Hello New Visitors,

If you’ve arrived at our blog via Stumble Upon, welcome!

Just wanted to remind you that if you like what you read, you can subscribe by clicking here.

Thanks!

-James

Hello New Visitors,

If you’ve arrived at our blog via Stumble Upon, welcome!

Just wanted to remind you that if you like what you read, you can subscribe by clicking here.

Thanks!

-James

Hi All,

Hi All,

This posting is a quick rant about one of my personal finance pet peeves: on-line calculators. A lot of people use on-line calculators to help them make financial decisions. However, they fail to realize that many on-line calculators are only crude approximations of financial reality.

There are at least two problems with many on-line calculators.

1) Reliance on Compounding Assumptions:

Many calculators assume that compounding occurs linearly over time. Right, you plug in your numbers, assume some given interest rate per year and at the end of a period of time, you will have some amount of money. This, unfortunately is at odds with reality. In reality, people are much more erratic in their savings behavior. Think about it, your bank changes interest rates and you probably don’t save the same amount each month. To assume that your interest will compound over time at the same rate every year is not tenable.

2) Ignoring Inflation:

Inflation occurs when there is a sustained rise in prices over a given time. It has the insidious effect of reducing the long term purchasing power of your money. This is a problem because many calculators do not account for inflation. Lets say for example that you have the goal of saving $40,000 to buy a house. Well, if you relied on a simple compound interest calculator in a high inflation environment, it turns out that instead of $40,000 you might actually need $45,000. The difference is due to the loss in purchasing power of your money due to inflation. this is a problem because when you take your $40,000 to market, you might find its not enough to get the job done.

If you do want to make reasonable assumptions, be sure your calculator accounts for both real world contingencies and inflation. Click here and here to get started.

Best,

James

I like Peter Lynch because he’s a populist. I especially enjoyed his book “One Up On Wall Street”. This quote just about sums it up:

“It’s Best to define your objectives clearly and clarify your attitudes beforehand, because if you are undecided and lack conviction, then you are a potential market victim, who abandons all hope and reason at the worst moment and sells out at a loss. It is personal preparation, as much as knowledge and research, that distinguishes the successful stockpicker from the chronic loser.”

– Peter Lynch

One Up On Wall Street

If you think gas prices are expensive here, you’ve got to check out the prices around the globe. In fact, the US comes in at 108th out of a survey of gas prices in 155 countries. Most countries in Europe have been used to shelling out a great deal more per gallon. Check out how we rank:

Keep in mind that all gas prices are not created equal. The retail price is based on whether a given government taxes gas, as many European nations do, or subsidizes it as the US does.

The US government has been giving tax breaks to the oil and gas industry for years to keep the price of gas artificially low. Without these tax breaks, the industry would arguable pass on higher gas prices to the consumers at the pump.

Now while nobody wants to hear about further increases in gas prices, it’s got to be asked why it is that the US government offers subsidies to one industry over another. According to the laws of supply and demand, they are messing with the whole system by keeping prices low to fuel the American gas addiction.

According to the Energy Information Administration, the artificial reduction in US gas prices has contributed to higher gas consumption. Since the 1980 the UK has had flat growth in gas consumption, France has seen a decline by 17%, and the US has increased its consumption by 21%.

You know where you really want to head for cheap gas: Venezuela has gas for 12 cents a gallon!

If you are interested in further information check out this piece on the real prices of gas.

Stay away from the pumps!

Miel

Today’s post is a reminder that it is the process rather than the numbers alone.

We are certainly advocates for achieving financial freedom to go after your personal and life goals. We also recognize that it is largely the process that makes the difference in whether or not happiness is attained in the short and long term.

This is one of the reasons why we feel strongly about working together as a couple. Doing this enables a stronger relationship overall, meaning that you’ll be more likely to enjoy your riches together.

It’s also not a particular amount that matters. Getting hung up on numbers, particularly with the economy as it is, won’t make it any better. Hang in there and work together. Yard by yard it’s hard. Inch by inch it’s a cinch.

Cheers,

Miel

Hi All,

Today’s posting is a quick piece on the economy. As you probably know, America is currently in the midst of a recession. There have been 6 straight months of job losses, the subprime mess is still with us, oil has busted $145 dollars per barrel thus driving up the price of everything, and inflation is at an 11 year high and – oh yeah – home prices are down by 15%. In short the news is bad pretty much everywhere.

