James Hendrickson is an internet entrepreneur, blogging junky, hunter and personal finance geek. When he’s not lurking in coffee shops in Portland, Oregon, you’ll find him in the Pacific Northwest’s great outdoors. James has a masters degree in Sociology from the University of Maryland at College Park and a Bachelors degree on Sociology from Earlham College. He loves individual stocks, bonds and precious metals.

Janus, ancient Roman god of war. Image source: Wikipedia.

This posting is on what to do with your personal finances in the event of war. And to be even more specific, this article is about a war happening in the borders of your country. Not one happening far away from you that your country is involved with.

Wait, isn’t this topic ridiculous? Wars just don’t happen that much these days.

No.

While it is true that wars, industrial accidents, and crime have become increasingly rare in the last 100 years, even rare events like war can and do happen frequently.

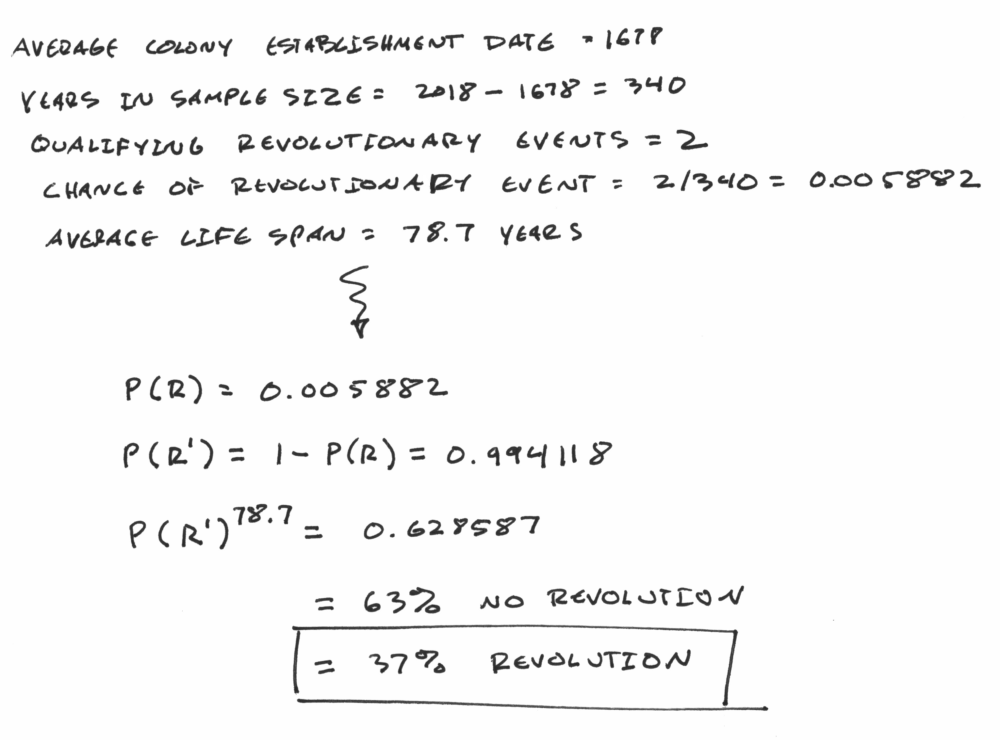

The Chances of a Revolutionary Event: 37 percent

In a little-noticed 2018 analysis, hydrologist BJ Campbell gave a very tight synopsis of the chances of a violent revolution in the United States in his article “The Surprisingly Solid Mathematical Case of the Tin Foil Hat Gun Prepper“. Noting that there have been two major revolutionary events in the United States since the country’s founding, he calculated a 37 percent chance that any American of average life expectancy will experience at least one nationwide violent revolution. Here is his math:

Wealth Destruction Is An Enduring Part of Human Condition

In the 1980s, historians Will and Ariel Durrant synthesized some of the major findings of recorded history in their book The Lessons of History. They noted that out of the last 3,421 years where reliable historical records exist, just 268 had no wars. So, while conflict has been absent from the post-war finance literature, it is an enduring part of the human experience for virtually all of recorded history.

So, What To Do With Your Money In Case Of A War?

With notable exceptions, this topic has been largely ignored by the investing community. This is possibly because professional investors tend to not have military experience or have spent substantial time in countries with a history of political instability.

The only really through work on this subject is Barton Biggs’ seminal book Wealth, War and Wisdom. Biggs, now deceased, was a Yale graduate, U.S. Marine Corps veteran, Morgan Stanley executive, and hedge fund manager. Wealth, War and Wisdom is one of the only thorough books on how wide-scale military conflict impacts personal finances. Biggs looked at the impact of the Second World War on stock markets and discussed how wealth was preserved in Europe during the 1940s.

So, to answer the question of what to do with your money in case of war, let’s review each of the asset classes below in light of Biggs’ discussion. We’ll add in some relevant historical and contemporary examples.

The ultimate conclusions are diversify and get out of the way.War is profoundly destructive for wealth building, and it is remarkably worse if your country is on the losing side.

By asset class:

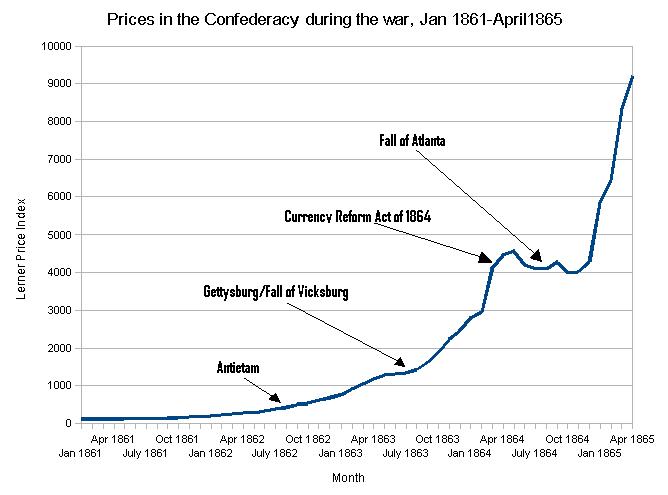

1) Cash: Wartime inflation and taxation usually substantially undermines the value of cash holdings. For example, cash proved to be a poor asset class during the Second World War. Inflation soared as high as 30 percent in France, 40 percent in Italy, and 50 percent in Japan — wiping out of the value of these currencies. In the United States, income taxes were raised to its highest historical levels — 94 percent on incomes above $200,000 — and inflation jumped as high as at 14 percent. The inflation numbers are historically consistent with what’s known about the U.S. Civil War. Here is a chart of the Lerner Price Index in the Confederate States of America between January 1861 and April 1865. Essentially, confederate money became worthless during the conflict period.

Source: Wikipedia.

2) Precious metals: Gold and silver work well as a means of protecting small amounts of wealth. However, large amounts are almost sure to be confiscated or stolen. As they were during the German and Russian occupations of Europe during the Second World War.

3) Bonds:Depending on where you live, the performance of bonds can suffer a great deal during wartime. Between 1900 and 1949 bonds issued by Axis governments returned a negative -96 to -98 percent return. In contrast, bonds issued by Allied and neutral powers had average returns of 1.8 percent.

4) Real estate: During World War II, if you were on the losing side, physical real estate (houses and buildings) were generally not good assets to hold. Real property in Poland, France, Belgium, Denmark, and Eastern Europe was frequently confiscated or destroyed in the fighting. By the end of 1944, virtually no rents were paid on land or buildings in continental Europe. During the American Civil War, nearly 20 percent of all major plantations were destroyed. On the other hand, small, out of the way farms generally avoided destruction, at least during World War II and provided a good way to both preserve wealth and provide for yourself.

5) Equities: Even during World War II, stocks outperformed all other asset classes in countries which were directly impacted by the war. This was the case for both the Axis and Allied powers in World War II. However, performance depended largely on whether or not the country won or lost the war. Among countries victorious in World War II, stocks showed a 4.2 percent real return between 1900 and 1949. Among those countries that lost World War II, or were occupied, real returns of up to -26 percent were evident.

6) Personal property: Generally speaking looting in conflict zones is common, so personal property such as art, valuable collectibles, etc. are likely to be stolen by occupying powers. However, as Biggs warns, even if valuable personal property is able to be sold, it is often at a fraction of the item’s true value.

