James Hendrickson is an internet entrepreneur, blogging junky, hunter and personal finance geek. When he’s not lurking in coffee shops in Portland, Oregon, you’ll find him in the Pacific Northwest’s great outdoors. James has a masters degree in Sociology from the University of Maryland at College Park and a Bachelors degree on Sociology from Earlham College. He loves individual stocks, bonds and precious metals.

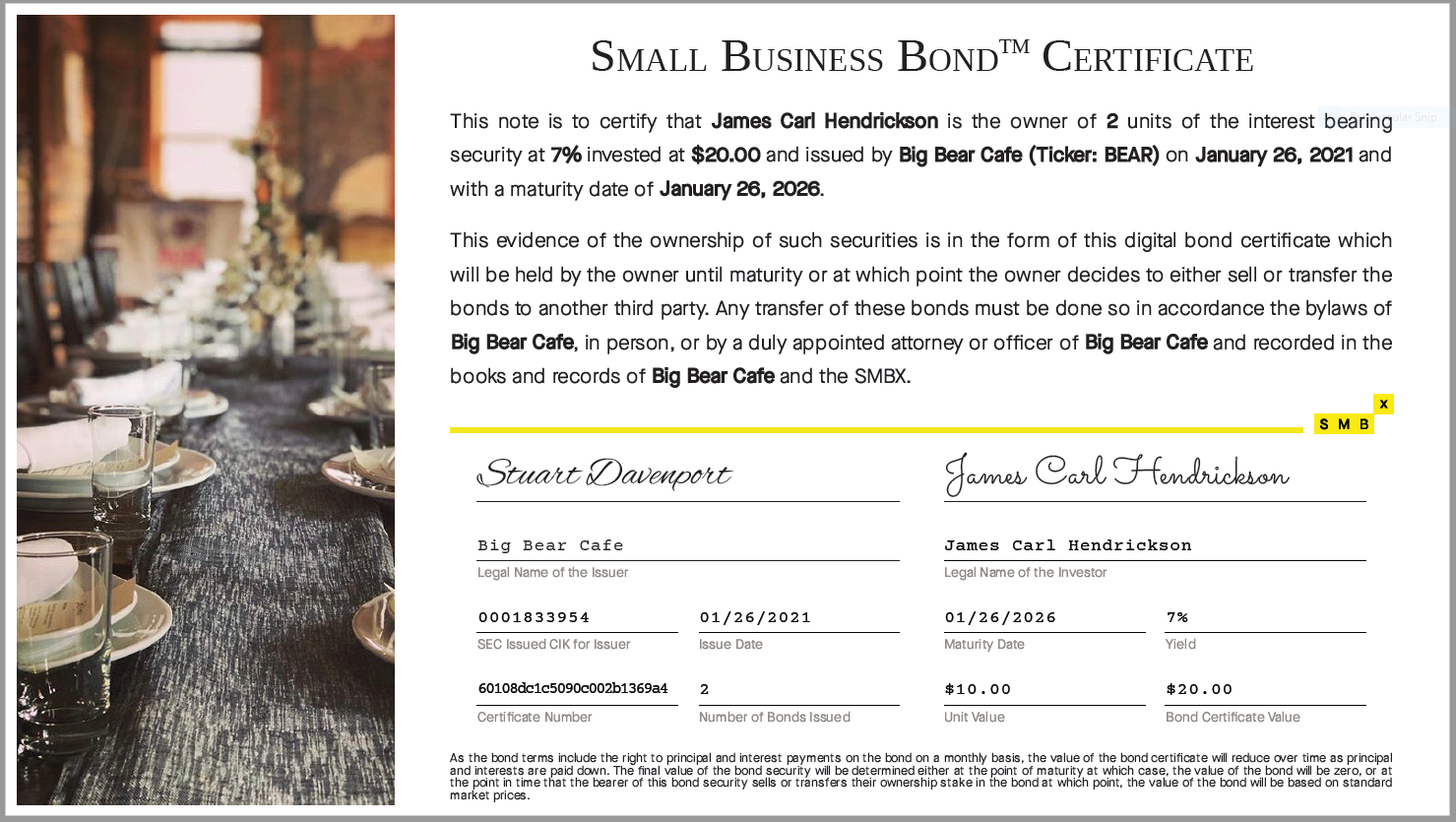

A few weeks back, I took some of the holiday gift money I’d received and put it into small business bonds. I did this via a neat, if not somewhat risky fintech I’d discovered last year. Well, it seems like the bonds are starting to get processed and issued. I just received this in my email today:

Even though its electronic, its nice to get the actual bond statement. When the US Treasury phased out paper savings bonds in 2010, I was a little bit disappointed. There is nothing like having an actual physical paper receipt to prove you own something. Sometimes the digital world feels too ephemeral to be real.

The company I bought the bond through is called The Small Business Marketplace or SMBX. They’re a Fintech start up trying to build a market for small business bonds. At this point, the model is pretty immature – nobody really knows what the risk profile for small business bonds look like. So I just put a small amount of money in to limit my risk. Still, it’s pretty cool to see the process working, and if things are successful I’ll get 7% on my 20 dollars.

For more on the mechanics of wealth building, read these:

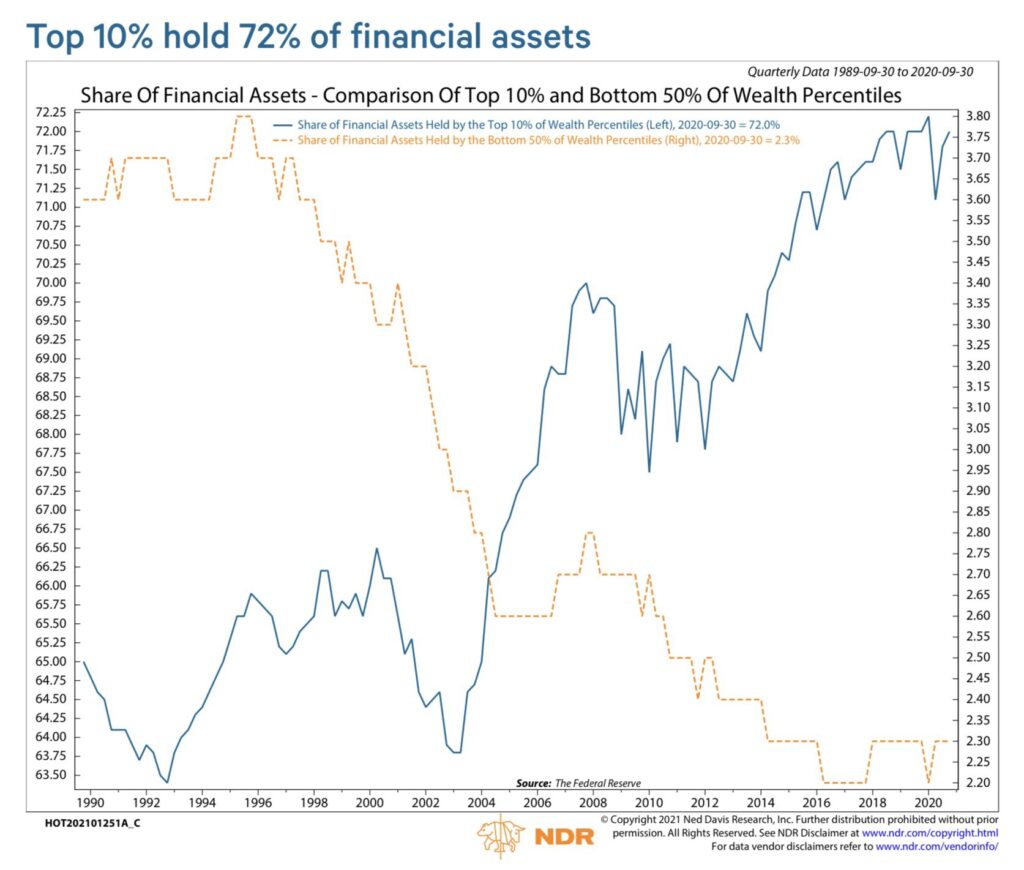

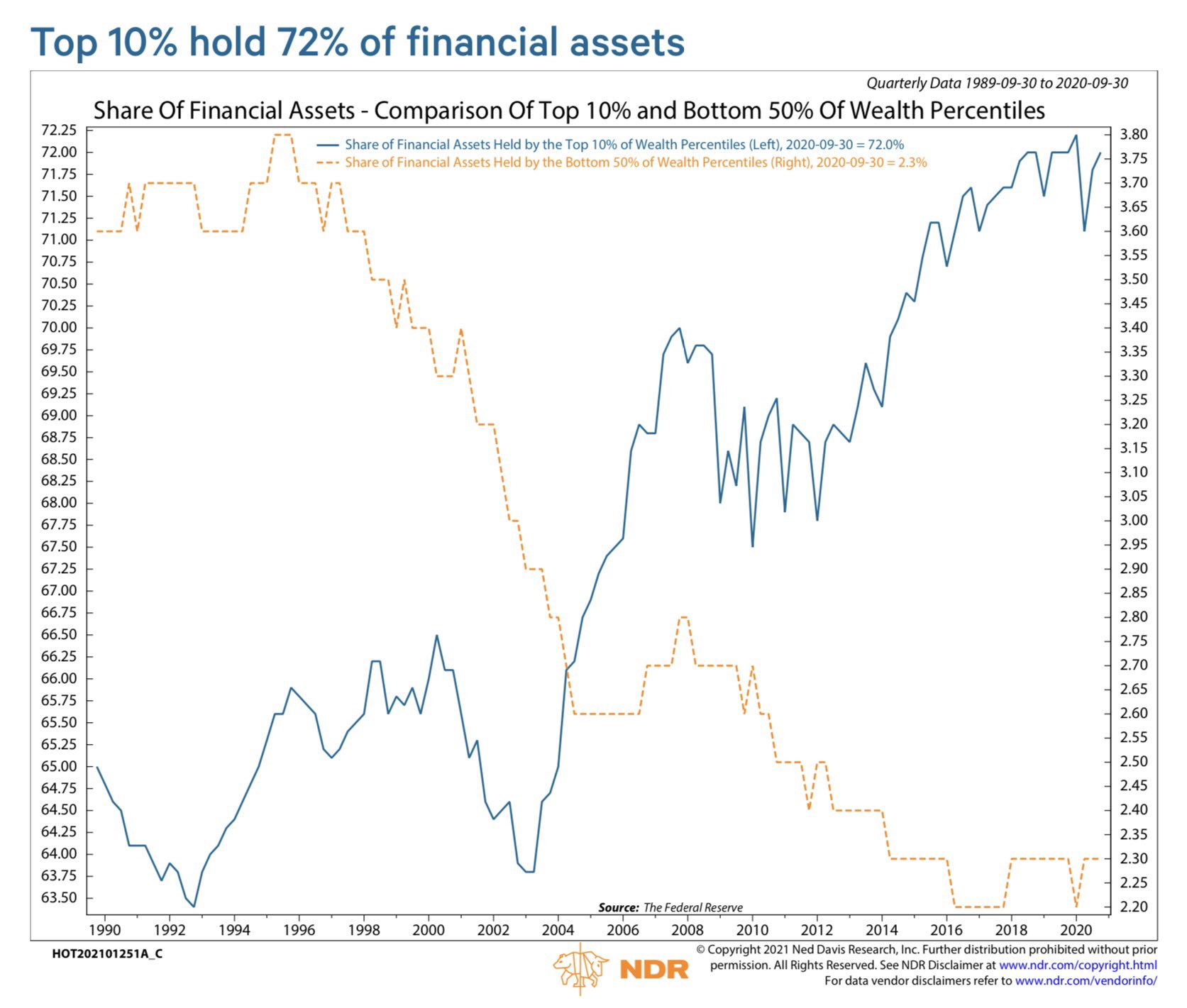

Here is an example of a K-shaped chart for you. This shows the long time divergence of the amount of financial assets held by the top 10% versus those held by the bottom 50% of wealth percentiles.