Well, instead of panicking or buying survival gear and moving to Idaho, you might consider doing the following:

1) Stay Positive & Focused: It’s a bit silly, but thinking positive may actually help you achieve the kinds of goals you wanted to have. I don’t entirely understand the processes, but there seems to be something about the relationship between attitudes and action that suggests that optimists tend to be more likely to achieve their goals. Also, unless you are Ben Bernake, you can’t do much about macro economics. So, it makes sense to stay focused on your own goals.

2) Consider International Stocks: Things are kind of choppy in the US right now, but the world is a big place. For example, there are many fine European, Canadian and Chinese companies that are making healthy profits in expanding economic conditions. A couple of industries you might consider are Chinese companies specializing in exports, Canadian Royalty Trusts, and Swiss eco-companies. But, having said that we don’t have any recommendations for specific stocks, but do think you might consider looking beyond the US.

3) Consider Precious Metals: We don’t normally recommend precious metals because they haven’t done well historically. However, some people think that gold and silver are good stores of value that retain their intrinsic worth even in an inflationary environment, so you might consider it. The encouraging aspect of gold and silver is that you can get some for as little as $20 to $40. Just cruise over to ebay and see what’s available.

As a final note about precious metals – we are actually considering selling some of ours. But, that said, it is entirely likely that the economy will be shaky for the next few months, so you might consider picking some up anyways.

Finally, just to reiterate the main idea here. Even though the economy is bad shape, there are still some things you can do to maintain a healthy bottom line.

Best,

James

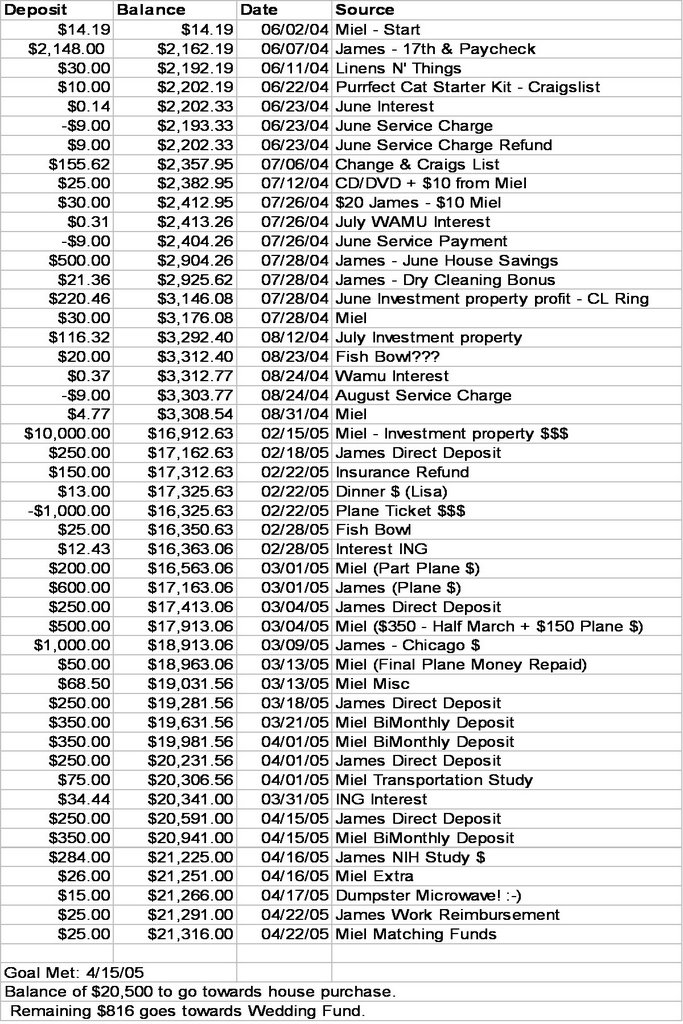

One thing about finance blogland is there is a lot of talk about saving, but fewer examples of how people actually do it. If you’re a frequent reader of Dual Income No Kids, you know that we are homeowners. When we were saving for our place back in 2004, we kept a record of where our savings came from. We thought you might enjoy having a look at this.

We did all kinds of stuff to meet our savings goals. For example, we set up direct deposit into ING, sold things on craigslist, put money from family into the fund, profit from our investment properties, pretty much anything to meet the goal. One time we found a working microwave in the dumpster, cleaned it up and sold it.

Some things weren’t that great. For example, James bounced a check because of some carelessness and we had to juggle the savings to cover his airfare for a work function at one point. The money got made up, but generally its a good idea to keep personal checking and savings accounts separate.