7) Cryptocurrency: Cryptocurrencies are vulnerable in wartime in two regards. First, they depend on localities having sufficient electrical power to access cryptocurrency exchanges. Recent experience in Venezuela suggests this isn’t always the case, per the BBC. Second, cryptocurrencies under the control of large corporations or national governments are vulnerable to confiscation. Fully 29 percent of global cryptocurrency trading takes place within the United States and “know your customer” regulation has increased substantially in the United States, elevating possible confiscation risk.

Practical Advice On What To Do With Your Money In Case Of War

Biggs offers some practical advice for safeguarding your wealth in the event of war:

Diversify your wealth by moving at least 5 percent of it out of the country. Be careful of Swiss banks, they require strict documentation that is often not available post-conflict

Buy a small farm with 5 percent of your wealth. This should be in an out of the way location

Put 5 percent of your wealth in TIPS (Treasury Inflation-Protected Securities), inflation is common in countries experiencing warfare

Be sure your stock holdings are diversified. Don’t put all of them in computerized databases in the giant banks — go paper instead. Be sure the stock is in your name, not in the “street name” or the name of the brokerage. Focus on global equities. If you’re holding domestic stocks, you’re going to get wiped out. Plain vanilla index funds are fine.

Pay attention to stock markets. Markets have generally done a good job signaling when wars turn around

Hold gold and silver outside of the country. Keep only a small amount at home

Diversify your currency holdings. Carefully consider what currencies you want to hold and where you want to hold them

To briefly wrap this up — both Wealth, War and Wisdom and math behind the long run human experience suggest that war is more common and more destructive than we’d like to admit. The best thing you can do is diversify your assets and get them out of the way of the conflict by moving them out of the country.

Source: Barton Biggs, Wealth, War and Wisdom. Wiley. 2008.

I was reading Loral Langemeier a few years back. She’s a big advocate of direct investing in business opportunities like self-storage, rental real estate, and oil wells.

The idea of buying an oil well intrigued me. So I started looking around online. Some small wells can be had for around $200,000 to $1,000,000. This type of business works based on how much oil/natural gas, etc., you can get out of the ground. The sizzle is that wells can be extremely profitable, especially when gas prices are high.

Since I don’t have $200,000 to $1,000,000 in cash lying around, this is probably going to be a project for 5 to 10 years down the road, but I’m definitely interested. It looks like a great money-making opportunity that could allow one to significantly build their wealth. In case you’re also interested, here is where to buy a well, and some alternatives if you can’t afford to buy one directly.

Where To Buy A Well And What To Consider

Most wells appear to be sold by brokers, so if you want to cruise some of the listings, check them out here.

The only book I’ve been able to find on buying oil wells is Investing In Oil Wells by Nick Slavin. It retails for $12.99, but if you are going to drop $5,000 to $20,000 on fractional ownership in a well, $12.99 and some education is probably worth it. You can get the book here.

There are some factors to consider. Oil and gas wells are capital-intensive – they cost a lot to operate and maintain. Oil is also heavily regulated, so when a well stops producing, you need to cap it to prevent damaging the environment. Capping is extremely expensive – costing between $20,000 and $80,0000. So, they cost a lot to drill, maintain, and close.

Also, wells are risky. So, what a lot of investors do to avoid risk is to buy several wells. This, of course, requires a lot more capital and management time. For example, buying several wells at $200,000 each could cost millions of dollars.

Alternatives To Direct Ownership

Since the costs of owning wells directly are prohibitive for most investors, here are some alternatives if you want direct exposure to oil and gas:

Buy Royalties: Royalties are basically payments made to individuals for the right to use their natural resources. What often happens is that an oil company will agree to pay a landowner a given payment per barrel of oil or gas extracted. For example, if a landowner’s property produces 100 barrels of oil a month and the royalty agreement between the extraction company and the landowner says the owner gets $2 per month, the landowner would get 100 x $2, or $200 per month. Royalties can be bought and sold. If you want to get some, Energynet is a good place to find royalties to buy.

Buy Oil and Gas Stocks: A simple and straightforward option is to buy the common stock of oil and gas companies. Owning shares of major companies like Exxon (XOM), ConocoPhillips (COP), or Phillips 66 (PSX) is a good way to get exposure to oil wells. Similarly, exchange-traded funds (ETFs) that focus on the oil industry are good ways to get exposure.

2025 Oil Market Trends

Oil prices have fallen to around $65 per barrel as oversupply and slowing demand weigh on markets. While this creates opportunities to acquire wells at lower valuations, investors must weigh the risks of stricter environmental regulations and costly well closures. Industry growth is shifting toward enhanced recovery techniques and eco-friendly production methods, while geopolitical tensions continue to drive short-term volatility. For most individual investors, indirect exposure through royalties, stocks, or ETFs remains the more accessible path to participate in the energy sector.

To Buy or Not to Buy: It Depends

Buying an oil well may sound like a ticket to instant wealth, but in 2025, the picture is more complex. Oil prices have retreated to around $65 per barrel, creating lower entry costs but also slimmer margins compared to past boom years. At the same time, stricter environmental regulations and expensive well-closure requirements mean investors must plan for long-term costs, not just short-term profits.

For most individuals, direct ownership remains a high-risk, capital-intensive venture best suited for seasoned investors with millions to deploy. Alternatives such as royalties, oil and gas stocks, or ETFs provide more accessible ways to gain exposure without the operational headaches.

Ultimately, the opportunity lies in understanding both the sizzle and the risk. Oil wells can indeed generate significant returns, but only for those prepared to navigate volatile markets, regulatory hurdles, and the realities of energy’s shifting future. For everyday investors, indirect strategies may offer the smarter path to participate in the oil economy while keeping risk manageable.

When I was a child used to read the Duck Tales comics, which were the story of Donald Duck and his family. Donald’s Uncle, Scrooge, was a billionaire with a massive money bin full of coins that he’d go swimming in. This got me thinking, how much would it take to fill up his money bin – probably a lot. And, what kind of coins would do it – probably a lot. I’m thinking 600,000 in pennies. And how much is 600,000 pennies in dollars, anyway?

How Much Is 600,000 Pennies Worth?

Doing the math is pretty simple. As part of the Coinage Act of 1792, Congress set the value of a dollar at 100 pennies. So, you simply divide 600,000 by 100 to get the number of dollars. Or, 600,000 / 100. This gives you $6,000.

So, how many dollars is 600,000 pennies? It’s $6,000.

Here Are Some Interesting Facts About Pennies

1. Pennies were historically made out of 100% copper. However, modern pennies are mostly made out of Zinc. Only 2.5% of a modern penny is copper.

2. Before 1850, pennies were made out of copper from Cornwall, England. After 1950, the mint used copper from Michigan.

3. Per Wikipedia, pennies used to be much larger. For example, in 1857, the penny was about the size of a Susan B Anthony dollar. Pre-1857 pennies looked about like this:

4. Modern pennies weigh about 2.5 grams. Thus, 600,000 pennies weigh about 1.5 million grams. This translates to 3,306 pounds and 14.9 ounces.

5. There are 84,480 pennies in each mile. This is because 16 pennies laid side by side constitute 12 inches, or one foot. And since there are 5,280 feet in one mile, that gives us 16 * 5,260, or 84,480 pennies in a mile.

6. Unlike other coins, pennies have smooth edges.

7. Due to changing commodity prices, sometimes the value of the copper in pre-1982 US pennies is worth more than its face value. However, melting down pennies is against U.S. Treasury regulations and could get you into trouble.

8. The official U.S. Mint’s name for the penny is the “cent”. The official name from the U.S. Treasury is a “one-cent piece”. The colloquial term “penny” is not an official US government designation.

9. The most valuable pennies are wheat pennies from 1943 and 1944. Some of these have a very high value for collectors. For example, the 1943 D Lincoln Wheat Cent Bronze/Copper shown below has a price tag of over $2,000,000.

10. Pennies are great for talking about compound interest. Saving Advice has a great article that asks if you’d rather have a million dollars or a penny doubled every day for 30 days. Hint: You want to choose the penny doubling every day for thirty days. At the end of the 30 days, you’d have $5.36 million.