The graph has different axes, so sit and look at it for a while. In a nutshell, the share of financial assets held by the bottom 50% has declined from 71% in 1989 to 2.3% in 2020.

For some historical context on the concentration of wealth, you might consider reading Will and Ariel Durrant’s The Lessons of History. They have a highly pertinent summary of the concentration of wealth in their chapter on economics and history. Here is what they think drives wealth inequality.

Since practical ability differs from person to person, the majority of such abilities, in nearly all societies, is gathered in a minority of men. The concentration of wealth is a natural result of this concentration of ability, and regularly recurs in history. The rate of concentration varies (other factors being equal) with the economic freedom permitted by morals and laws. Despotism may for a time retard the concentration; democracy, allowing the most liberty, accelerates it.

Thought I’d update all of you on what I’ve been doing to build wealth in the new year. I’ve been focusing on the basics (paying down debt, investing, etc.). However, since my attempts to build passive income by utilizing my unused computing resources haven’t yielded much, I decided to pivot and invest in real estate and small business bonds to build up more revenue flow. The companies I looked at in January were a couple of newer fintechs: StReitWise and SMBX.

StReitWise

StReitWise is a private real estate investment trust (REIT). They’ve been making the rounds of the blogsphere in the past few months. Unlike most REITs you might be familiar with, StReitWise’s equity is privately held. This means that unlike common stock traded on the New York Stock Exchange there is no way to sell their shares if you buy them. Privately held REITs are typically riskier investments – they’re regulated by the SEC, but they often have transparency issues (here). This was especially the case in 2008 when many invested in the subprime housing market, resulting in unexpected losses.

StReitWise also has a couple of challenges in particular. Commercial real estate is experiencing substantial losses due to changing labor patterns. More people are working from home, so the demand for office space is falling. This is somewhat mitigated by the fact that most of their leases are valid through 2024, and by their recent dividend payment cut (data here). So, some of the loss is already factored in.

That said, StReitWise’s has returned between 8 and 10% on an annualized basis. So, net of their management fees (2%), I’m hoping to make 6% real returns. That’s four times what the S&P is yielding. It’s also going to help diversify my assets. Due to the risk, I got the minimum buy-in – $1,007.

SMBX is a highly interesting company. Unlike a lot of the FinTech out there, SMBX could be a long term winner. SMBX is basically working on creating a market for small business bonds. The problems SMBX solves are: 1) access to inexpensive capital for small businesses and 2) improved risk-adjusted returns for investors. Small businesses typically have a hard time obtaining cost-effective financing. In a lot of cases, they can’t obtain financing at all, especially if they’re female or minority-owned, or they’re forced to get funding from usurious outfits like Kabbage. SMBX solves this problem by helping companies issue bonds with coupon rates between 6% and 10%, which is less expensive than many alternatives currently available. For investors, the value proposition is also attractive. The rates are far better than many other lending instruments.

SMBX is still a pretty small company – they’re funded by venture capital and I’m pretty sure they aren’t cash flow positive. Which means they could go out of business. Also, the small business bond market they’re developing isn’t mature yet, so like StReitWise, the assets are illiquid. Investors are totally dependent on SMBX for their bonds to maintain their value. Their website is here. Recommend you check it out.

I put about $180 into the platform earlier this week – not much due to the liquidity issue.

