Can’t Save? Use Digit.

One thing I love about being a personal finance blogger is the chance to review new and exciting technology. The latest innovative product to come out of Silicon Valley is something called Digit. Digit is a web based application which identified and saves any surplus you have in your bank account.

The software is generating a lot of buzz on the internet – Digit has the potential to help people who aren’t great at saving money more efficiently manage their cash flow thus allowing them to save any excess cash without a lot of effort.

About Digit

The Digit process is pretty simple. Digit works on a passive model – all you do is attach your checking account and their robots do the rest – analyzing your income and spending patterns to figure out what amounts you won’t miss, and then transferring these amounts right into a savings account it creates for you.

1. You link your checking account to Digit’s secure Website. It takes 5-10 minutes and you’ll need your account and routing numbers plus answers to any security questions.

2. You confirm your account via text message.

3. Over the first couple of days, nothing happens. With their proprietary algorithm, Digit analyzes your historical spending and checking account balances.

4. Then, Digit makes small periodic savings transfers from your checking account to your Digit account. The transfers are small (a few bucks) and will be timed not to interfere with bills or other expenses.

It’s all really easy. The setup is pretty much idiot proof, you just need to follow the prompts from Digit on your smartphone.

Digit Gives You a Mental Boost

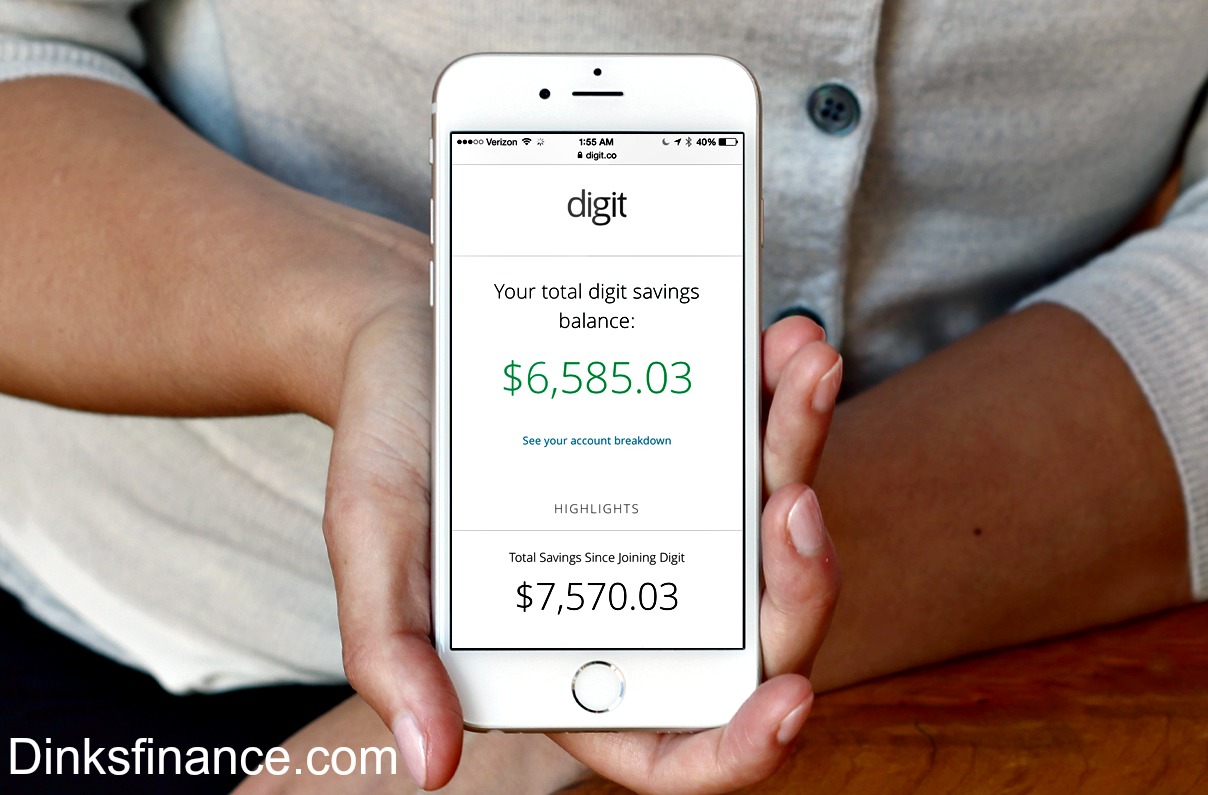

One great thing about Digit is that checking your account is usually a psychological boost. Often when you’re looking at your checking or brokerage accounts, you sometimes have an unpleasant surprise. You could be overdrawn or your stocks or bonds could decline in value. A lot of the time people know they need to save, but the process is stressful. But with Digit every time you check your Digit account, you should see more money in it! Thus using Digit is just fun.

How Does Digit Work?

These answers come paraphrased off Digits Frequently Asked Questions:

Is it free? Yes. There are no fees.

How does it work again? Every few days Digit checks your income/spending patterns and moves a few dollars from your checking account into its savings account. This is only if you can afford it.

What if it transfers over too much? Digit has a “no overdraft” guarantee which means they’ll cover all costs incurred if this ever happen. Digit believes in their technology so this will happen very often.

Do you need to set up a new savings account? No. When you sign up you automatically get one through Digit.

Is it insured like all other banks? Yes. All money saved is FDIC insured up to $250,000.

Can you withdraw your money anytime you want? Yes. All you have to do is text them “withdraw” and you can send your money back to your checking account as often as you need or want. Just like any other bank account.