The Future of the Penny

The penny’s long run has officially come to an end. On November 12, 2025, the U.S. Mint struck its final batch of one‑cent coins, closing the book on more than 232 years of production. Rising costs were the driving factor: while a penny is worth one cent, it has cost the Mint between 1.42 cents and 3.69 cents to produce each coin in recent years. With cash usage declining and billions of pennies already in circulation, the Treasury determined that continuing production was unsustainable.

What Happens Next

Legal Tender: Pennies will remain legal tender indefinitely. You can still spend them, deposit them, or save them.

Circulation Shrinkage: With no new coins being minted, the supply will gradually shrink as pennies wear out or are lost. Retailers may begin rounding transactions to the nearest nickel.

Collector Value: The final 2025 pennies are expected to become collectibles, especially uncirculated versions from the Philadelphia Mint. Older copper pennies and rare wheat cents may also rise in value as interest grows.

Cultural Shift: For generations, pennies were used in coin flips, lucky fountains, and everyday transactions. Their disappearance marks not just a financial change, but a cultural one.

Bigger Picture

Ending penny production reflects broader trends in digital payments and cashless commerce. As Americans increasingly use cards and mobile wallets, small‑denomination coins have less relevance. The penny’s retirement is both a cost‑saving measure and a symbolic step toward a more modern financial system.

While 600,000 pennies may only add up to $6,000, the exercise reminds us that even the smallest denominations can carry big lessons. From their quirky history and surprising weight to their role in teaching compound interest, pennies prove that money isn’t just about face value—it’s about how you use it. Just like Uncle Scrooge’s money bin, the real treasure isn’t the coins themselves, but the financial wisdom they inspire. Whether you’re stacking pennies or building wealth through smart saving and investing, the principle remains the same: small steps, multiplied over time, can lead to extraordinary results.

Looking for ways to make some extra money? We thought it would be fun to share some things we’ve done to make extra money on the side.

We’ve continually updated this posting, so its way more than 9 ways, we just don’t want to change the graphic.

1) Do Surveys:

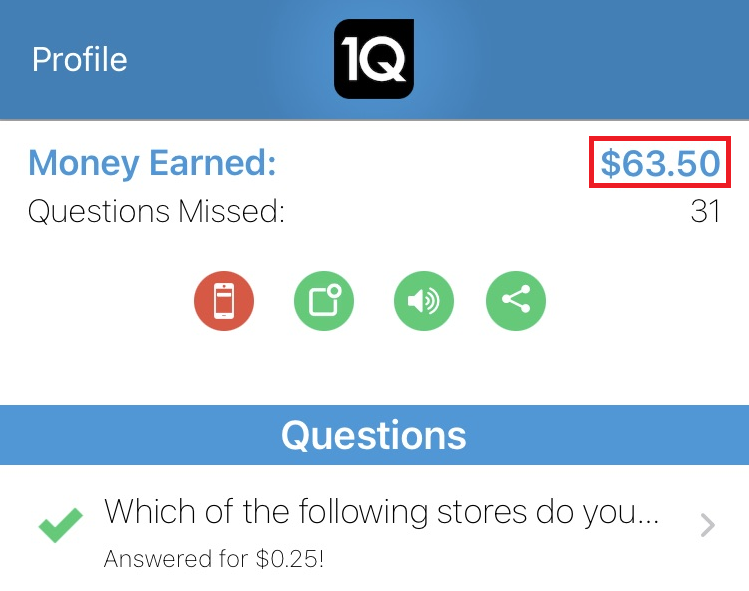

This is a classic. Doing surveys won’t make you rich, but it’s a good way to get a little bit of extra residual income in your spare time. Plus if you dump the money into a retirement account, you could be eligible for the savers credit. Most of the survey companies don’t pay well at all. An exception is 1Q. They pay 25 cents per QUESTION, which is about ten times more than other apps pay. They also payout right away to Paypal, which is excellent. Money in your accounts today is worth more than money in your accounts tomorrow.

Definitely get this app.

2) Invest For Income:

For a while we DINKs held stock in Exxon Mobile and Johnson Controls through a dividend reinvestment program. We got in initially for around $250 bucks for each of these stocks, and enjoyed a modest, but noticeable dividend. Most recently I’ve been buying bonds via SMBX – which is a nice solid way to pick up a few extra bucks a month.

Edit: 2025. In 2022 the brokerage industry has changed a lot, there is a ton of venture capital money sloshing around in the stock market. As a result, several companies are now offering “get paid to sign up” type offers. Basically, these companies are offering a trade. You sign up and link your bank account, and in return you get a share of stock or two. There are two that don’t require you put money into their system. These are:

Of these Robinhood is the best. It has very fast execution and delivers on its promises.

Oh, as a side note another good fintech app which I actively us is Ark7. They’re a neat little fractional ownership of real estate app. These kinds of app are good if you don’t have enough money to buy a house yourself, but you want the passive income that comes from owning real estate. You can sign up for them here.

3) Hold a Garage Sale:

Back in 2006 we cleaned out the closets, called a couple of friends and put on a yard sale. We ended up getting a couple of hundred bucks. Not a lot, but it reduced the clutter and was a fun thing to do on a Saturday. This hasn’t really been a thing during the pandemic, but its a good way to declutter. You could also try selling your stuff on decluttr.com. If you want a good resource on which items sell better a yard sales, read mystayathomeadventures article on the topic, here.

4) Sell Your Personal Data Online:

Due to regulatory changes in Europe and the U.S., a number of startups are now paying your for browsing history, spending history and demographic data. These payments aren’t much, but they have a couple of upsides. First, they’re totally passive. Once you sign up for the service, you just have to check in and collect every couple of months. Second, these companies generally sell your data to marketers, which is mostly happening without your consent anyways. So you’re not losing much in terms of your privacy. The ones that actually work are:

There are a ton of companies that will buy your spare internet bandwidth for between 50 and 10 cents per gigabyte. What these companies do is set up private proxy networks and sell the bandwidth to businesses for research or other purposes. This is a solid option if you’ve got unlimited bandwidth and want to defer the cost of your internet. They also have the virtue of being largely passive – you just have to check the balances and collect when you have enough revenue.

All of these are worth between $2 and $5 per month.

6) Sell Things on Craigslist or Facebook Marketplace:

A couple of years ago, we found a microwave in the mailroom of our building, we ended up cleaning the thing up, snapping a couple of pictures and putting an ad up on craigslist. The microwave sold the next day for twenty bucks. Not bad. One thing to note here: most of the action is moving from Craigslist to Facebook Marketplace.

7) Negotiate a Raise:

Some people are great about this. What they do is change jobs every two or three years, and each time they change jobs they end up negotiating a raise. Even factoring in taxes and expenses associated with changing jobs, the higher income levels usually make it worthwhile.

8) Start a Blog:

Blogging isn’t what it used to be – there is something like 1 website for every seven people on the planet. At one point we had figured that our hourly wage from working on Dinks was about a $1.85, but hey – it gives us something to do and is a way to have an impact and stay connected. Note as well that our blog income generation has increased as we’ve put energy into doing so.

The great thing about blogs, is you can also sell them. Blogs can sell for something like 5 to 10 earnings, so if you make $100 a year on your site, you could sell it for $500-$1,000. Blogs are also nice because once your site has traffic and you have advertising installed, its pure passive income.

9) Sell Your Body to Science:

If you are in a big city like Washington DC, or Chicago you are in luck. Large research hospitals are typically constantly running a number of research studies. Some of them pay well. We’ve both participated and have been rewarded with some modest checks from the federal treasury for the federal studies we’ve participated in. If you don’t mind being poked and prodded, you can always participate in research studies.

Check your local newspaper or University advertisements.

10) Rent Out a Room:

If you have a spare bedroom in your house or apartment. You might consider renting it out. A bedroom in a decent place can go for $500-$800. The extra bucks could really help improve your bottom line. But, be careful to screen your roommate, you don’t want to get someone messy or a deadbeat who won’t pay your rent! The modern way to do this is via Airbnb.

11) Take Advantage of Grocery Apps:

There are number of good ones. Ibotta is the most common one. How it works is you can either scan your receipts for cash back or you can directly link your loyalty cards to it. This gives you a minimal percentage back – most people get 10 to 20 bucks a month back. Not a lot, but it adds up. Their sign up is pretty easy => check it out here.