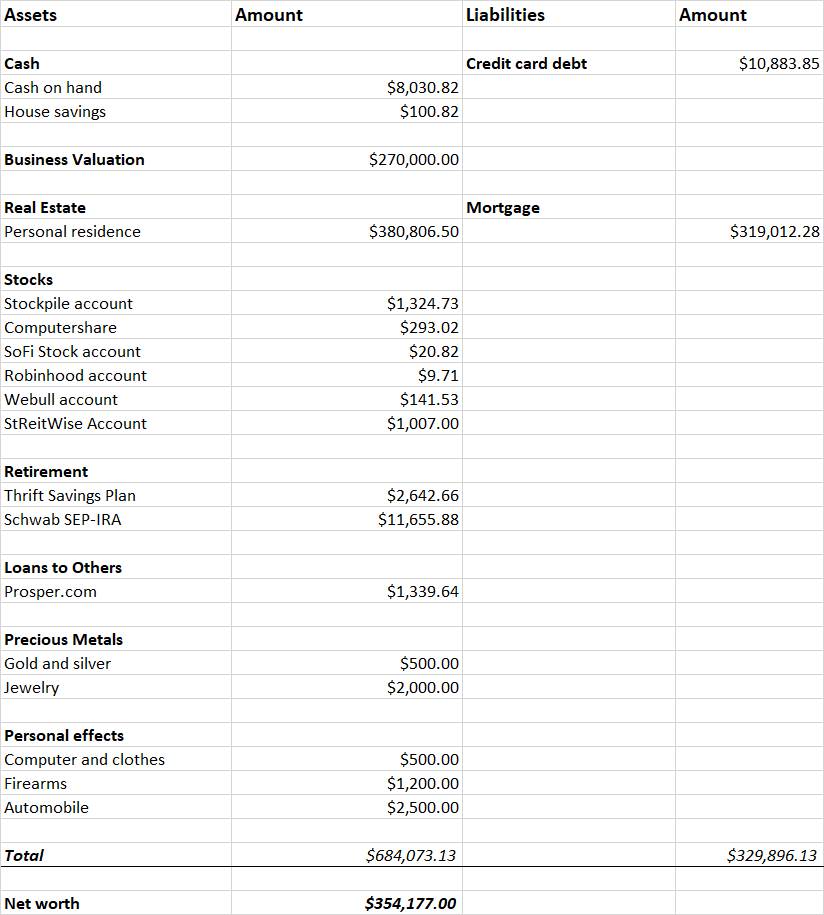

January wealth: $354,177.

At the start of January, my personal wealth was at $345,177. I’m up by about $63,000 since the start of 2020. This is mostly due to improvements in the value of my business, stock market appreciation, and debt payoff (e.g. reduced mortgage and credit card balances). Here is the snapshot of my net worth as of January 7th.

Incidentally, I opened up accounts with Robinhood, Webull and SoFi for the sign up bonuses. You might consider doing the same. Its free money.

For more on the mechanics of wealth building, consider reading:

Editors note: In light of the protesting today at the US capitol building – this article is being republished.

Unless you’ve been away from the internet in the arctic, you’re probably aware of recent events following the killing of George Floyd in Minneapolis. The country has been gripped by the largest wave of civil disorder since 1968. The costs of riots are substantial. Past riots have cost between $50 and $446 million with scores dead. But, there is a way to protect yourself.

I’ve been seeing a lot of news articles talking about how wealth is owned in the United States. The main idea is usually centers around a statement such as “the rich are getting richer” or “only a few people control a disproportionate amount of wealth”. The main idea behind much of these news stories is that only a few people control most of the money in our country. This has been especially the case with the recent pandemic related news highlighting the growth of big tech.

The major implication of these statement is that “the system”, e.g. the government, society, whatever, is subtly influencing policy and laws to keep economic resources out of the hands of the general public. Thus, the thinking goes, the odds are stacked in favor of entrenched interests such as corporations and accordingly, the poor are poor because society is structured to keep them that way.