Digit works using text messaging. The whole system is set up around a text based system to make it incredibly easy. You can text in for a bunch of things like “savings” to see the amount saved so far, “balance” to check your checking balance, “pause” to stop the savings, and “bills” to see upcoming bills they know you’re about to get.

What Problems Could Digit Have?

There are at least four potential downsides to Digit

1. What about Digits’ information security? Do they have a mechanism for stopping hackers or their employees from stealing or selling your bank account information? A review of their webpage suggests they have are a startup, with a staff of 5 to 6, it’s not entirely clear if they have the organizational capacity to prevent theft or resist hard core hacking attacks. Also Digit’s privacy policies seem to indicate that they will sell your personal information to a 3rd party if business needs require it.

That said, Digit doesn’t store any bank logins or passwords on our system. They also encrypt sensitive data using asymmetric cryptography and they store sensitive data anonymously.

2. Digit is a startup. This means that its business model is promising, but doesn’t have a long term track record of sustained profitability. While any funds you are holding with them are FDIC insured, there is no guarantee that the service they offer is going to be around in the long term. If they can’t grow the amount of funds they have under management, it’s not clear if they’ll have long term survivability. For example, as of the end of 2014 Digit had about $600,000 under management. They may have obtained more since then, but the interest on $600,000 isn’t enough to sustain 5 salaries and the IT equipment needed to run a company like Digit.

3. Digit gets to use your money while they are holding onto it for you. This is fine if the amounts are small, like 50 or 100 dollars, but if they hold 500-1,000 or larger amounts of your money, you might be better off having the cash in an interest bearing account.

4. Digit also doesn’t have coverage for a lot of the smaller credit unions. The weight of the last 15 or years has shows that Credit unions are a better deal for consumers, so if you bank with a local credit union, Digit might not be able to help you out.

But even after you’ve connected, some banks have security features that make it more difficult to maintain that connection. Doing this level of data entry for some people can be a hassle. Unless this gets remedied it could lead some people to avoid the service.

Our Review of Digit – The Bottom Line

So here is our bottom line assessment of Digit. Use Digit if you have can’t save and need help. Don’t keep a balance in their service. To build your networth aggressively, you’ll need every dollar working for you as hard as possible. Once something like $500 or a $1,000 builds up in your Digit account, its probably best to transfer it somewhere where you’ll get a better return.

No Comments yet!