The one app that you definitely want to get is the Amazon Shopper Panel. This one gives you .15 cents for each receipt you scan up to $10. That is an excellent rate. As a result, everyone and their mother wants the app, so there is a waiting list. Get it on and try back every week.

12) Sign Up For Class Action Lawsuits:

I regularly sign up for any of these I’m qualified for. We recently got a 90 dollar check from a class action lawsuit regarding using debit cards at BP gas stations. You won’t get immediate cash, but if you work this, you’ll get a couple of hundred extra bucks a year. Consumeraction.org has a pretty solid listing of open lawsuits.

13) Look For Unclaimed Money:

State and local governments administer a fair amount of unclaimed funds. Most of this is just sitting around, waiting to be claimed. So, there is no good reason to not check and see if you’re owed something. The place to check is: The National Association of Unclaimed Property Administrators.

14) Credit Card Cash Back Promotions:

The typical amount in cash back is 1%, if you’re lucky. Certain credit cards like Discover have quarterly promotions that can give you up to 5% cash back in certain categories. Some other cards do promotional cash back quarterly, but if you track the rewards and don’t carry a balance you can get 1 to 3% cash back. Sometimes you can also exchange the cash back rewards for a higher dollar amount in gift cards. This is most lucrative during the holidays. BE SURE TO KEEP YOUR CARD PAID OFF!

15) Drive A Taxi/Do Food Delivery:

In the past couple of years, companies like Uber and Lyft have been good at breaking up local taxi monopolies. Provided your car is in good shape, you can always sign up with one of these companies. Uber in particular has an easy sign up process. They’ve got a couple of options, you can drive an Uber taxi or you could sign up for Uber Eats food delivery service. They won’t make you rich but you can hustle an easy extra $150 to $300 a month with Uber.

Finally – don’t neglect the basics:

Of course, if you want to make real money you should probably consider investing seriously in stocks and real estate, as well as reduce your expenses by budgeting and saving like a fiend.

Additional Reading:

Finally if none of these ideas work you, and you’re in college consider reading Dollar Sanity’s list of ways to make money as a college student. Its geared for students, but its got some ideas that apply to everyone. They also have a good review article on this subject.

A while back I read a story about a local Lions club that was asking for pennies for charity. They wanted to raise something like 1 million pennies to help a little league rebuild its ballpark. The club was asking for pennies because they aren’t worth much and people are willing to donate them (here). So…It got me thinking. How much is a million pennies worth, really?

The answer is: a million pennies is $10,000 dollars.

How Much Is A Million Pennies Worth?

The math is pretty simple.

Per the coinage act of 1792, each US dollar is worth 100 pennies (clicky). So, you simply divide 1 million by 100 to get the number of dollars. Or, 1,000,000 / 100. This gives you $10,000.

So, how many dollars is one million pennies? Its $10,000.

Here Are Some Fun Facts About Pennies:

1) Pennies are made out of 2.5% copper, with the rest made out of Zinc.

2) Between 1828 and 1848, pennies were made out of copper from Cornwall, England. After 1850 the mint used copper ore from Michigan.

3) Per Wikipedia, pennies used to be much larger. For example in 1857 the penny was about the size of a Susan B Anthony dollar.

4) Each penny weighs about 2.5 grams. Thus, a million pennies weigh about 2.5 million grams. This translates to 5,511 pounds.

5) Pennies are 1.52 millimeters thick. If you stacked a million pennies on top of each other, they’d be about .94 miles tall.

6) Pennies have smooth edges.

7) Due to changing commodity prices, sometimes the value of the copper in US pennies is worth more than its face value. But, don’t think you can find a bunch of pure copper pennies and melt them down. Per the Federal Register, this is against treasury regulations and could get you into hot water (click here if you want to read the regs yourself).

8) The most valuable penny you might find in circulation today is the 1983 double die reverse. The word “double die” refers to an error in the minting process whereby the coin is struck twice. This causes the coin’s design to slightly overlap. For the 1983 pennies, the error is on the back where it says “ONE CENT”. Here is an image of what this looks like:

Image source: Ebay.com

9) There are lots of pennies. There are about 130 billion pennies currently in circulation. In 2020 the Mint produced about 4.4 billion pennies.

10) In 2025, The Trump Administration announced it was planning on getting rid of the penny. This is because the penny costs 3.7 cents to manufacture, meaning the government looses money on each penny it produces. Its unclear if the Administration can do this via executive order, as some legal analysts feel only Congress can abolish the penny, see the PBS story on this.

By way of a conclusion, pennies are great for talking about compound interest. Dividend Power has a great article that talks about what happens when you double a penny every day for 30 days. Hint: In effect it says that compound interest is so powerful that at the end of 30 days you’ll have more than $5.3 million dollars…

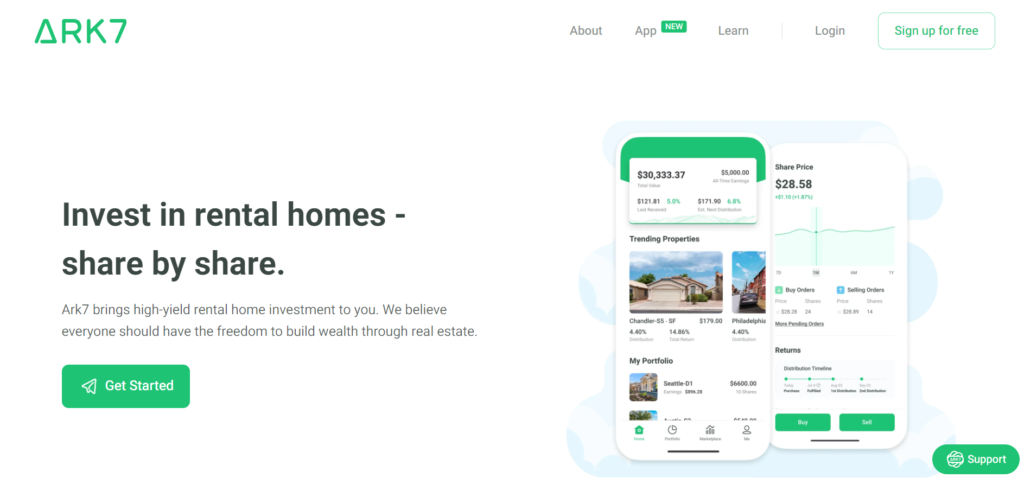

Ark7 is a real estate investment platform that has gained popularity in recent years. It offers investors the opportunity to own shares in income-producing properties without the hassle of being a landlord or dealing with the complexities of traditional real estate investing. In this comprehensive Ark7 review, I will take a closer look at Ark7 and examine if it’s worth your time.

Ark7 Summary

The Dinks Ark7 Summary

Ark7 is a fintech start-up with mobile and browser applications. The company buys rental property with an LLC and issues shares to investors. Ark7 then takes a management fee and manages each property on behalf of its investors. The company is new but well-suited for risk-tolerant investors who want a geographically focused investing strategy.

Real estate investing has long been considered one of the best ways to build wealth and generate passive income. However, for many people, investing in real estate is out of reach due to high transaction costs and significant paperwork requirements. Ark7, at its core, is a solution to this problem. It allows investors to access real estate markets without requiring large amounts of capital.

Ark7 is a real estate crowdfunding platform that was founded in 2017 to democratize real estate investing. The platform allows everyday investors to access high-quality real estate deals that were previously only available to high socioeconomic status or institutional investors. While the platform has fees and is less flexible from a taxation standpoint, it is suitable for investors who want to invest in a targeted geographic manner.

What is Ark7?

At its core, Ark7 is a platform that allows investors to purchase fractional shares in properties. What Ark7 does is buy a property, put it under a corporate umbrella and issue shares in the corporation. This means that investors can own shares in a corporation that owns a property, rather than having to purchase the entire property themselves. By pooling their resources with other investors, individuals can invest in high-quality real estate deals that they may not have been able to access on their own.

Ark7 was founded by Andy Zhao (an ex-Google engineer), James Weng, and Lynn Yang who recognized the potential of real estate investing for building wealth and generating passive income. They wanted to create a platform that would allow everyday investors to access real estate markets with more ease and lower cost than existing markets allowed for.

How Does Ark7 Work?