Also, we switched from a Washington Mutual to an ING savings account halfway through the process. ING has much lower monthly fees and pays a much higher interest rate than the Washington Mutual alternative we were looking at.

Hope you enjoy!

p.s. We had to truncate some of the lines to get the photo to fit, so the numbers don’t necessarily add up in the middle.

“Until one is committed, there is hesitancy, the chance to draw back, always ineffectiveness. Concerning all acts of initiative and creation, there is one elementary truth, the ignorance of which kills countless ideas and splendid plans: that the moment one definitely commits oneself, then providence moves too. All sorts of things occur to help one that would never otherwise have occurred. A whole stream of events issues from the decision, raising in one’s favor all manner of unforeseen incidents and meetings and material assistance,which no man could have dreamed would have come his way. Whatever you do, or dream you can, begin it. Boldness has genius, power and magic in it. Begin it now.”

– Wolfgang Goethe as Quoted by John Bogle

Like many of you, we get our inspiration from family. Miel and her sister were discussing her sisters lovely new house in Portland. And it came up that, PMI might be involved. For those with a mortgage, you probably know about PMI. PMI stands for Private Mortgage Insurance. PMI is required by some lenders when you have less than a 20% down payment.

Miel’s sisters question was: should you take out a second mortgage or pay for PMI?

Pros and cons of the situation

PMI Pro:

1) PMI has some limited deductiblity. Right, so you can deduct your PMI, but there are several limitations. These are 1) Limited Timing: you have to buy or refinance your home between 2007 and 2010. 2) Income phase outs: your spouse file a joint tax return and have adjusted gross income (AGI) of no more than $100,000 or you file an individual tax return and have AGI of no more than $50,000. 3) Refinancing limits: if you refinance, you can only take the PMI limits on your initial borrowing amount. For example if you bought a house and borrowed $75,000, but refinanced a year later for $90,000 you could only take PMI on the initial $75,000

PMI Con:

1) PMI is an extra expense

This is probably the biggest factor to weigh as a con. Most of the time if you don’t have enough for a full down payment you aren’t likely to want to add more expenses to your monthly budget. Additionally this feels like an expense that is going nowhere, since it is. It can also feel like a penalty for not having enough, thereby possibly giving the feeling of inadequacy when you have to shell out the dough.

Second Mortgage Pro:

1) You don’t have to pay PMI. This means that you can put the funds that would have gone towards PMI will go partially towards your equity, though not much. The major pro is that you’ll have a bit more in your monthly cash flow than you would paying PMI, all things being equal.

Second Mortgage Cons:

2) Interest rates are higher than on a first mortgage. This means that you’ll have a harder time paying it off as you’ll be working against yourself with the interest compounding. For example, we took out our 2006, we split the loan 80 /10, 80% on the first loan, 10% on the second loan. Our first loan had 6.5% and the second had 8.84% – roughly a 2&1/2 percentage point difference.

Given that both PMI and second mortgage have significant drawbacks, we’d advise the following strategies:

1) Do neither! You’re better off having twenty percent down to avoid having to make the choice between PMI and a second mortgage. Saving and investing is old fashioned, but it works. If you have 20% down you avoid both the higher interest rates AND paying PMI.

2) Do the math before you are ready to buy.

3) If you do have to make the choice, then do whatever you can pay down your debt so you aren’t fighting against high interest or insurance payments going down the drain. Paying off your mortgage to below the 20% loan to value ratio will allow you to stop paying PMI. If you pay off your second mortgage you can avoid higher interest rates.

If this post saves any readers from the woes of higher interest or PMI we’ve done our job in the blogsphere.

Readers: We’d love to hear any comments you have on experiences with PMI or second mortgages.

Cheers,

James&Miel

Hi All,

Hi All,

I just had to get this up. If you’ve been following the news about Zimbabwe, you probably know the economic situation is very bad there. But, now the AP news is reporting that inflation may be at 4 million percent. In February alone, the countries official statistics measured inflation at 165,000 percent. Let me repeat that – 165,000 percent, in one month.

Now, I’m not an economist, but 4 million percent is out of control. Effectively it means that Zimbabwe’s economy is ruined. Think about it – with that kind of inflation its impossible to save for a house or start a business. Since the money becomes worthless overnight, budgeting is an exercise in futility and if you already have a business or work for a wage, you are likely to get wiped out by the declining value of the currency.

The AP story is also reporting that its gotten so bad, the German firm that sells the bank note paper to Zimbabwe has stopped at the request of the German government. They don’t want to be a party to the disaster.

Check out the story here.

Best,

James

You cannot copy content of this page