Since “the system” isn’t keeping anyone down, the question is: what is about the individuals who do manage to become wealthy? These factors aren’t any surprise: people who save money, live frugally, and invest prudently are more likely to gain wealth. People who don’t do these things, aren’t going to become rich. If you don’t buy it, read The Millionaire Next Door.

The long and short of this is two things: 1) lack of wealth is due to the individual and 2) if you want to get ahead, you should dispense with the idea that society is holding you back.

Friend tip: If someone tells you about an important upcoming date in their lives, write it into your calendar and send them an appropriate text on that day.

It’s a quick and easy way to improve your relationship.

So, I wanted to update you all on what’s been going on with my personal finances.

Last month my truck died on the way to a hunting trip – it needed a new engine. The repairs ended up costing around $4,200. I ended up selling some of my gold and silver to cover the bill. When I was figuring out how to pay for the cost, I was kicking myself for not having an emergency fund. So, that could have been better.

On a more positive note, I’m seeing that my efforts to build passive income and wealth are getting some traction.

Passive Income

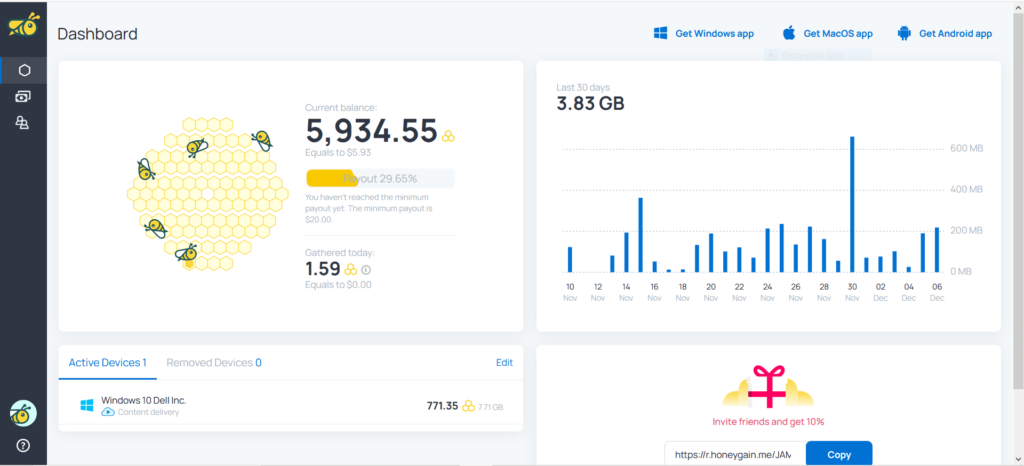

Most of the passive income ideas I’ve read about aren’t really passive – they all require some effort or capital. So, I’ve been looking at using my unused computer memory and bandwidth to generate some extra revenue. I’ve tried two different programs so far: Honeygain and LoadTeam.

Honeygain

Honeygain is billed as ‘Truly Passive Income”. How Honeygain works is basically you give Honeygain a portion of your internet bandwidth, and in return to Honeygain pays you a very modest amount. Honeygain then sells the bandwidth it to market research and search engine optimization companies.

Their app was super easy to install on my desktop and it has a neat looking interface (below).

On the other hand, it is not a big money maker. Factoring in the sign up bonus, I’ve made $5.85. It’s been paying about 2-3 cents a day. That’s not that great.

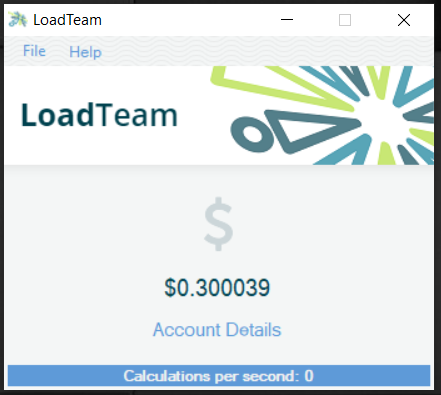

LoadTeam

LoadTeam basically a cryptocurrency mining outfit located in New Zealand. There isn’t much on the company on LinkedIn or on Facebook. What there is, suggests it is a smaller operation. It also seems like they’re renting space on users computers to mine cryptocurrency. This isn’t a bad approach as it means they avoid the major expenses most cryptominers have, which is electricity and computing hardware.