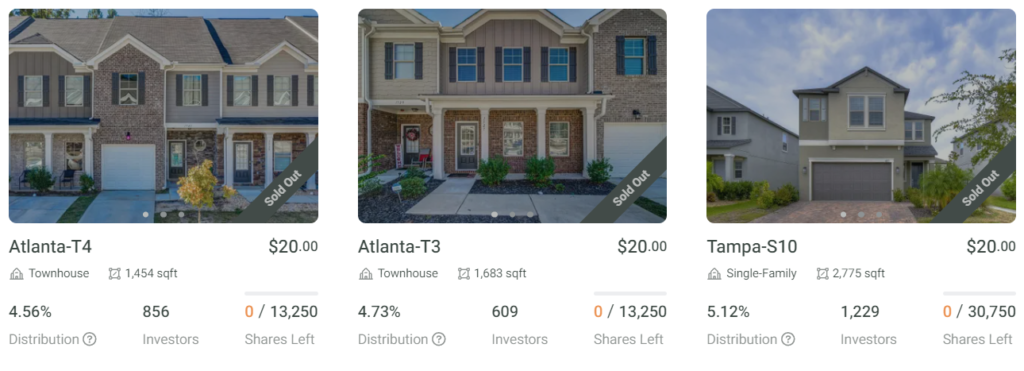

Ark7 is a fintech start-up with mobile and browser applications. Ark7 buys rental property under an LLC and issues shares in that LLC that sell at varying prices based on the underlying economic value of the property.

Share prices are determined by the property’s value and can vary a great deal across markets. Ark7 allows the securities to be traded and has options for holding your investment in an IRA.

When you buy shares in the LLC, you receive a part of the monthly property income proportionate to the percentage you own. For example, if you owned 10,000 shares in a property and there were 20,000 shares outstanding, you’d be entitled to 50% of the income, less fees.

Rental properties listed on Ark7 are located in various real estate markets and cities around the country. Ark7 is active in ten states with a good amount of market data for app users to review. The company requires a three-month minimum hold on its properties. Users are provided a very consumer-friendly user exchange to peruse, analyze, and buy into properties, as well as monitor the investments they make and track dividend payments. The company indicates it has close to 90,000 active users, pays out $1.4 million in dividends monthly and its portfolio is worth around $19 million. Its securities are registered with the SEC.

Ark7 is a full-service organization. The company manages all the real estate, including collecting rent and dealing with any necessary property management and maintenance. For these services Ark7 charges between 8% and 15% of the rental income. Ark7 offers retirement accounts and opportunities for accredited investors.

Key Features of Ark7

As an emerging fintech, Ark7 has some features that other fractional ownership of real estate companies do not. These are: offering highly specific investment opportunities and a high degree of operational discipline.

Highly Specific Investment Opportunities

One of the key features of Ark7 is the highly specific investment opportunities that it provides to investors. The platform offers access to a range of different types of properties, from single-family homes to multi-unit apartment buildings. This diversity of investment options allows investors to tailor their portfolios to meet their investment goals and risk tolerance.

Tailoring investment goals and risk tolerance usually means diversification, but not always. Unlike other REITs or fractional ownership apps, Ark7 allows budget-conscious investors to make highly targeted investments.

For example, if an investor felt that single-family homes in Texas were likely to outperform other asset classes, they would be able to execute a strategy around this using Ark7. In contrast, companies such as Fundrise, which issue shares in a pool of assets, are not able to provide this level of exactness.

Very Good Operational Discipline

Ark7 exercises a high degree of discipline in its internal operations. For example, for each property in the Ark7 marketplace, the company will look at over 1,000 possible opportunities. Ark7 usually uses three factors to evaluate opportunities: the presence of massive socioeconomic development, population growth, and pro-growth domestic policies.

Ark7 also thoroughly vets local real estate market conditions and communities around the candidate property. Its team looks for nicer homes in communities with good accessibility, good public schools, and a pleasing appearance. It also looks at neighborhood comparables, such as local rental rates, and local policies on renting, zoning, and other natural factors (Coinmonks.com).

In addition to highly focused investments and good operational discipline, Ark7 has several other advantages.

User-Friendly Platform

In contrast with competing apps such as HappyNest, the Ark7 platform is easy to use and navigate, making it accessible to a range of investors. The platform is also well-designed, with clear and concise information about each property and the investment opportunity it presents. The user interface is intuitive, and investors can easily track their investments and the income generated.

Investing in real estate can be complicated, but Ark7 makes it simple. The platform provides investors with all the information they need to make informed investment decisions, and the user interface is designed to be user-friendly and accessible to everyone.

Using Ark7

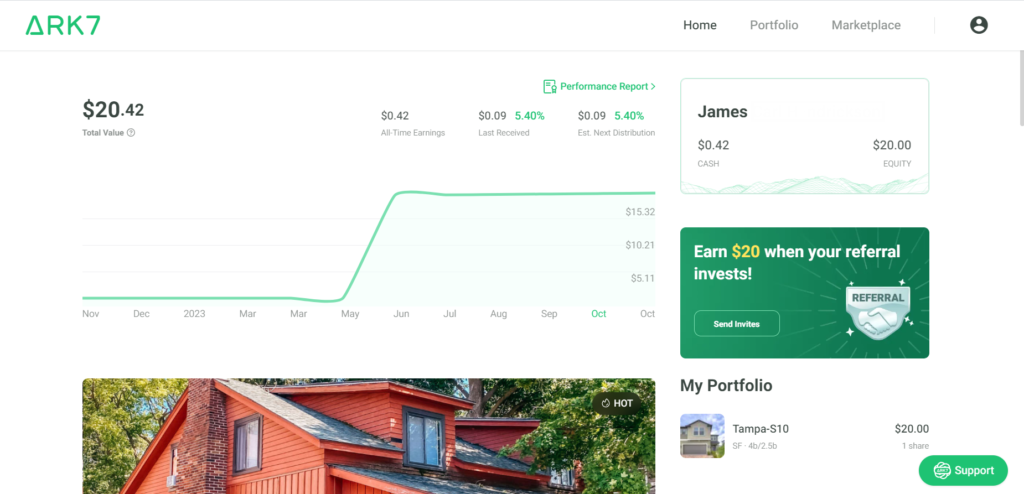

After you open an account you’ll get a dashboard that looks like this.

The dashboard shows you a bunch of properties, as well as the cost of a share, your total portfolio overview, and some tabs to access the marketplace and your portfolio. When you click on a property it will give you information about its location, conditions, share pricing, and cash distribution data.

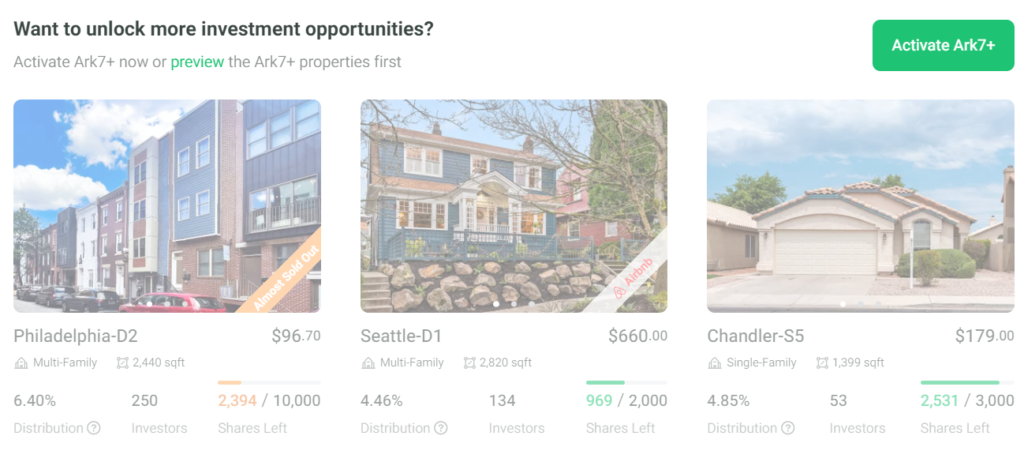

Most of what is available to retail investors on the platform are single-family homes. To get access to commercial and multifamily properties, you’ll need to be an accredited investor. Ark7’s channel for accredited investors is called Ark7+. The Ark7+ accredited investor opportunities are greyed out until you apply, see here:

In general, their interface is simple and well-designed. Money deposited is credited promptly.

