Since Dual Income No Kids is a personal finance blog, I wanted to take a few minutes to share our own personal wealth building journey. My wife and I sit down every few weeks and review our budget and net worth. Here is what the figures looked like at the beginning of August 2019.

For those of you who don’t want to read the whole post, here is the story: net worth of $828,000 driven by stocks and real estate.

Where things stand:

Net worth: $828,000. The bulk of our assets are in stocks, our online business and real estate. My wife owns an investment condominium free and clear and we’ve got about 10% equity in our home.

Colors in doughnut charts indicate: purple = real estate and business assets. Orange = mortgage.

Colors in doughnut charts indicate: purple = real estate and business assets. Orange = mortgage.

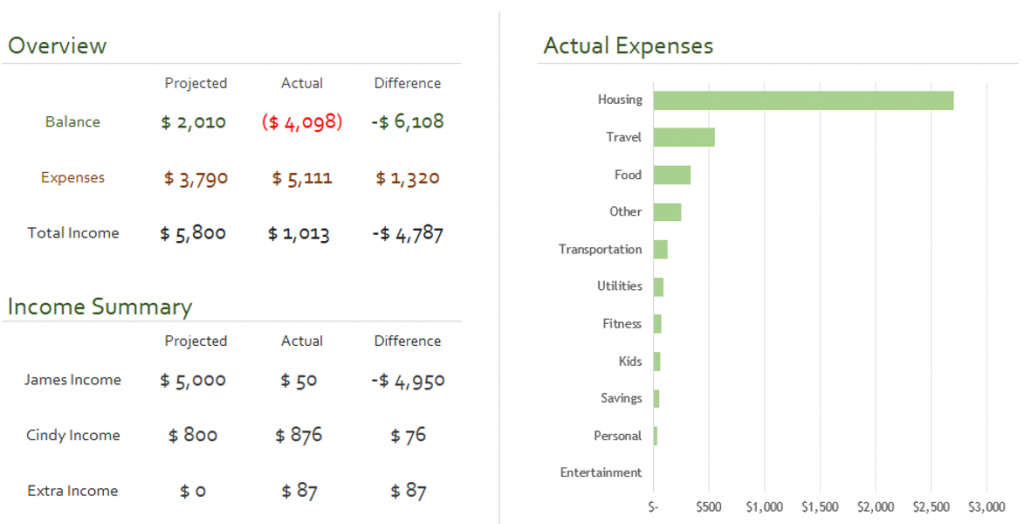

Budget: The figures here are super preliminary but we’re heavily in the red this month due to a decision to allocate some of our savings to pay off my credit card debt.

The budget figures here are incomplete and preliminary because we calculated them at the start of the month. However, they are substantively accurate. We basically decided to use our savings this month to fund our current bills so we could divert most of my income to paying off some credit card debt. Drawing down our savings is frankly a source of added stress, but its better than the 20% interest the credit cards are charging us.

Thoughts:

Whats killing us is our housing costs – we’re running at about $2,700 per month in housing costs. This is our #1 expense, its mainly our mortgage, plus taxes, PMI and a condominium fee. Our main goals at this point are to pay down our mortgage and apply to have the private mortgage insurance taken off. This should whittle our housing costs down to $2,400. Its not a game changer, but slow and steady progress is just fine.

Lessons Learned:

These things have historically driven our net worth.

- Stock appreciation

- Investing in real estate

- Saving money

- Avoiding/eliminating debt

This is what hasn’t worked well for building wealth.

1. Shifting assets around. I’ve tried shifting assets around to meet larger goals. For example we sold some of my silver to pay off some credit card debt. That said, the best approach is probably limiting spending, saving and investing.

2. Precious metals. We’ve invested in gold and silver, but haven’t necessarily seen explosive growth in these assets.

3. Bonds. We have some of our savings in bonds. Bond are excellent for safety, wealth preservation and income, but we haven’t necessarily seen explosive growth in their value. So, our personal experience is basically inline with the historical performance of this asset class.

Readers, if you have any thoughts, please leave a comment below.

Here are more articles on the mechanics of getting head financially:

Building Wealth on $600 Per Month

Ways To Make Extra Money

The Pros and Cons Of Investing In Mutual Funds

Oh wow! Congratulations on all of the hard work. Thanks for being so open to share!

Gina – thanks a ton. I’m kicking myself a bit for letting my credit card debt levels climb so high.

I totally ran into trouble with them in my 20s and I should have known better.

Pingback:An Honest Credit Check Total Review - Dual Income No Kids | Dual Income No Kids