The money with LoadTeam is quite poor. They give you a 20 cent sign up bonus. However, even with my super fast gaming laptop, I’m still just making about two cents a day with the LoadTeam application. It also appears to be slowing down my computer. I’ll probably see how long it takes to reach a dollar and then uninstall the software.

Both of these have referral programs, so you can always make some extra money by getting others to sign up for their programs.

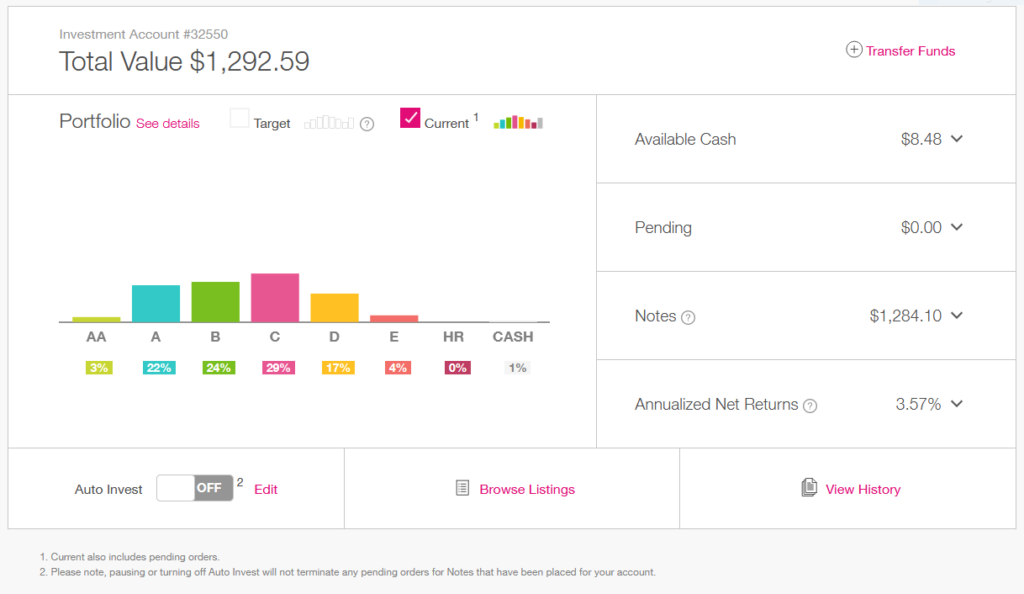

I’m still investing with Prosper, even thought I’ve been hearing negative rumors about bad corporate culture from friends. I’ve got the total portfolio returns up to 3.63 percent from 3.5 percent. The value of my account is also up to $1,333.81 – up from $1,092.00.