Good Quality Investments

One of the biggest advantages of using Ark7 is the access it provides to good-quality real estate investments. The properties in the Ark7 app are all typically newer, well-maintained properties in good neighborhoods. You’re not buying trailer parks or $500 houses in Detroit.

Diversification

Most fractional ownership real estate apps offer diversified real estate investments. Ark7 is no exception. It offers a diversified portfolio of real estate investments, reducing the risk of any one property underperforming. This diversification provides investors with more stability and security in their investments. Moreover, investors can choose from a range of investment options, including long-term holds, short-term flips, and more.

Returns: How Much Does Ark7 Pay?

Ark7 generates income for investors in two ways:

monthly rent payments

capital gains.

As of the time of this writing, listed properties on the Ark7 marketplace were paying annualized rent payments of between 4.5% and 7.3%, and capital gains appreciation rates between 4.1 and 20.7%.

In Ark7 both sources are essentially passive for investors. While some effort is required to select and monitor investments, as well as communicate with the Ark7 team, small investors don’t need to spend much time beyond some initial due diligence and ongoing investing monitoring.

Ark7 also offers IRA options. Their IRA options allow your returns to grow in tax-advantaged accounts. This increases the real returns of the investment because the impact of taxation on profits is lessened or eliminated. With Ark7 the accounts are held in custody for you. You hold the assets in the account because you aren’t involved in the day-to-day management of the companies running your properties – making them suitable for being held in an IRA.

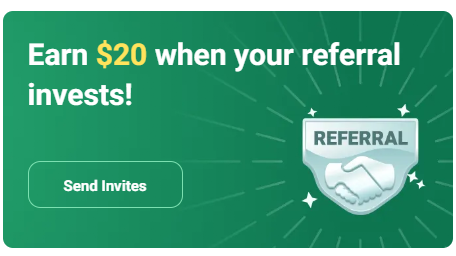

Referral Program

Since Ark7 is in a growth phase, they have a generous referral program. If you sign up, you can pick up some extra money by getting a friend to join — you’ll both get $30. Thirty dollars isn’t a lot, but when you factor in a couple of years of additional passive income the $30 gives you, it starts to look worth it. You can sign up here.

Potential Drawbacks of Ark7

Ark7 has several potential drawbacks.

The Platform is New

Ark7 was founded in 2019. Running a high-growth fintech startup is notoriously difficult. About 80% of fintech startups fail within the first 15 years of business operation. And, while Ark7 is a relatively new investing platform with an interesting business model, it has not yet stood the test of time.

Lack of Managerial Control

One potential drawback of using Ark7 is the lack of control that investors have over their investments. As fractional owners, investors have limited control over the underlying property and its management. This lack of control may be a concern for some investors who prefer to have more control over their investments.

Risk of Capital Loss

In addition, while Ark7 offers a diversified portfolio, there is still a risk of loss associated with real estate investments. Real estate values can fluctuate, and unexpected events such as natural disasters or economic downturns can negatively impact the performance of real estate investments. Investors should be aware that Ark7 investments could lose up to 100% of their value.

Lack of Leverage

Traditional real estate investing allows owners a high degree of leverage. Take for example the case of a homeowner who buys a house for $100,000 and puts down $20,000. If the value of the house grows to $150,000, the homeowner has received an investment return of 250%. The amount of leverage an Ark7 share provides is unclear as the platform is still new, however, it is likely less than directly owning real estate.

Unclear If You Can Borrow Against Your Ark7 Shares

One advantage of traditional real estate is the ability to borrow and use your real estate as collateral. Borrowing is the principle underlying mortgages, home equity lines of credit, and the like. The ability to borrow is non-trivial. Many high-net-worth investors can grow their real estate portfolios aggressively and quickly using leverage. However, it is not clear if this is an option with Ark7.

Less Taxation Flexibility

Payments from Ark7 are taxed as LLC partnership income, per Ark7. This is slightly less flexible than the taxation of REIT distributions, which can be considered ordinary income, capital gains, or return of capital (Reit.com). In addition, Ark7 shares don’t have as many tax advantages as directly owning real estate such as the deductibility of interest and property tax payments.

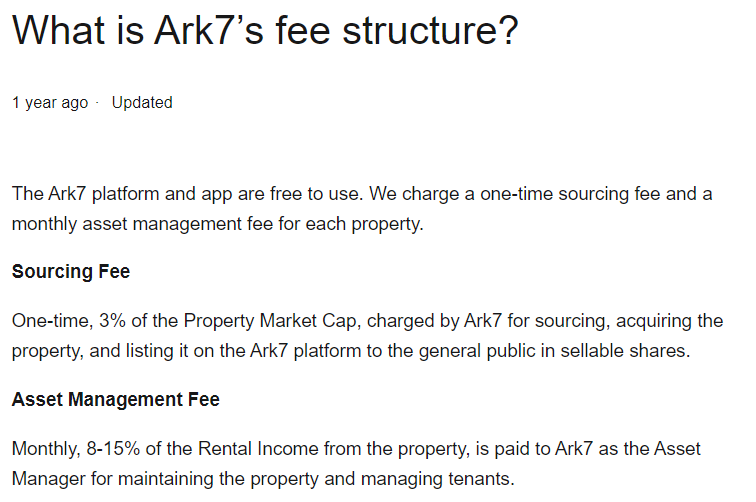

Fees and Pricing Structure

The platform charges investors a one-time sourcing fee of 3%, which is deducted from the rental income generated by the properties in which they have invested. This fee covers the cost of managing the properties, including property maintenance, tenant management, and other administrative tasks. Ark7 also charges between 8% and 15% monthly for management fees. They also charge an annual fee for IRS accounts.

Here is the fee structure from its webpage.

It is important to note that investors may be subject to other fees, such as a documentation fee or transaction fee. These fees are typically charged when investors make a transaction on the platform, such as when they invest in a new property or when they withdraw funds from their accounts.

Ark7 also charges annual fees for their IRAs. This is a $100 custodial fee, per property, per year. Ark7 will waive the fees if your IRA balance is more than $100,000 and caps the fee at $400 per year.

Ark7’s fees generally lower the platform’s return on equity. However, these rates are comparable to fee structures charged by realtors and management companies. In this regard, they likely reflect the underly unavoidable economic costs of owning and operating real estate. Tenants need to be screened, properties need to have appliances updated, roofs repaired, etc.

What are Ark7’s Long-Term Prospects?

While the fintech real estate space is extremely competitive, Ark7 is well funded.

Any potential investor looking at Ark7 may wonder if the platform will be around in the next five to ten years to deliver on the returns investors are anticipating. In this regard, Ark7 is well-funded. It received two tranches of funding one of $2,000,000 in 2019 (Crunchbase) and one of $9,000,000 in 2022 (Pitchbook). While exact figures are not available, Ark7 has likely sold at least over an additional $1,000,000 worth of securities. In addition, Ark7 charges management fees on the $19 Million worth of property it manages.

In short, the company appears well-funded and has a cash-generating business model. This suggests it will be around for the medium to short term.

Is Ark7 Right For You?

On the whole, Ark7 is a good fit for risk-tolerant investors who are interested in passive geographically targeted real estate investments.

Relative to its competitors, Ark7 offers quality investments in geographic real estate. It is however a newer platform. In addition to market risk, interest rate risk, and asset risks, investors take on the added risk of investing through a new platform with unproven longevity.

However, real estate as an asset class is generally desirable. If you’re looking for a way to generate a steady passive income stream from real estate investments, then Ark7 may be a good fit for you. However, if you prefer more control over your investments or are looking for higher returns, you may want to consider other options.

Ultimately, whether or not Ark7 is right for you will depend on your individual investment goals and risk tolerance. If you’re looking for less risky returns, you may want to consider a REIT index fund. However, if you are risk-tolerant and want a low-maintenance way to make concentrated investments in real estate and generate passive income, Ark7 is a great option.

Sign up For Ark7

Signing up with Ark7 is easy. Pretty much all that is required is a US bank account and a social security number. The process is just like opening a bank account — you need to fill out a couple of forms and provide your address and other identifying information. A simple account gets you access to Ark7’s single-family home investments. You need to be an accredited investor to get access to their multifamily and commercial listings.

