January gets all the blame for post-holiday money stress, but for a lot of couples, the real pinch shows up later. You finally feel like you’re back to “normal,” and then February arrives with a credit card balance that won’t quit, surprise renewals, and a calendar full of plans you forgot you agreed to. That’s the spending hangover in its truest form, the fun is over, but the costs keep showing up. For DINK couples, it can feel extra annoying because two incomes should mean faster recovery, yet the drag still happens. Here’s why it lingers, what it looks like in real life, and how to clear it without turning your budget into a punishment.

Why The Spending Hangover Hits Later Than You Expect

A lot of holiday costs don’t land when you spend them. Credit card statements close after the holidays, travel charges finalize late, and returns can take weeks to process. Some expenses also get delayed on purpose, like “we’ll deal with it in January,” which quietly becomes “we’ll deal with it in February.” The result is a weird time gap where your bank account looks fine, but your overall financial picture is still recovering. That delay is why this financial situation can feel like it appears out of nowhere.

The Sneaky Costs That Keep The Cycle Going

February often brings a second wave of spending that’s easy to ignore when you’re focused on paying down December. Valentine’s Day plans, winter weekends out, and little “we deserve this” purchases can stack on top of the remaining holiday balance. Subscription renewals also love the new year, and annual fees can hit when you’re least excited to see them. Add in seasonal stuff like higher utilities or winter travel, and the budget gets squeezed again. When these layers pile up, the spending hangover turns into a longer season instead of a single rough month.

How It Shows Up For DINK Couples

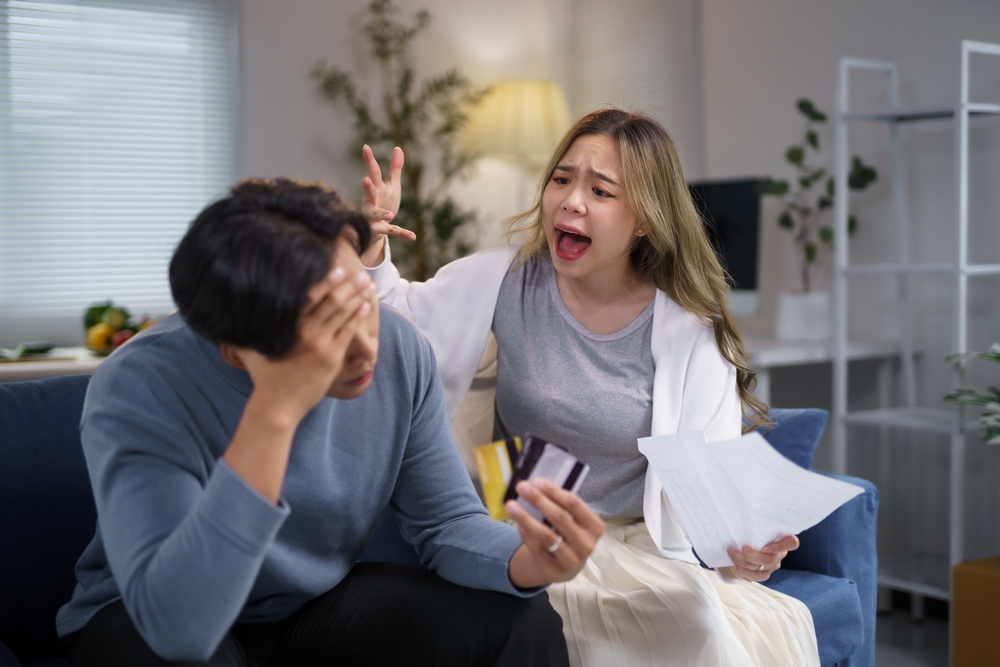

For many couples, the hangover isn’t just a number, it’s how you feel when you look at it. One partner wants to aggressively pay down balances and pause fun spending, while the other feels like life is already stressful and doesn’t want to “live on restriction.” You might start second-guessing plans like weekend trips, concerts, or dinners out because the leftover holiday costs keep whispering in your ear. Even if you aren’t in debt, you may feel behind on goals like investing, saving for a home, or building a travel fund. That’s when the spending hangover becomes emotional, not just financial.

The “We Didn’t Mean To” Budget Leaks

Most lingering holiday costs come from category creep, not one giant splurge. It’s the shipping fees, last-minute add-on gifts, extra meals out, and convenience spending that snowballs. Then January arrives and you’re tired, so you keep ordering takeout because cooking feels like too much. Suddenly you’re paying for the holidays and paying for recovery at the same time. These leaks are frustrating because they don’t feel like “real spending,” yet they absolutely count. The fastest way to shrink a spending hangover is to plug two or three leaks instead of trying to overhaul everything.

A Two-Week Reset That Doesn’t Feel Like A Crash Diet

A reset works best when it’s short, specific, and agreed on by both partners. Pick a two-week window where you pause the biggest “extras” category, like delivery, cocktails out, or impulse shopping. Decide on one replacement that still feels like a life, such as a home date night, a simple brunch at home, or one planned outing instead of three random ones. Put any refunds, cash-back, or gift card leftovers toward the same goal, because that creates fast momentum. When you treat it like a sprint, the spending hangover starts to lift without resentment.

The One Conversation Couples Skip That Would Help Most

Instead of asking, “How did we spend so much?” ask, “What did we expect recovery to look like?” One person may assume the holidays get paid off by the end of January, while the other assumes it’s normal to carry it into spring. If you don’t align expectations, you’ll feel like you’re failing even when you’re fine. Set a clear finish line, like “We want the holiday balance gone by February 20,” or “We’re rebuilding our cash buffer by March 1.” A shared timeline turns the spending hangover into a plan instead of a cloud.

Simple Rules That Prevent Next Year’s February Drag

You don’t need complicated rules, you need repeatable ones. Create a holiday “all-in” number that includes travel, hosting, outfits, and shipping, not just gifts. Set a check-in threshold for any single holiday purchase over a certain amount, so surprises don’t slip through. Build a mini “January buffer” in December with one extra transfer to savings, even if it’s small. These habits make the spending hangover less intense because you planned for the aftershock.

Turning The Spending Hangover Into A Win

The point isn’t to regret the holidays, it’s to learn how your money behaves afterward. When you name the delays, identify the leaks, and agree on a short reset, February stops feeling like a financial punishment. You also build trust, because both partners know what’s happening and what the next steps are. Recovery feels better when it’s shared and realistic, not silent and stressful. Once you clear the spending hangover, you get your momentum back for the goals you actually care about.

What part of the hangover hits your budget the hardest, and what’s one rule that would prevent it next year?

What to Read Next…

Here Are Some Amazing Valentines Day Letter Board Ideas

7 Subtle Spending Habits That Add Up in Child-Free Homes

Why So Many Child-Free Couples Are Quietly Downshifting in 2026

7 Social Pressures That Push Couples to Overspend Without Realizing It

Two-Income Couples Who Feel “Behind” Often Make This One Mistake

Why Some Couples Without Children Regret Their Spending Although They’re Affluent