One thing I love about the stock market is that it provides objective feedback — either you make money or you don’t.

I was talking with another blogger earlier this week (we all know each other) and the question about objective returns on stocks came up. So I had a look at my portfolio. To my shock, it looks like I’ve been an underperforming stock picker.

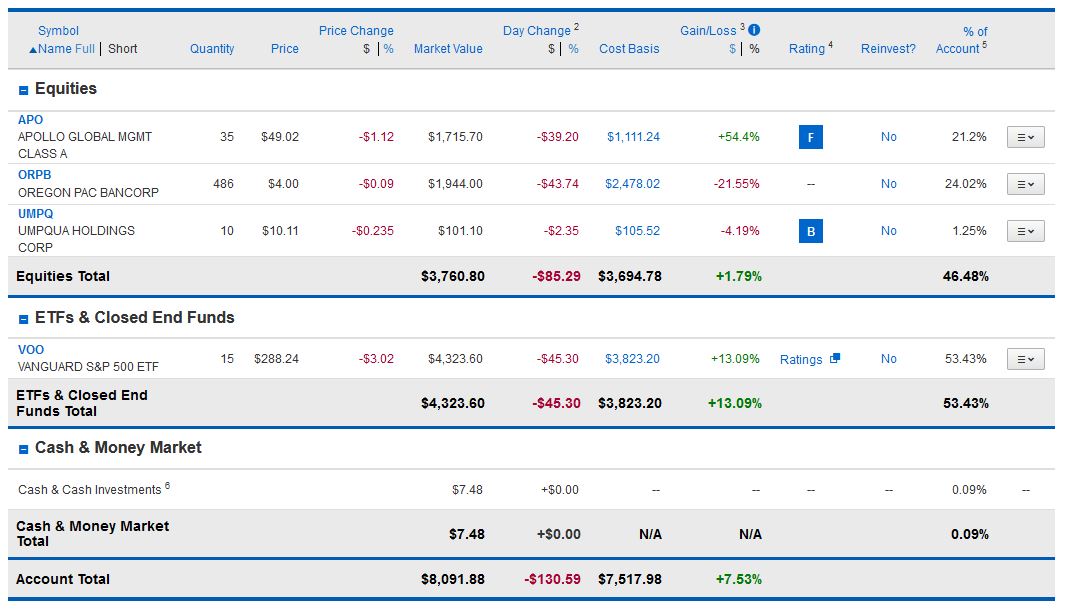

Here is a screenshot from my SEP-IRA:

The top part shows my individual stocks. I’m holding three. The bottom part is basically my S&P 500 ETF. In total, my stocks have returned 1.79 percent. So, that means my picks haven’t made much money. In contrast, my S&P 500 shares are up by 13.09 percent.

This is a bit of a bummer because I’ve hit some home runs in the past – notably with Monster energy.

It is also a bummer because stocks are historically the best asset class to own. They perform better than bonds and cash in almost all circumstances. And, having a high return on your investments over time is a strong driver of wealth at retirement.

So, I’ve been brainstorming on how to improve which stocks I buy. If you’re in the same boat, here are some potential approaches.

1. Stop Buying Individual Stocks.

Just go with mutual funds, index funds or ETFs.

2. Go With An Established Stock Picking Methodology.

One reason I’m an underperforming stock picker is that I don’t have much discipline in how I pick stocks. My strategy has been idiosyncratic — I just buy whatever seems like a good idea at the time. This has obviously resulted in low returns, so a better approach might yield more profits.

There are at least two good methods to consider: CANSLIM and the Piotroski F-score.

CANSLIM:

CANSLIM is a stock-picking methodology developed by William O’Neill, the founder of Investors Business Daily (IBD). It’s a method for selecting stocks using both fundamental and technical analysis techniques. CANSLIM has seven elements, each corresponding to one of the letters in the acronym.

C = Current Quarterly Earnings. CANSLIM practitioners want quarterly earnings to grow by at least 25 percent.

A = Annual Earnings Growth. The criterion here is an annual growth of at least 25 percent or more in the past 3 years.

N = New. CANSLIM proponents say that good investments are companies that have something new or disruptive. Good examples are Uber and Airbnb. Both companies leveraged handheld computing to solve inefficiencies in the taxi and rental real estate business.

S = Supply and Demand. CANSLIM investors avoid being underperforming stock pickers by looking for stocks being accumulated by institutional investors.

L = Leader vs. Laggard. Basically, CANSLIM’ers look for stocks close to 52-week highs being acquired by institutional money.

I = Institutional Sponsorship. Banks, mutual funds, pension funds, or other large institutional investors are buying the stocks. Most importantly, institutional ownership should have increased over the past few quarters.

M = Market direction. This refers to investing along with general market trends. The market refers to broad indexes such as the S&P 500, the DOW Jones Industrial Average, or the NASDAQ Composite.

Moneycrashers.com has a really nice summary of the CANSLIM method. IBD’s website is here.

