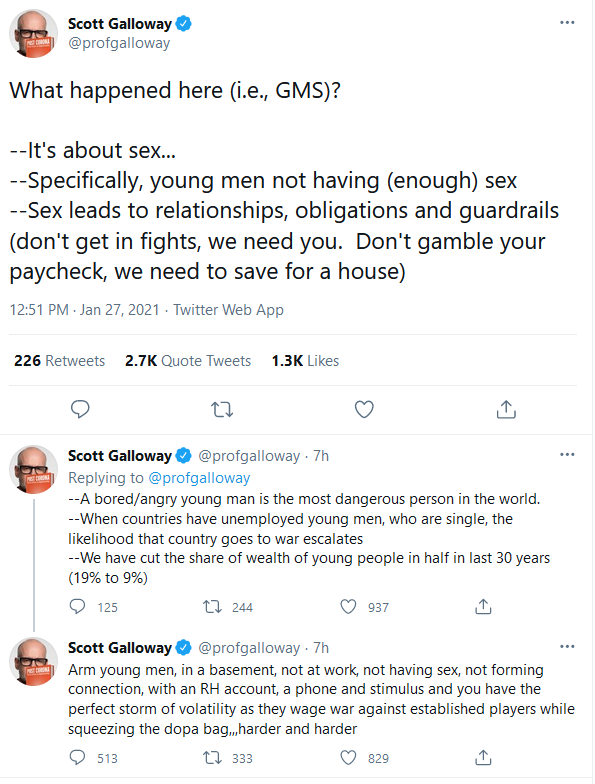

The biggest thing to happen in the markets this year is the action on GameStop, Inc. You’ve probably heard what’s happening but briefly summarized small traders, using internet forums like Reddit, 4chan, and TikTok, led by a man calling himself “Roaring Kitty” have coordinated to drive up the price of GameStop, Inc.

This was made possible by mass use of stock trading apps, zero-commission fee structures, and easy communications. Much of the motivation has been quasi-populist, with small investors betting against hedge funds who’ve to take a short position in GameStop (and other companies).

Market manipulation is nothing new. What is interesting is what is driving this particular market manipulation. There haven’t been a lot of good explanations, but the best one so far has been offered by Scott Galloway. Galloway is a marketing professor at NYU’s Stern School of Business, so his viewpoint carries weight. He’s saying the problem is caused by a critical mass of single young men “armed” with trading accounts and stimulus money.

Here is his Twitter thread.

He’s correct in a couple of respects – young unmarried men are the demographic group that has the highest propensity to commit a crime. He’s also correct about the weakening legitimacy of social institutions in general.

Readers: if you are browsing this article because you’ve got money in GameStop, please don’t forget. Populist uprisings don’t always go well. GameStop is a very poor long-term prospect so don’t forget to manage your risk. Diversify or take a limited position in the stock.

And – in case you haven’t noticed, wealth concentration has become a serious issue. This has historically lead to dangerous social and economic instabilities. Famed investor

And – in case you haven’t noticed, wealth concentration has become a serious issue. This has historically lead to dangerous social and economic instabilities. Famed investor

In 1758, Benjamin Franklin, the original blogger, wrote an essay called The Way To Wealth. The essay is basically a collection of advice and adages from 25 years of Franklin’s Poor Richard’s Almanac.

In 1758, Benjamin Franklin, the original blogger, wrote an essay called The Way To Wealth. The essay is basically a collection of advice and adages from 25 years of Franklin’s Poor Richard’s Almanac.