Ark7 is a legitimate platform that lets risk-tolerant investors passively invest in real estate for as little as $20.

The fees you pay when you use Ark7 can be high, which can reduce your potential returns. You also need to keep your money invested for a minimum holding period, between three months and a year.

However, the platform is innovative, interesting, and well-suited for investors who want a targeted real estate strategy.

I’m crashing on some work today so here, so this posting is for everyone thirsty for good things to put into their mind. So, without further ado, here are my favorite books on personal finance.

The author of The Intelligent Investor was Benjamin Graham. Benjamin Graham is famous for being the mentor to billionaire Warren Buffet of Berkshire Hathaway fame. Not a lot of people realize it, but Graham was an uncommonly intelligent man. He was born in 1894 and is reputed to have earned a half-million-dollar salary in finance by the age of 25, which was a lot of money in 1919! Graham introduced the notions of ‘intrinsic value’, and buying at a discount to that value to the discipline of securities investing. He’s had a tremendous impact on my own personal investing philosophy. I can’t recommend his book enough.

Malkiel’s book is mostly memorable because it demolishes a lot of the junky philosophies which can be found in the investing arena. He argues that markets are basically efficient which means that a given securities’ price reflect all available knowledge about that security. The implication of this is that it is impossible to realize long-term value through structural inefficiencies in markets. Not everyone believes this, but you should check it out if you haven’t already done so.

Bloggers love this book. It’s very easy to read and has some interesting insight. The authors are a couple of marketing professors from New York. They drew a sample of millionaires based on census data and then mailed them a survey to ask about their financial status and personal habits. They found, based on their survey and their later interviews that millionaires were more likely to be frugal, hardworking, small business owners. Most of them owned stock and other investments, but their primary driver of wealth was equity in their business.

I’m recommending this book because it’s a good read, but, if you read the fine print in the back, only 2 out of 10 people answered their survey, so it’s really impossible to tell how accurate their picture of America’s millionaires is. My feeling is that their data tend to overrepresent business owners and underrepresent people who’ve achieved wealth through other means like stock market investing.

For this book Stanley solo authored the work on this one. I’m not 100 percent sure why. Also, I think the book suffers a bit in this regard because Stanley’s insight isn’t as fresh in this round. But, it is worth going down to your local library and picking up a copy of this book. There are two arguments I think it’s working through in this one: 1) that married persons are more economically productive than single persons, and 2) that people with low scholastic achievement can still achieve wealth through perseverance and hard work. It’s an empowering message because it suggests that even if one isn’t that smart or that great of a decision-maker, one can still get ahead.

This is a good, good book. Charles Carlson is a big proponent of dividend reinvestment programs. What he is basically saying is that the way to become a millionaire is set a goal, and invest regularly, for a long, long time in quality stocks while using tax-advantaged accounts. Bob Carlson is an investment advisor so his focus is primarily on the stock as a means to wealth. It’s an informative read, and his strategy is a good one for people who don’t have a lot of time but want to build wealth anyways.

That’s all for now folks. I hope this has been helpful!

And, if you have a chance Kalen Bruce over at the MoneyMiniBlog has a solid list of 75 Must Read Personal Finance Books. Check it out if you need some reading ideas.

For free classic literature, consider Fullbooks.com.

Purchasing new electronics can be a serious investment, especially if it is something you will use regularly. Often times, this also means you pay top dollar. For instance, most recently, Apple and Samsung released phones priced between $800 and $1,000. Many people thought these are crazy. Who would pay that much for a phone? But, many buyers simply see a quality product.

The same can be said of many other electronics as well, including things you buy for a small business. What about printers? And specifically, what about the Afinia L301? Here is the Dinks review of Afinia L301 label maker.

The Afinia L301 Summary

I recently ordered an Afinia label printer for small business for my office and decided to take a look at how it performed. The results? The Afinia L301 was a bit of a hassle to set up, but the final product was well worth it. The machine has the potential to generate consistent savings for any business that needs a consistent level of printing.

About Afinia L301: Pricy, But Good Features

If you’ve not heard of Afinia printers before, they are some of the highest quality printers around, but they do come with a price. The L301 printer mentioned above costs about $1,249 but if you are using it for business it will definitely be worth it.

That price tag comes with plenty of great features, including a professional and glossy look. Afinia printers also come with a 1-year warranty.

Obviously, if you’re using one of these printers, you’ll be printing business labels and other items for your business. One of the key features that makes the label printer for small business high price tag worth it is the flexibility to make changes to label design at the last minute. You can also minimize waste by only printing the labels you need for the business you’re performing. If you only need one, only print one!

Using the Printer: Some Setup Hassles, But Quality Worth the Hassle

When it came to unpacking and setting the printer up, everything was a breeze. It only took about 10 minutes to set it up. here is what came in our order:

After setting the printer up, I discovered that software needed to be downloaded to the printer in order for it to work – it wasn’t automatically wifi enabled. So, You will need to download software for creating labels to be able to use the Afinia printer. There wasn’t anything mentioned clearly on their website about this, so it may catch some people by surprise (it caught me by surprise). However, the site does have some instructional videos that should help. That said, the process of installing the software and figuring out how it works is a pain.

Once you’re ready to print, you won’t be let down. The Afinia L301 printer takes just seconds to produce a high quality professional label. You can also customize the size of the label to just about any size you’d need. The printer was able to create an entire roll of labels in just minute with just a bit of adjustment time.

Here is a good basic instructional video on getting the Afinia set up.

A Price Savings? Online Labels Price Comparison

While the Afinia L301 label printer sounds good, the $1,249 price tag can turn many people off from the purchase. So, here are a few words on cost.

Getting custom labels printed costs between $1 and five cents, depending on the shape, size and material requirements you have for your label. Another factor is the quantity of labels you need. And something else to consider is how much time you have. If you need labels faster, it generally costs you more.

So, is it cheaper to print your own labels? What this comes down to is if you have a business that requires bulk and frequent printing then using your own resources to print is generally less expensive. However, if you only sell a few products that need labels per month, or you only have a one time need, outsourcing is a better choice.

The Price of Ink

You will want to be careful though. If your bottom line is saving money for your business, printers can also wind up costing you more than you save. How much it costs to fill the printer with ink and run it is important. A cheaper label printer with a high ink cost could easily become more expensive than a higher priced printer in just a couple of months. Alfinia provides a calculator to determine the cost of ink for each of your labels to determine if the purchase will be the right move for your business.

Where To Get The Afinia L301?

The Afinia L301 isn’t listed on Afinia’s website, so you’ll have to buy it on Amazon. You can get it by clicking on the image below or hitting the button underneath the picture.

Amazon retails the L301 for $1,249, which is considerably less expensive than the newer L701 and L502. These machines retail for $2,500 and $5,000 respectively. Amazon does have payment plans if you don’t have a spare $1,250 lying around. You can also buy this printer by clicking on this button.

All in all, the Afinia L301 label printer is a good machine and makes it easy to cut down waste while saving money on online printing services. The printing software does have some initial startup hassles, however the quality of the final product works as advertised and for a small to medium sized business, the Afinia offers a solid savings.

Its a Monday and I’m banging away in my home office here in Portland, Oregon. Earlier this month, I picked up some silver on Amazon, I ended up buying a few grams of silver rounds – I had some extra Amazon credit and I liked the idea of not wasting it.

So, the reason I’m bringing this up is, a while back, one of our readers emailed and asked us to write a little more about the pros and cons of buying silver. Here are a few points that are relevant if you are thinking of investing in this asset.

Reasons To Get Into Silver.

1) Limited Hedge Against inflation. Precious metals like gold and silver can hedge against inflation. However, the relationship between real returns on these assets and inflation isn’t that great, at least according to the scientific articles I’ve read. For example, one article argued that silver hedged inflation only during the early 1930s and the late 1970s, other articles didn’t show a relationship at all. So, what this indicates is that silver can hedge inflation, but its effectiveness has limitations.

2) Diversification. Most of the time when you hear about diversification, its in the context of the stock market. Typically you’ll see something to the effect that you need to buy stocks in larger and smaller companies, and that you need to get positions in different industries, etc etc. Well, hard assets like gold and silver tend to have low correlations with other types of investments. So, if your 401(k) stocks are declining, the price of silver might increase.