The Piotroski F-score:

Another good stock-picking method is the Piotroski F-score. The F-score is a value investing methodology based on the work of Stanford accounting professor Joseph Piotroski. It’s less well-known than the CANSLIM method. The F-score is basically a simple way of using 9 criteria to measure a company on three underlying factors: profitability, financial leverage/liquidity, and operating efficiency. I’m not well-versed in it, but supposedly it’s able to predict the price of a company in the near term. Here is Petroski’s original paper.

3. Use A Stock Picking Service.

If you’re an underperforming stock picker like me, a professional stock picking service might help. Some good ones are:

1. The Motley Fool’s Stock Advisor:

The picks are selected by Tom and Dave Gardner, founders of the multimedia financial services company, The Motley Fool. Their choices are based on modified value and growth investing perspectives. Their services have juicy returns — 150 to 200 percent figures are touted in their marketing. However, The Motley Fool has been criticized by some who say most of its portfolio’s returns are based on the success of just a handful of stocks. However, its in-house communities are generally well-reviewed and the company has an overall favorable reputation. The service costs about $99 per year. The Motley Fool Stock Advisor’s webpage is here.

2. The American Association of Individual Investors Model Portfolio:

AAII (American Association of Individual Investors) is a non-profit corporation focused on allowing individual investors to become better managers of their own money. The AAII operates on a freemium model — some of its investment information are free, but most of its materials are for dues-paying members. The AAII has a strong community of local chapters and is well-rated by the Better Business Bureau. It charges about $198 per year, so it’s not free.

3. Morningstar StockInvestor:

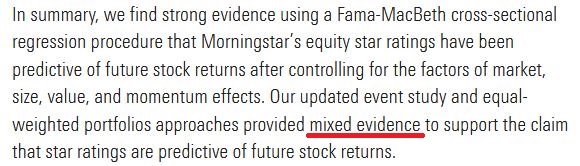

Morningstar StockInvestor is a monthly newsletter that emphasizes a wide-moat investing strategy. I don’t like it. Its manager is a guy named David Harrell, who looks like an unlikely candidate for a professional stock picker. Harrell has degrees in music and biology, not finance. Also, Morningstar’s rating system has been heavily criticized by some academics on issues of mutual fund classification accuracy. In addition, Morningstar’s own internal reviews suggest that its star rating system, in general, has a mixed record in predicting future stock returns. Here is the relevant language from its webpage:

Its StockInvestor costs about $145 per year.

4. Jim Cramer’s Action Alerts PLUS:

Action Alerts PLUS is an investing newsletter run by Jim Cramer of CNBC’s Mad Money and his staff at TheStreet.com. The platform shows Cramer’s recommended portfolio, recommended stocks to buy and sell, as well as analysis on how stocks in the portfolio are moving. All of Cramer’s buy/sell recommendations are executed through his Action Alerts PLUS charitable trust, with a high degree of transparency.

The one highly cited independent review of Cramer’s Action Alerts PLUS was mixed. Jonathan Hartley and Matthew Olson’s review of Action Alerts plus suggests that between 2001 and 2016, Cramer’s stock choices underperformed the S&P 500 by a modest amount. They found that Action Alerts PLUS yielded 64.45 percent cumulative returns versus the S&P 70.04 percent cumulative returns. So, Action Alerts PLUS is doing about as well as the market.

Cramer’s Action Alerts PLUS costs $59.95 per month.

5. Buffet’s Annual Letters:

An underperforming stock picker might follow Warren Buffet for stock-picking advice. Usually, Buffet outlines which stock his company Berkshire Hathaway holds in his annual letter to shareholders. Buffet’s letters merit some attention if you’re looking at ways to improve your stock picking ability.

An underperforming stock picker might follow Warren Buffet for stock-picking advice. Usually, Buffet outlines which stock his company Berkshire Hathaway holds in his annual letter to shareholders. Buffet’s letters merit some attention if you’re looking at ways to improve your stock picking ability.

One major drawback to following Buffet’s picks is his age. Buffet has been an active investor since the 1950s and has an exceptional track record. However, Buffet is eventually going to die — and likely sooner rather than later. With most money managers being unable to beat the S&P 500, any likely successor will need to be exceptional indeed to be as good as Buffet at selecting investments.

Buffet’s letters are here. If you want a good independent assessment of Buffet’s actual stock picking history, read James Altucher’s book Trade Like Warren Buffet.

How To Fix My Underperforming Stock Picker Habits?

I’ll likely weigh my purchases to index funds and select one of these services to work with. This seems like a good way to stop being an underperforming stock picker.

Further Reading

Our Review Of The Motley Fool Stock Picks

Building Wealth on $600 Per Month

How Much Interest Does A Million Dollars Earn Per Year?

What Are The Traits That Make A Great Investor?

Readers, if you have ideas that haven’t been included here, please leave us a comment below.

Disclosure: Some links in this article are affiliate links. Dinksfinance.com will earn a commission if you click through and buy something. Dinksfinance is independently owned and the views expressed here are entirely my own.

No Comments yet!