Stocks

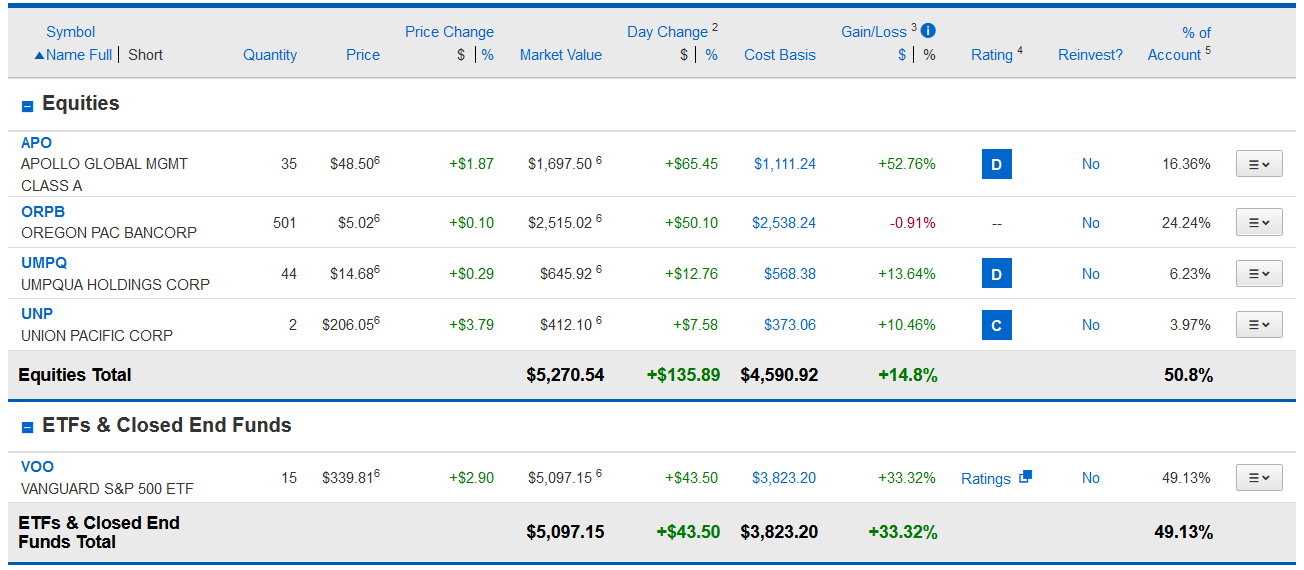

A while back I was writing that I was a terrible stock picker – I still am. To improve my performance, I ultimately went with getting a subscription to The Motley Fool’s stock advisor. I picked up a couple of shares of Union Pacific Railroad on their recommendation. We’ll see how it works out.

Incidentally if you’re looking to get some inexpensive stock picking advice, you could get The Motley Fool’s stock advisor for like 80% off. They’ll charge you like $100 bucks for a year, but if you go through a cash back site, you might be able to find a deal. For example, Dollar Dig is offering The Motley Fool for $80 cash back, on your first year. So if you go through them you’ll get the service for basically 80% off, probably more if you use a credit card that gives you points back.

Actually, that’s the thing with digital information subscriptions. Beyond their initial productions costs, it doesn’t take a whole lot to maintain them. This means you can often find a sweet deal on them.

For those of you who are interested in prosper, here is a quick update on what is going on with my account.

I’ve been pretty consistent with investing in Prosper since 2006. For the last couple of years, I was paying off a ton of credit card debt and was drawing down the account. However, I’ve got the debt under control, so I’ve been gradually easing back into the platform.

For those not in Portland, Oregon, here is the view from my balcony this morning around seven AM. Oregon is on fire. The haze in the air is heavy smoke from wildfires in the Cascade Range mountains.

I got up this morning and started reading the news. Evidently there was another round of riots in Minneapolis, Oakland and aggressive protests in Portland, Oregon last night. This comes on the heels of civil disturbances in Chicago and Denver earlier this month.

LoadTeam basically a cryptocurrency mining outfit located in New Zealand. There isn’t much on the company on LinkedIn or on Facebook. What there is, suggests it is a smaller operation. It also seems like they’re renting space on users computers to mine cryptocurrency. This isn’t a bad approach as it means they avoid the major expenses most cryptominers have, which is electricity and computing hardware.

LoadTeam basically a cryptocurrency mining outfit located in New Zealand. There isn’t much on the company on LinkedIn or on Facebook. What there is, suggests it is a smaller operation. It also seems like they’re renting space on users computers to mine cryptocurrency. This isn’t a bad approach as it means they avoid the major expenses most cryptominers have, which is electricity and computing hardware.