3) Return. One great reason to invest in silver is the possibility of making some money. For example, a friend bought a large batch of silver when the commodity was trading for less than 4 bucks an ounce. Recently the white metal has been trading for $31.09, which indicates a 770% return on his investment. That is a significant increase, and if you really want to build wealth you will need to find these kinds of opportunities as often as possible to realize real gains.

(Example of chart showing spot price of silver).

4) Low Cost. Silver usually costs less than $35 bucks per ounce. Even if you don’t have a lot of money, you can often get some silver with what you’ve got in your pocket or by scraping up change lying around the house.

Reasons NOT To Get Into Silver

1) Better alternatives. Another one of the pros and cons of buying silver is the presence of better alternatives. Silver and gold prices generally follow economic activity. So, when the economy is strong, these metals tend to do better. Like an inflation hedge, the relationship isn’t all that great, but it does exist. However, when the economy is doing well, other assets – stocks in particular – also do well.

Silver compares unfavorably with stocks for other reasons. For example, stocks pay dividends and can split. Splits and dividends can lead to compounding. If you buy actual physical silver bullion, you won’t be able to take advantage of this. So, briefly put, stocks are often a better alternative to silver because stocks provide cash and holding physical bullion doesn’t.

2) Hassles. Provided you are buying actual physical silver, taking possession and holding onto the metal can be a real pain. For example, if you have anything over 100 ounces, for example, you’d need someplace safe to store the stuff. This is usually a safe or a safety deposit box. The major problem here is that you need to incur the costs of the storage. Safes can be hundreds of dollars and deposit boxes can charge a healthy annual fee. Also, if you are buying the silver, you need to get in the car, or get on the subway, or whatever and actually go and make the transaction. Both storage and buying can be a hassle.

3) Freak Factor. Another one of the pros and cons of buying silver – in this case a con – is the freak factor. A lot of people who are really heavily into owning gold and silver are conspiracy theorists. They believe the government is going to confiscate their bullion, that the federal reserve is a Jewish cabal that is out to control the world, etc. etc. Plus, a lot of bullion dealers are pretty crusty people. They tend to be a bit suspicious of anyone who isn’t a 40 to 60 year old white Anglo-Saxon slightly overweight white guy. Do you really want to be associated with that crowd? I personally don’t mind so much, but its a legitimate question.

So, what should you think about when buying silver?

Assuming you want to buy actual physical silver…

1) Get something standard. There are a lot of private companies that have produced silver rounds. These vary in the quality and amount of bullion included. Instead, of getting these, consider Canadian Maple Leaf or American Eagle coins. These are produced by the Canadian and US Federal governments, so they are standard and a bit more universally recognizable than the private options. More importantly, they also have higher resale value.

2) Know the market. Silver trades on exchanges just like stocks. The value of silver at any on point in time is called the spot price. Don’t pay more than a couple of dollars over spot. A lot of dealers will try to jack you on price so know your market and shop around. Consider both local dealers and online sources like eBay.

If you want to get into silver, but don’t want to buy the actual metal…

1) Buy an exchange traded fund. A couple of popular ones are: SLV, DBS and AGQ. The investments indicated by DBS and AGQ track the index price of silver and may be a bit cheaper over the long run due to lowered expense ratios.

2) Consider a mining company. A lot of mining companies haul silver out of ground as a by product of their operations. Or the alternative is that you can buy shares directly in a mining company that focuses on extracting and producing silver.

3) Other alternatives. There are a TON of ways to invest in silver other than physically buying the metal or getting it indirectly via an exchange traded fund or a mine. These other options include spread betting and derivatives. I know almost nothing about these alternatives, so its best to check Wikipedia.

Finally if you want a read about a really hardcore silver mine, check out the story of the Bolovian Potosi mine. The Potosi mine singled handedly funded Spain’s ascension to world power in the 17th century and was responsible for the deaths of hundreds of thousands of indigenous persons. The mine is so deadly, it has an image of a devil like imp as its patron saint. Its very interesting story indeed.

Having been around the wealth-building game for nearly a decade, I’ve had a chance to learn a few things.

First, getting financially fit occurs in a few reliable stages. Typically you pay off any debts. Second, you build up a cash nest egg and third, you start to acquire assets. This happens more or less in a typical progression. But what is less obvious is how to accelerate this process.

Here is a hint, wealth building is a team sport. That is, you need to make friends and work with good advisers to maximize your wealth accumulation.

1) Large Assets Generally Transfer Through Relationships

Large assets can be real estate, commercial real estate, business interests, large public or private stock placements, or gold bullion, etc. The process of getting your hands on assets worth having is ultimately going to involve forming relationships with persons who have these goods to sell or who can help you buy them.

For example, you may want to recruit a good real estate agent or you might need a friendly mortgage broker, or you might want to strike up a relationship with a small business broker who can help turn you onto deals.

In any case, you’ll want access to a good commercial banker. Like it or not commercial banks have access to large amounts of capital and you might need this if you’re serious about seizing opportunities you can scale.

2) You’ll Need To Get Involved in Business

This seems a bit controversial, but if you look at wealth in America, you’ll immediately see that only a very small number of fortunes have been made exclusively through saving or from low-probability events like winning the lottery or legally seizing someone else’s wealth (through the courts or war).

Most, regardless of size, are built by either starting or managing successful businesses. This applies not only to entrepreneurs who launch their own companies but also to investors who participate in the stock market.

The stock market is in effect a derivative way to profit from the management and running of successful businesses.

If you choose to become rich, you’ll need to ultimately find someone to help you manage, promote, or work in your enterprise. The reason for this is that there are only so many hours in the day and you’ll eventually run into limits on your knowledge and ability to exert effort. This problem will become even more acute as your business grows.

3) As You Get Richer, You’ll Need Help Accounting For Everything

The more wealth you have, the more you’ll need someone to help you deal with all of it. For example, the more income you have the more you will need someone to help you with income taxes. Generally speaking, as your income improves, your tax situation becomes more complex. In addition, the IRS and US Congress typically change tax regulations yearly. So, hiring professional tax help can mean the difference between paying thousands per year in income taxes or not.

4) People You Need On Your Team:

Tax Accountant – As your wealth gets more complicated, record keeping and accounting become more important in determining return. Accounting is especially important if you own real estate or a complex business. Part of the benefits of owning a rental property is the ability to take a deduction on the expenses incurred in running the property. However, this deduction can get phased out on your Federal return if your income exceeds a certain threshold, thus reducing the real return on your investment. So, to make the best decisions regarding capital allocation you’ll need to work with a tax professional.

Real Estate Agent – Most wealthy people own some kind of real estate. You can’t really buy real estate without an agent. Find someone who understands your needs, helps guide you to find the right place, doesn’t pressure you into something that doesn’t suit your needs, and negotiates on your behalf. Most people only buy real estate once or twice and therefore don’t think much about selecting an agent, but this is shortsighted.

Mortgage Lenders – Interest rates have a significant impact on your long-term expenses and wealth building. A good relationship with a mortgage lender can make it easier to buy property – they can advise you on what’s feasible when structuring deals. Make sure to evaluate several lenders to compare rates and terms. Lenders are like commercial bankers, they’re basically your access to capital, so you’ll want to appropriately nurture those relationships.

Contractors & Service Providers – Contractors and Service providers are key if you run any kind of business. For example, if you run a portfolio of rental properties you’d want someone good in home repairs or renovations. Alternatively, if you have a consulting business you might need bookkeeping or marketing help.

Financial Advisor – Most financial advisors are insurance salespeople or have conflicts of interest that prevent them from adequately serving you. However, if you find a good fee-only financial advisor whose focus is truly on maximizing your wealth, hire them.

Regardless of where you are in your wealth building, consider being strategic in your relationship approach. Try to find people who share your interests, who are very good at what they do, and who are willing to work with you.

Finally, remember this: there is no such thing as truly passive income. Someone has to work for wealth to be created. Many great economists have noted this. Marx and Adam Smith said that value is determined partly by the amount of labor invested in a commodity. So, it’s fair to say that without labor, there isn’t going to be a lot of wealth accumulation happening – regardless of the economic model you’re invested in. So, the bottom line is that to get rich, paying a team to support you in the process is worth every penny.